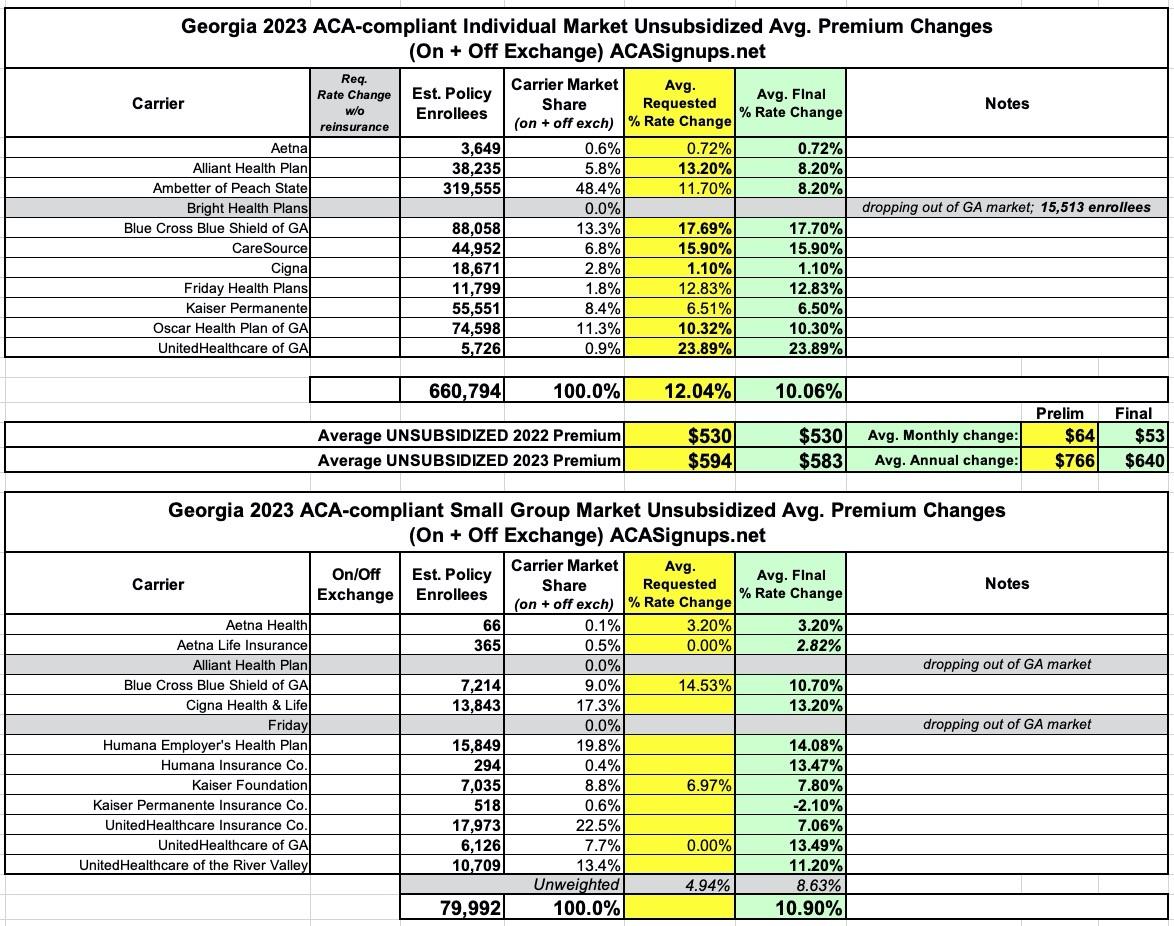

Georgia: Final avg. unsubsidized 2023 #ACA rate changes: +10.1% (down from +12.0%)

Thu, 10/13/2022 - 2:02pm

Georgia's health department doesn't publish their annual rate filings publicly, but they don't hide them either; I was able to acquire pretty much everything via a simple FOIA request. Huge kudos to the GA OCI folks!

A few years ago, Georgia's GOP Governor, Brian Kemp, put in a request to the Centers for Medicare & Medicaid Services (CMS) for what's known as a Section 1332 State Innovation Waiver. If approved, these waivers allow individual states to modify how the ACA operates in their state as long as they can prove that the changes would a) cover at least as many residents b) at least as comprehensively without c) increasing federal spending in the process.

1332 waivers have been used by over a dozen other states, mostly to set up "reinsurance" programs, which reduce the unsubsidized premiums for ACA marketplace policies (but which can, ironically, end up increasing the net cost of ACA policies for subsidized enrollees, depending on how they're funded and structured). However, they can be used in other ways as well. Reinsurance programs can be useful in a world where the ACA's subsidy cliff exists, but won't serve much function if, as I hope, the American Rescue Plan's expanded ACA subsidies are permanently extended.

Georgia's 1332 waiver proposal consisted of two parts. The second part was terrible and has been scrapped for now, thank God. The first part is more or less a standard reinsurance program not too different from other states utilizing such a program, and was given the green light and went into effect this year.

In any event, while the preliminary rate requests for unsubsidized enrollees in 2023 by Georgia individual market carriers was around 12% (ouch), it looks like state regulators have shaved this down a bit to around 10.1%. Still not great, but that's still an average savings of $126/year vs. the requested rates.

The other major news for GA's indy market was announced just yesterday: Bright Healthcare, which had previously been planning on staying in the GA market and was going to bump their rates by a relatively modest 5.7%, is instead pulling out of pretty much the entire individual market nationally, leaving up to a million current enrollees having to switch to a different carrier. Over 15,000 of those folks are in Georgia.

As for Georgia's small group market, two carriers are leaving: Alliant and Friday (the latter of which just entered GA's small group market this year).

I've been informed that Georgia's small group market has been significantly shrunk of late by two things:

Level-funded insurance refers to a health insurance plan in which an employer pays a set premium amount each month to an insurance carrier or Third-Party Administrator (TPA). The insurance company or TPA puts these funds into an account to cover claims, stop-loss coverage premiums, and administrative expenses.

Your monthly premium in a level-funded plan is based on an estimated maximum cost or worst-case claims projection. This projection includes the cost of a stop-loss policy, which limits the financial risk for catastrophic claims. The benefit of this type of health insurance is that if your claims are lower than expected, there is the possibility of receiving a refund at the end of the plan year.

An individual coverage health reimbursement arrangement (ICHRA) is a new type of health reimbursement arrangement in which employers of any size can reimburse employees for some or all of the premiums that the employees pay for health insurance that they purchase on their own. ICHRAs were created under regulations issued by the Trump administration in 2019, and became available as of 2020.

ICHRAs represent a departure from previous ACA implementation rules that forbid employers from reimbursing employees for individual market premiums. QSEHRAs, which became available in 2017, allow small employers to reimburse employees for individual market premiums. But ICHRAs allow this for employers of any size, and they offer more flexibility in terms of how much an employer is allowed to reimburse an employee.

I don't know nearly enough about "level-funded" plans to comment, but ICHRAs essentially boil down to employers shifting their employees over to individual market policies...and while the enrollees don't qualify for any official ACA premium subsidies, both the employer and employee still benefit from the employer-sponsored insurance tax benefits, which means the employer still covers the bulk fo the cost of the plans.

In any event, statewide, small group market rates are going up around 10.9% on average.

Advertisement