BOOM: 11.7% Weighted Average 2016 Rate Increase Confirmed.

Thu, 11/12/2015 - 10:00am

[assuming that everyone currently enrolled sticks with their current policy next year], no matter how I slice it, the national weighted average increase for 2016 seems to be somewhere between 12% - 13%.

As I noted a couple of weeks later:

My attempt to boil down the overall, weighted-by-market-share, national average 2016 individual market rate increases into a single percentage figure has received a lot of attention over the past few weeks, including not one but two citations from Paul Krugman of the New York Times, feature articles from Bloomberg News and the Huffington Post, and even a partly-mangled version from the right-wing Daily Caller.

I'm not name-dropping for the heck of it here; my point is that I've been a little jumpy about that particular projection (12-13% overall) getting so much attention because I honestly had no clue how accurate it was.

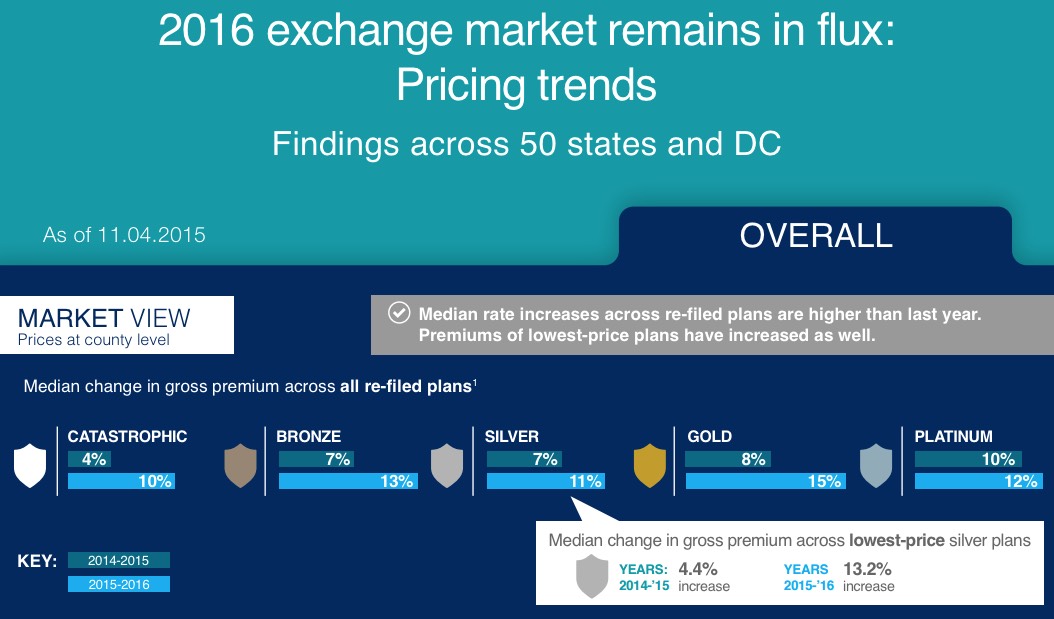

...As shown in Figure 1, the average lowest silver plan in states with a federal exchange increased by 13.0 percent from 2015 to 2016, compared to 3.2 percent from 2014 to 2015.

2016 Exchange Premiums: Changes in 2016 premiums vary widely by geography and regional market dynamics. When considering premium impact, note that over two-thirds of exchange consumers picked silver plans in 2015. Exchange plan enrollment is often concentrated in the lower priced plans in a particular metal level. As such, changes in the lowest priced plans in markets will have a larger impact on the average exchange consumer than the average premium for the entire market.

...Premium data based on the 2014 HHS Individual Market Landscape file, updated as of August 2014, the 2015 HHS Individual Market Landscape file, updated as of October 2015, and the 2016 HHS Individual Market Landscape file, updated as of October 30, 2015. The 2016 Landscape file is accurate as of October 16, 2015, after which several co-ops and other issuers may have exited the market. Analysis excludes state-based exchanges. All premiums are based on a 50-yr old non-smoker. Averages are not enrollment weighted.

As I also noted at the time:

- My estimate is based on both on- and off-exchange policies; theirs is based purely on exchange-based policies only.

- My estimate includes all ACA-compliant policies (ie, all metal levels, plus catastrophic plans); theirs is based purely on the lowest-priced Silver plans.

- My estimate includes all 50 states, plus DC; theirs includes only the 37 HealthCare.gov-based states.

- Also, it should be noted that Avalere's analysis of the lowest-priced Bronze plan came in with a higher average increase (16%) than the 13% for Silver.

However, having said that, Avalere's other points are also important to keep in mind: While they don't know exactly how many people are currently enrolled in "lowest-priced Silver plans", the odds are that it's well over 50% of them. Again, nationally, 68% of the total chose Silver plans, and most of that crowd likely went with the lowest-price offering. Another 21% went with Bronze plans.

...which brings us to today's report issued by the McKinsey Center for U.S. Health System Reform:

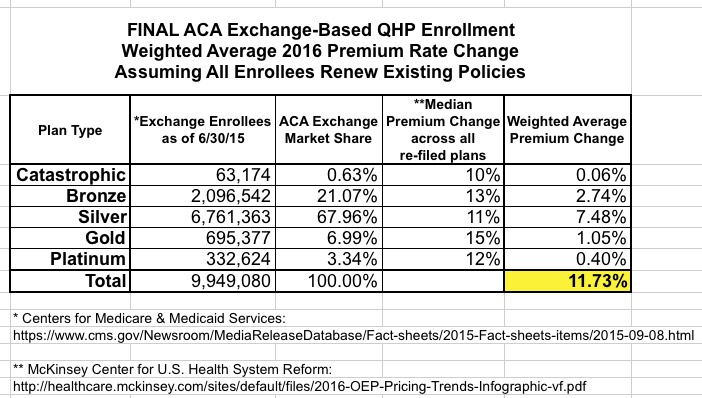

Here's the actual metal-level effectuated enrollment numbers from June.

Add them all up and you get:

BOOM.

According to the McKinsey Center report, the nationwide weighted average increase is 11.7%, slightly below my 12-13% estimate. Unlike the Avalere Health report, the McKinsey study appears to be more of a true apples-to-apples comparison:

- It includes all 50 states, plus DC.

- It includes all Silver plans, not just the lowest-priced one.

- It includes all Metal Levels as well as Catastrophic.

In fact, the only significant differences between the McKinsey Center report and mine are:

- My estimate includes off-exchange ACA-compliant policies as well as exchange-based ones

- My estimate attempted to look at the average change as opposed to the median change (the distinction of which, admittedly, is often difficult to remember)

Regardless, I think it's safe to say that my 12-13% estimate is on pretty damned safe ground.

Of course, even if I'm 100% on target, the biggest caveat here is that these numbers all still assume that everyone renews their existing policies instead of shopping around, which everyone should do. The lowest-cost plan within a given metal level won't make sense for everyone, but it will for many people, and if a significant number of people switched to a lower-cost policy it would indeed reduce the average rate changes significantly (I could see the effective average rate hike ending up around perhaps 9-10% nationally after the dust settles next spring).

Advertisement