Colorado: NET attrition rate estimated at...0.5% by end of year

Fri, 09/26/2014 - 1:46pm

Hat Tip To:

Esther F.

OK, the number-crunching gets a little complicated here, and isn't helped by some sloppy wording on the part of the reporter (though it's a highly useful article overall).

First, let's start with the headline: "Thirty-percent attrition bites into exchange revenues"

Health exchange managers expect to lose about 30 percent of enrollees due to attrition by year’s end.

That means they’ll carry over about 114,000 existing customers as they head into the 2015 open enrollment season.

Connect for Health Colorado managers expect enrollments to slide back from a total of 146,000 so far.

...Of the 146,000 people who signed up by the end of August, exchange managers said 10 percent dropped out right away, never paying their first month’s premium. Then about 20 percent more leave in subsequent months.

OK, "30% attrition" is, once again, misworded. The Colorado exchange has not seen 30% of enrollees drop their coverage, since 10% don't pay in the first place and are therefore never fully enrolled, remember? Out of the original 125,402 offiically listed on the March/April HHS report, only around 112,800 paid for their first month's premium. This may seem like semantics, but it's important to recognize that some are trying to attack the enrollment numbers on both the "But how many have PAID??" front as well as the "But how many have dropped out???" front. You can claim "10% never paid and another 20% dropped out" or you can claim "30% dropped out", but you can't truthfully claim "10% never paid and 30% dropped out".

Clear? OK. Moving on...

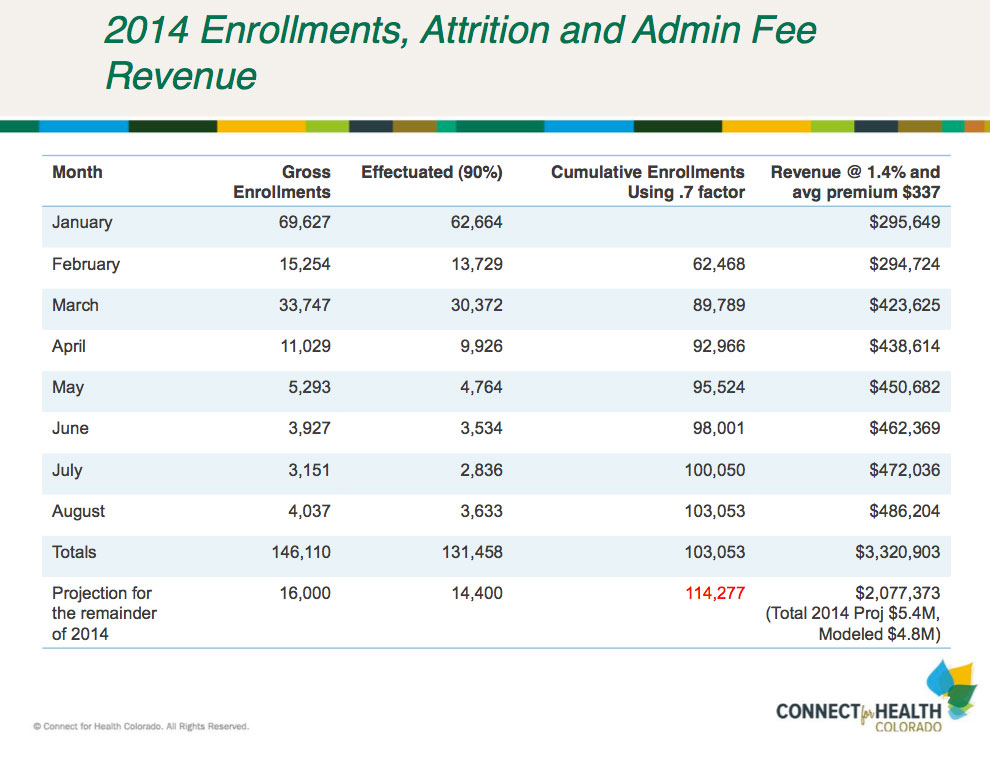

So, this article includes a handy chart which is very similar, at the state level, to my national attrition estimate chart:

According to this, as of the end of August there were 146,110 total enrollments, of which 131,458 (90%) paid their first month's premium and were therefore "effectuated" (ie, fully enrolled for at least one month). Out of those, 103,053 (78.4%) are still currently enrolled. That's a 21.6% gross attrition rate...but when compared to the original 112,800 figure, that's only an 8.6% net drop since April, or only 1.9% per month.

It's actually a bit worse than that, though, since the 146,110 figure includes about 2,500 SHOP enrollments, which aren't included in almost any other "QHP tally" that I (or anyone else) has done. Subtract those out and you get around 101,200, or about 89.7% of the April tally (around 2.3% attrition per month)

However, they also include their gross, paid and current (as of that time) projections through the end of 2014 (which presumably runs through 11/15, since anyone who enrolls after that doesn't start their coverage until January 2015 anyway, part of the 2nd open enrollment period).

That means that as of mid-November, they anticipate 114,277 enrollees to be currently enrolled as of that date. Again, subtracting out the SHOP enrollees, that should give roughly 112,300...or 99.5% of what Colorado started out with in April.

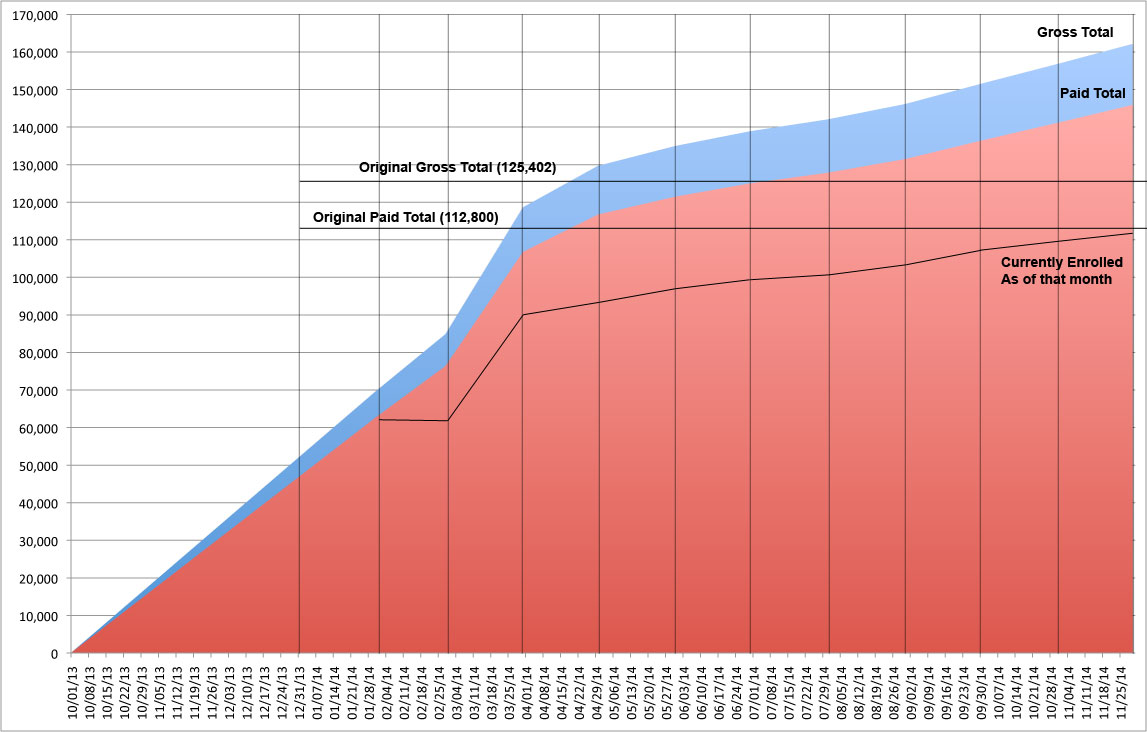

See, here's the problem with "attrition rates": What are you comparing the current number against???

- The total number reported by HHS as of April (ie, the "8 Million")? That'd be 89.5% in November.

- The paid number out of the April total (ie, 112,800)? That'd be 99.5% (that's the one I'm using, since I've already accounted for the 10% unpaid factor)

- The cumulative total number as of mid-November (around 159K)? That'd be about 70.6% (which is where the article seems to get their "30% drop" headline)

- The cumulative paid number as of mid-November (around 145,800)? That'd be around 77%.

So, an accurate attack on the Colorado numbers would be either:

- "10% of the April number didn't pay, and they lost another 0.5% by the end of the year!!", or...

- "They lost 10.5% of their April number by the end of the year!!"

...either of which is pretty weak tea to me.

Of course, the fact that the reasons why these people drop off the exchange policies can vary widely, including moving onto Medicare or Medicaid, or...

As the economy improves, it’s possible some people who needed individual insurance bought through the exchange, then dropped their coverage because they found work with an employer who provided insurance.

Note to conservatives: This is a good thing.

Advertisement