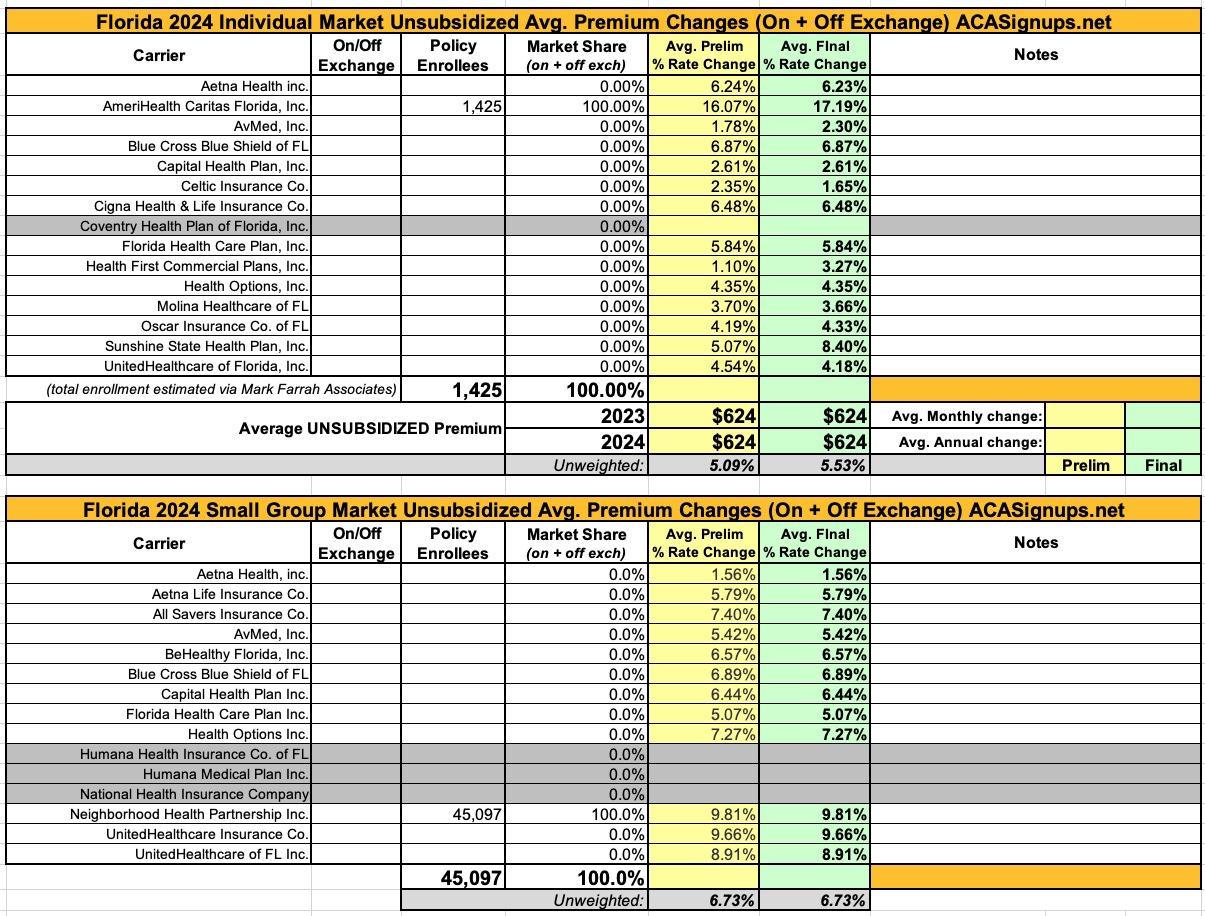

Florida: *Final* avg. unsubsidized 2024 #ACA rate changes: +5.5% (unweighted) (updated)

Thu, 11/02/2023 - 3:09pm

Originally posted 08/07/2023; updated 11/02/23

Florida state law gives private corporations wide berth as to what sort of information, which is easily available in some other states, they get to hide from the public under the guise of it being a "trade secret."

In the case of health insurance premium rate filing data, that even extends to basic information like "how many customers they have."

If you think I'm being sarcastic, this is literally a screenshot of what you get if you attempt to use the Florida Office of Insurance Regulation's filing search:

In any event, this means that I can only run the numbers on unweighted average rate change requests in Florida for the moment, since even the federal Rate Review website only lists the average rate changes themselves, while the enrollment data is redacted for nearly every carrier in both the individual and small group markets.

The most noteworthy items I can find for the moment are that Coventry Health Plan appears to be dropping out of the FL individual market, while Humana and National Health Insurance Co. are pulling out of the small group market.

Beyond that, the unweighted average rate increase being requested by indy market carriers is 5.1% (ranging from 1.1% to 16.1%), while small group carriers are requesting unweighted average hikes of 9.8%, ranging from 1.6% to 9.8%.

UPDATE 11/02/23: The final/approved rates have been posted at the federal Rate Review database, and it looks like average individual market rates have been bumped up slightly overall (4 increases, 2 decreases from the preliminary requests). Overall the unweighted average increase is +5.5%.

I should note that there are 2 carriers which do include unredacted filing summaries which include the enrollment numbers as well as other info: AmeriHealth Caritas FL on the individual market and Neighborhood Health Partnership on the small group market:

Scope and range of the rate increase -- Provide the number of individuals impacted by the rate increase. Explain any variation in the increase among affected individuals (e.g., describe how any changes to the rating structure impact premium)

1,425 AHC members in Florida are receiving a rate increase of over 15% effective 1/1/2024. These members are exclusively located in Broward County. Differences in rate increases across metal tiers is due to differences in the metal-level-specific pricing AV factors from 2023 to 2024.

2. Financial experience of the product — Describe the overall financial experience of the product, including historical summary-level information on historical premium revenue, claims expenses, and profit. Discuss how the rate increase will affect the projected financial experience of the product.

AHC entered the Florida individual ACA market in 2023. Current financial experience is limited; however, the 2023 rates were based on anticipated provider contracting levels that were not realized in provider rate negotiations. The 2024 rates reflect the current anticipated provider contracting levels. The projected financial experience of the product, however, is still based on a target medical loss ratio of >80%.

3. Changes in Medical Service Costs — Describe how changes in medical service costs are contributing to the overall rate increase. Discuss cost and utilization changes as well as any other relevant factors that are impacting overall service costs.

Please see the response to Question 2 above. Changes in medical service costs are a significant driver of the overall rate increases, based upon actual versus anticipated provider contracting terms.

4. Changes in benefits — Describe any changes in benefits and explain how benefit changes affect the rate increase. Issuers should explain whether the applicable benefit changes are required by law.

No changes to the medical benefits covered, however there are changes to the cost sharing amounts of the standard plan designs. The impacts of these cost sharing changes vary by plan, from roughly -0.1% to 0.5%.

5. Administrative costs and anticipated margins — Identify the main drivers of changes in administrative costs. Discuss how changes in anticipated administrative costs and underwriting gain/loss are impacting the rate increase.

Last year, AmeriHealth Caritas chose to enter the market without a profit and risk margin. This year, a 0.50% profit and risk margin has been included. In addition, AmeriHealth Caritas Florida is planning to invest in greater broker support for plan enrollment, resulting in higher commission rates. Both of these adjustments contribute modestly to the overall rate increase.

Scope and Range of the Rate Increase

The requested rate change for small group health benefit plans sold in the state of Florida will be effective January 1, 2024 and impact 45,097 covered lives. The rate change experienced by members will vary depending on plan selection and geographic area. Additional premium changes may occur upon renewal due to changes in member age, changes in plan selection, and changes in geographic location.

Financial Experience of the Product

The benefit care ratio for these products during January 1, 2022 – December 31, 2022 was 76.1%. This ratio is the portion of premium that is needed to pay medical claims. The complement of the benefit care ratio is the portion of premium needed for taxes and fees, administrative expenses, and margin.

Changes in Medical Service Costs

There are many different healthcare cost trends that contribute to increases in the overall U.S. healthcare spending each year. These trend factors affect health insurance premiums, which can mean a premium rate increase to cover costs. Some of the key healthcare cost trends that have affected this year’s rate actions include:

- Increasing cost of medical services: Annual increases in reimbursement rates to healthcare providers, such as hospitals, doctors, and pharmaceutical companies.

- Increased utilization: The number of office visits and other services continues to grow. In addition, total healthcare spending will vary by the intensity of care and use of different types of health services. The price of care can be affected by the use of expensive procedures such as surgery versus simply monitoring or providing medications.

- Higher costs from deductible leveraging: Healthcare costs continue to rise every year. If deductibles and copayments remain the same, a higher percentage of healthcare costs need to be covered by health insurance premiums each year.

- Cost shifting from the public to the private sector: Reimbursements from the Centers for Medicare and Medicaid Services (CMS) to hospitals do not generally cover the cost of providing care to these patients. Hospitals typically make up this reimbursement shortfall by charging private health plans more.

- Impact of new technology: Improvements to medical technology and clinical practice often result in the use of more expensive services, leading to increased healthcare spending and utilization.

Changes in Benefits

Changes in covered benefits impact costs and therefore affect premium changes. Benefit plans are typically changed for one of three reasons: to comply with the requirements of the Affordable Care Act or state law, to respond to consumer feedback, or to address a particular medical cost issue to provide greater long‐term affordability of the product.

Administrative Costs and Anticipated Margins

Neighborhood Health Partnership, Inc. works to directly control administrative expenses by adopting better processes and technology and developing programs and innovations that make healthcare more affordable.

We have led the marketplace by introducing key innovations that make healthcare services more accessible and affordable for customers, improve the quality and coordination of healthcare services, and help individuals and their physicians make more informed healthcare decisions. Taxes and fees imposed by the State and Federal government are significant factors that impact healthcare spending and have to be included in the administrative costs associated with the plans. These fees include Affordable Care Act taxes and fees which impact health insurance costs and need to be reflected in premium. Another component of premium is margin, which is set to address expected volatility and risk in the market.

The requested rate change is anticipated to be sufficient to cover the projected benefit and administrative costs for the 2024 plan year.

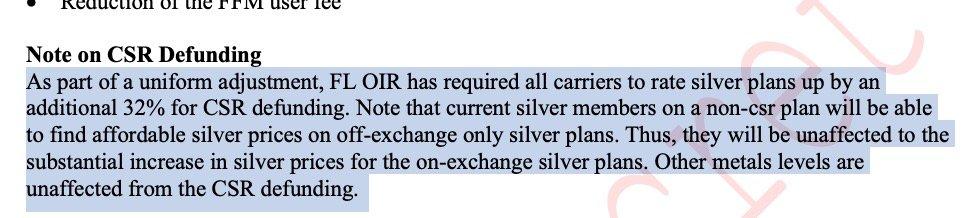

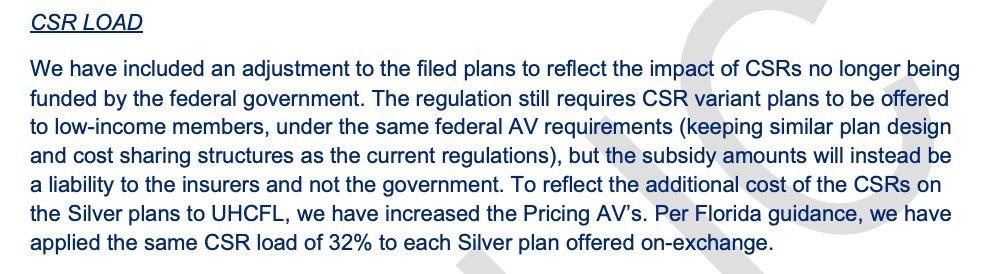

There's also this interesting tidbit which I found in the (otherwise redacted) filings for Florida Health Care Plans and UnitedHealthcare:

It looks like Florida has been quietly doing what other states like New Mexico and Texas are doing: Not just giving a general "Silver Loading" regulation but actually specifying a particular "load" to be tacked on to Silver plans. I checked the 2022 and 2023 filings for both carriers and saw similar "CSR loads" (31% and 33% respectively).

Advertisement