Quick Tip: How much of your health insurance premium is your employer paying?

Sun, 10/06/2019 - 12:20pm

A huge part of the controversy about "pure" Medicare for All is tied to the fact that nearly 50% of the population (roughly ~160 million Americans, give or take) currently receives healthcare coverage via their employer. Some of this Employer-Sponsord Insurance (ESI) is pretty damned good, while some of it kind of sucks, but that's how our absurd system currently works for good or bad.

Anyway, most employers cover the bulk of the premiums for their enrollees...but a lot of people (my guess is the vast majority) either have no clue that they do so or at best have no idea how much of their monthly premiums are covered for them by the employer.

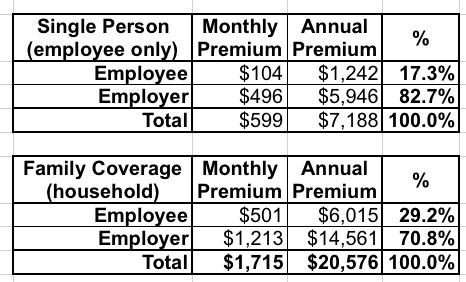

The breakout between the employee and the employer varies widely by company, but according to the Kaiser Family Foundation, as of 2019, the national average is:

As you can see, nearly half the country is scratching their heads, wondering why the plans advertised at HealthCare.Gov are officially listed as costing $600/month or more when they're "only paying" a couple hundred bucks per month apiece. If you forget about your employer covering the bulk of the premium, this confusion makes total sense.

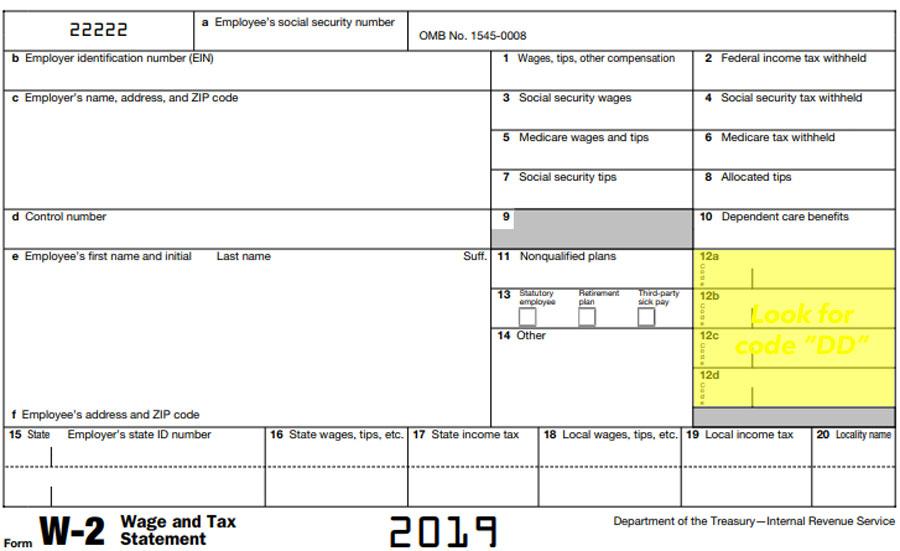

One small but important provision of the Affordable Care Act which even I didn't know about until recently (since I'm self-employed and on the Individual market) is that it requires the employer's portion of the premium to be listed in a special box on the employee's W-2 form:

Employers: The Affordable Care Act requires employers to report the cost of coverage under an employer-sponsored group health plan on an employee’s Form W-2, Wage and Tax Statement, in Box 12, using Code DD.

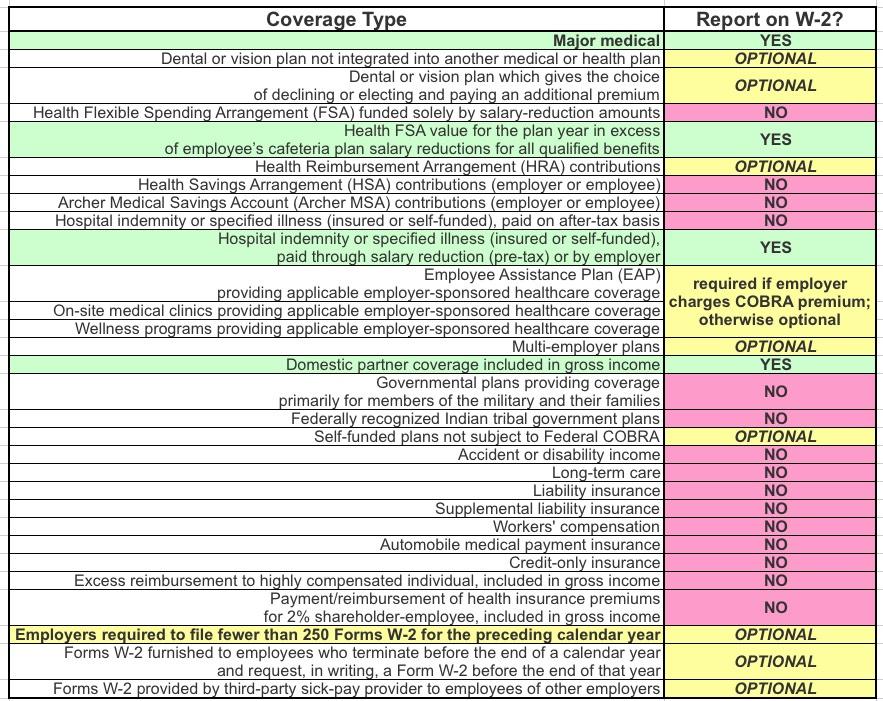

...More information about the reporting, and which employers are, or are not, required to report this on the Form W-2 can be found on the Form W-2 Reporting of Employer-Sponsored Health Coverage page.

Individuals and Families: Individuals (employees) do not have to report the cost of coverage under an employer-sponsored group health plan that may be shown on their Form W-2, Wage and Tax Statement, in Box 12, using Code DD.

The amount reported does not affect tax liability, as the value of the employer contribution continues to be excludible from an employee’s income, and is not taxable. This reporting is for informational purposes only, to show employees the value of their health care benefits.

So the next time you look at the ACA's high premiums for the individual market (they're gonna average around $595/month per person next year for a Silver plan which covers 70% of your medical expenses...aka the "actuarial value" of the policy), keep in mind that the average employer plan actually averages $4 more per month per enrollee.

Of course this is kind of an apples to oranges comparison for two major reasons:

One way to measure the generosity of health insurance is actuarial value: the percentage of the total average cost for covered benefits that a plan pays. Generally, a higher actuarial value indicates a health plan is shouldering more of the cost of care. On average, employer plans cover 85% of enrollees’ in-network expenses in 2017, leaving plan enrollees to cover the remainder in cost-sharing. Since 2003, employer plans have covered between 85% and 86% of enrollee costs.

A fairer comparison here would probably be to measure the ACA's Gold plans (which have an 80% AV rating) against ESI coverage. According to HealthPocket, the average Gold Plan premium for ACA coverage runs around 45% higher than the average Silver plan, which means they should average roughly $863/month for a single adult.

- Second, employer plans often have wider provider networks than ACA policies.

I'm not sure what the best way to quantify this would be...presumably I'd have to look at the average premiums for Gold PPO plans vs. Gold HMOs...and I'd also have to separate out the number of HMO and PPO ACA enrollees as well, since that $863 includes both mixed together.

An HMO looks to reduce costs by having a more restricted provider network. Your premiums on these plans will typically be less expensive. In 2016, the average annual premium for an employer-sponsored HMO family plan was $17,978, according to the Kaiser Family Foundation. A PPO plan cost $19,003, more than $1,000 higher per year.

I'm not sure if that translates closely to individual market PPOs vs. HMOs, but if it does, that suggests that the average Gold Individual Market PPO should run roughly $915/month for a single enrollee, or around 50% more than a comparable-quality ESI plan.

Of course, if you're on an individual market plan and earn less than 400% FPL (roughly $50,000 if you're single or $100,000 for a family of 4), you also qualify for financial subsidies...and if you earn less than 250% FPL, you qualify for additional subsidies to bring the AV rating up from 70% to as high as 94%. The problem, once again, is that people who earn more than 400% FPL receive bupkis, since they don't qualify for any assistance whatsoever.*

This is a problem which desperately needs to be addressed by passing H.R. 1868 (the flagship portion of the House Democrats' ACA 2.0 bill) and by upgrading the benchmark premium from Silver to Gold (which is included in Elizabeth Warren's CHIPA bill, Joe Biden's healthcare bill and Pete Buttigieg's "Medicare for All Who Want It" bill).

*UPDATE: As Ken Kelly points out in the comments below, my statement above isn't technically true for everyone over 400% FPL...if you're self-employed on the individual market, you can deduct 100% of your portion of your healthcare premiums from your federal tax return, along with some other oddball potential deductions. This has nothing to do with the ACA, mind you; the law allowing 100% premium deduction for self-employed folks dates back to 2003.

For instance, let's suppose you're a single adult, no kids, with a MAGI of $60,000/year after taking all of your other deductions. Normally you'd owe $9,058 in federal taxes.

However, let's assume that you were enrolled in an ACA policy running $600/mo last year. Since you're over the 400% FPL subsidy threshold, you had to pay the full $7,200.

If you're self-employed, however, you get to deduct all $7,200, bringing your taxable MAGI down to $52,800...which means your federal taxes are $7,474 instead; you just saved $1,584, or 22% of your premiums.

As Louise Norris notes in her excellent explainer, due to how the ACA Subsidy Cliff works, this can also lead to some strange circular math if your income is close to the 400% FPL Subsidy Cliff. Here's how:

Take the exact same situation I just described, but reduce the income to exactly $55,000. You're still just barely over the 400% cut-off of $49,960, so you don't qualify for any subsidies...except that if you deduct the $7,200, suddenly your MAGI is only $47,800...just 383% FPL. Hooray, you do qualify for ACA subsidies after all!

Assuming you're enrolled in the benchmark Silver plan, you should receive $2,487 in subsidies...except, of course, that pushes your MAGI back over the 400% cut-off again!

Fortunately, Norris also has an explainer of two methods the IRS provides to resolve this seeming Catch-22.

UPDATE: Thanks to Michael Capaldo for pointing out that employers aren't always required to report their portion of ESI premium contributions on W-2s...the most important exception being employers who file fewer than 250 W-2's per year (which isn't quite the same as having fewer than 250 employees):

Advertisement