New Jersey: Final avg. unsubsidized 2023 #ACA rate changes: +8.8%

Thu, 10/06/2022 - 2:07pm

via the New Jersey Dept. of Banking & Insurance:

NJ Department of Banking and Insurance Announces Expanded Health Insurance Options in 2023, Historic Levels of Financial Help Remain Available at Get Covered New Jersey

TRENTON — The New Jersey Department of Banking and Insurance today announced that consumers shopping for 2023 health coverage this fall at Get Covered New Jersey, the state’s official health insurance marketplace, will continue to benefit from historic levels of federal and state financial help. Consumers will also have more choice with Aetna now offering plans on the marketplace, increasing the overall number of carriers for the second consecutive year.

“Since launching our own health insurance marketplace, the Murphy Administration has been committed to increasing access to quality, affordable health coverage through Get Covered New Jersey,” said Commissioner Marlene Caride. “For the upcoming year, we have expanded the number of carriers offering plans through Get Covered New Jersey to five, up from three in 2020, and will continue to provide record levels of financial help to lower premiums.”

Open Enrollment begins November 1, 2022 at Get Covered New Jersey, which provides a one-stop shop for health insurance for residents who do not have coverage from an employer or other program, and is the only place residents can get financial help to purchase a plan.

The American Rescue Plan Act, signed in March 2021, significantly increased the amount of financial help available to consumers and removed the income cap to receive assistance. President Biden’s enactment of the Inflation Reduction Act earlier this year has preserved these record levels of financial help that have made health insurance through Get Covered New Jersey more affordable for hundreds of thousands of New Jersey residents.

Based on these federal actions, no one pays more than 8.5 percent of their income for health insurance through Get Covered New Jersey (based on a benchmark plan). The continuation of these savings allowed New Jersey to increase the amount of state subsidies available to eligible consumers and to extend the state savings to residents at higher income levels, allowing those earning an annual salary of up to 600 percent of the federal poverty level ($76,560 for an individual and $157,200 for a family of four) to receive state assistance. Both increased federal and state financial help will remain available, and 9 in 10 consumers enrolling will qualify for assistance.

To further bolster affordability, the Biden-Harris Administration is also proposing to eliminate the “family glitch.” If this proposal is finalized, family members of workers who are offered affordable self-only coverage but unaffordable family coverage may qualify for premium tax credits to buy plans on the marketplace.

For 2023, consumers will have more plan choices with Aetna selling plans through Get Covered New Jersey. Aetna will enter the marketplace in 2023, joining AmeriHealth, Horizon Blue Cross Blue Shield of New Jersey, Oscar and Ambetter from WellCare of New Jersey.

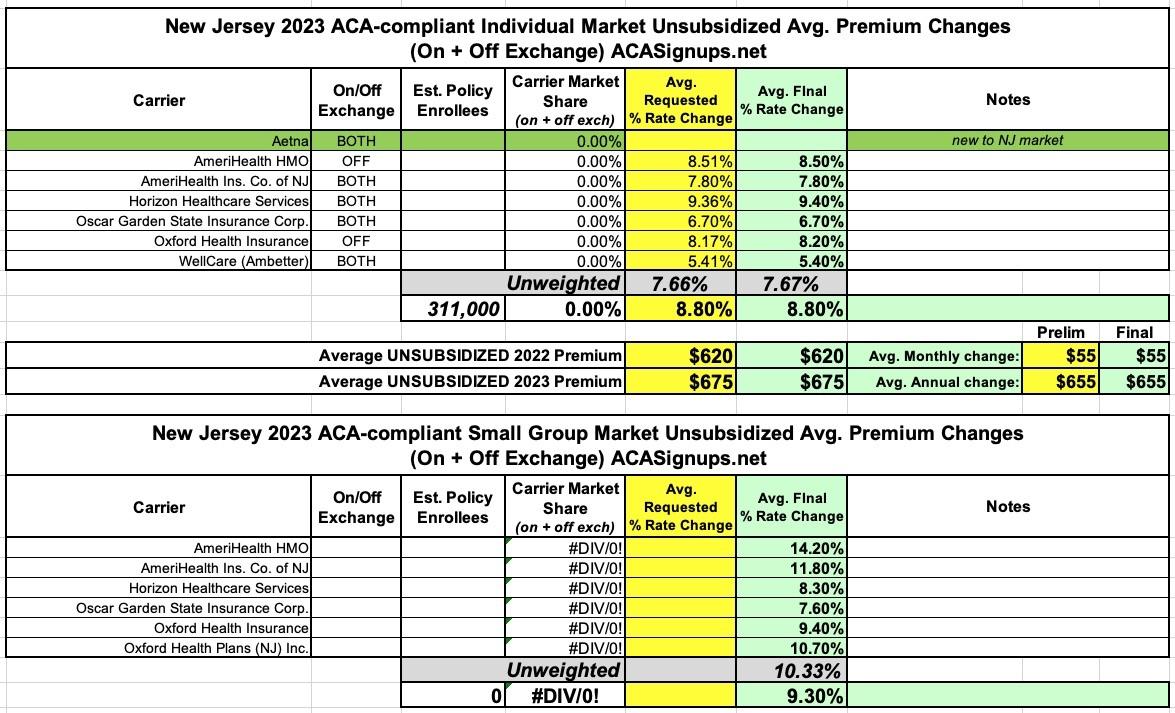

Based on plan rates for 2023 submitted by carriers, rates will increase on average by 8.8 percent over 2022 in the individual market, which includes on exchange and off exchange plans (sold directly by insurance companies) and Small Employer Health Benefits Program rates will increase on average by 9.3 percent over last year. However, thanks to federal and state actions, rates are significantly lower than they would be without efforts to stabilize the market. Rates in the individual market are an additional 15 percent lower than they otherwise would be as a result of the creation of the state’s reinsurance program in 2019, which better manages high-cost health claims. The passage of the Inflation Reduction Act, and specifically the extension of increased levels of financial help, has led to a one and half percentage point reduction on average in marketplace plan rates in New Jersey.

Rate increases in the individual market are attributed largely to an increase in health care costs, also referred to as medical trend, according to information submitted by the carriers. Another key driver of rates was increased medical claims, with utilization of care greater than expected as residents seek healthcare services previously postponed due to the COVID-19 pandemic.

Insurers are required under the Affordable Care Act to use 80 percent or more of premiums for the payment of claims, and to return excess premiums to policyholders. Once the full 2022 experience is available, the department will conduct an analysis and determine if rebates are owed to consumers based on all claims paid in 2022.

Rate filings are submitted to the department by carriers. By law, rate filings in the individual and small employer markets are informational and not subject to prior approval; however, the department may disapprove any informational filing if the department finds that the filing is incomplete and not in compliance with relevant laws or that the rates are inadequate or unfairly discriminatory.

The Open Enrollment Period for 2023 coverage at Get Covered New Jersey (GetCovered.NJ.gov) will run from November 1, 2022 to January 31, 2023. Consumers must enroll by December 31, 2022 for coverage starting January 1, 2023; if they enroll by January 31, 2023, coverage will begin February 1, 2023.

Below is the average total rate action by carrier in the individual market, which includes both on-exchange and off-exchange offerings:

Unfortunately I'm not able to acquire a clear enrollment breakout by carrier; the filings aren't available via the SERFF database, the federal Rate Review database filings are redacted, and even New Jersey's own Individual and Small Group market enrollment reports haven't been updated since December 2020 and June 2021 respectively, making those numbers useless for this purpose.

I'm assuming New Jersey's total current Individual Market enrollment is somewhere around the 311,000 who enrolled during the 2022 Open Enrollment Period, with the off-exchange enrollees being roughly cancelled out by the net attrition of on-exchange enrollment throughout the year.

Advertisement