Fun with Risk Corridor Payments: One lucky Texan could get rebate checks for $982 million!*

Wed, 06/26/2019 - 12:10am

*(OK, probably not, but...well, read on...)

Regular readers may have noticed that I didn't post a single blog entry on Tuesday even though there's been a ton of healthcare policy stuff going on. No, I didn't take the day off; I started poring over a spreadsheet at around 10am and was working on it almost nonstop all day.

On Monday, along with posting their decisions on several important federal cases, the U.S. Supreme Court announced that, much to the surprise of many healthcare wonks, they will take up the long-gestating (and presumed dead) Risk Corridor Massacre lawsuit:

Big news: SCOTUS is taking up the ACA risk corridors case. GOP's decision to stymie that program arguably did the most damage to the ACA marketplaces. https://t.co/VeMRcd5MYn

— Bob Herman (@bobjherman) June 24, 2019

As previously noted, the various Risk Corridor lawsuits had originally been assumed to be slam dunk cases: The United States Federal Government contractually and legally owed several hundred health insurance carriers billions of dollars via the ACA's "Risk Corridor" stabilization program, which was supposed to be active for the first 3 years of the ACA exchanges, from 2014 - 2016.

I gave a more in-depth explanation in my previous post, but the bottom line is that for the first 3 years, insurance carriers which did unusually better than expected were required to pay a portion of their profits into a central fund, while carriers which did unusually worse than expected were promised partial reimbursement via that same fund. If the amount put in was greater than the amount paid out, the government would keep the difference. If the amount owed was greater than the amount brought in, the federal goverment was supposed to pay the difference.

Halfway through the first year of the program, however, congressional Republicans insisted that the rules of the Risk Corridor program be changed in such a way that if there was a shortfall in the fund, the "losing" insurance carriers were essentially S.O.L...and that's exactly what happened.

- In 2014, around $362 million was paid into the fund...but it owed nearly $2.87 billion.

- In 2015, only $95 million was paid into the fund...but it owed over $5.8 billion.

- In 2016, a mere $25 million was paid in...while it owed almost $4 billion.

In late August 2015 (I believe), the federal goverment paid 12.6 cents on the dollar for 2014 ($362 million / $2.87 billion = 12.6%). This, along with some other factors, led to financial ruin for nearly 20 smaller startup carriers, most of which didn't have the cash reserves to help them weather the Risk Corridor storm. I wrote obituary blog entries for yet another victim of the Risk Corridor Massacre weekly between August and November 2015...in a few cases, two of them went bankrupt the same day.

The larger carriers, with massive cash reserves were able to absorb their losses--in some cases totalling hundreds of millions of dollars--while they filed class action lawsuits to force the federal government to pay up. Again, I went into the backstory of this mess on Monday.

The bottom line is that a year after everyone thought the suit was dead and the carriers would have to kiss over $12 billion goodbye forever, the Supreme Court announced that they're gonna hear the case after all.

On Tuesday morning, however, Dave Anderson posted something which caught my attention:

#SCOTUS #RiskCorridors #MedicalLossRatio #MLR rebates are at stake if the insurers win their case to recover $12 billion in #ACA payments from the federal government for 2014-2016 https://t.co/R400VynbD2@bobjherman @nicholas_bagley @xpostfactoid @charles_gaba @LouiseNorris

— David Anderson (@bjdickmayhew) June 25, 2019

When I first read about this on Monday, I assumed that if SCOTUS ends up ruling in favor of the insurance carriers and orders the government to pay up, it wouldn't be that big of a deal for anyone else. That is, I figured it'd be a tidy windfall for the carriers and their shareholders, but I also assumed that the revenue would simply be officially recorded in their 2014-2016 books and that'd be that. It isn't going to bring the bankrupt carriers back from the dead, unfortunately...their creditors will be happy, of course, but those 20-odd Co-Ops and other small insurers have been dead & buried for several years now.

Let’s assume the insurers win a full judgement in their favor and the US judgement fund starts cutting $12 billion dollars worth of checks a month after the decision.

There are two classes of insurers to consider; the living and the dead.

For insurers that are still an ongoing concern, not much happens. it depends on how the cash falls on the balance sheet. If the cash of an award is attributed to the years where the risk corridor losses were accrued, not much happens. For example, my former employer, UPMC Health Plan is owed over $60 million dollars for just 2016 losses. If they get a $60 million check in the spring of 2020, the accountants have to re-adjust the 2016 books and that is about it. A $60 million swing may affect bonus and perhaps Medical Loss Ratios. It is a lump sum windfall that does nothing to alter future decision making. At the smallest and most thinly capitalized surviving insurers, a lump sum windfall may rebuild capital reserves from low to high levels which may have incremental downward pressure on future premiums, but that is a bank shot of a move.

It was Anderson's mention of Medical Loss Ratios which perked my interest:

Wait...the RC $ would count towards MLR rebates? For which years, though? 2014-2016?

— Charles Gaba (@charles_gaba) June 25, 2019

Anderson almost immediately added an update to his post:

Update 1 However, risk corridor money has been treated on a cash basis. This means that an insurer that received 12.3% of the 2014 obligation in 2015 put that money onto their 2015 books instead of their 2014 books. If this holds, then there would be a huge bolus of money hitting 2020 books and thus hitting the 2018-2020, 2019-2021, and 2020-2022 MLR calculations without any underlying claims. This would significantly flow back to current year consumers as larger rebates and lower premiums. (End Update 1)

Let's go back and review how Medical Loss Ratios work:

- Under the Affordable Care Act, insurance carriers are required to spend at least 80 - 85% of their premium revenue on actual medical claims (80% for the Individual and Small Group markets; 85% for the Large Group Market).

- The Risk Corridor program only impacted the Individual and Small Group markets, so 80% is the percent to keep in mind.

- If they spend less than 80% on claims in a given year, the difference must be rebated to the policyholders.

- This has resulted in several billion dollars being paid out to millions of ACA enrollees and/or small business owners over the past 8 years (that's right...the MLR rule started out way back in 2011, three years before the ACA exchanges were even up and running!)

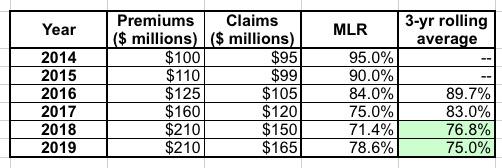

It's important to keep in mind that the MLR rule works on a 3-year rolling average basis. For instance, let's say a carrier brings in $100 million in 2014, $110 million in 2015 and $125 million in 2016. Let's also say that their medical claims totalled $95 million in 2014, $99 million in 2015 and $105 million in 2016, like so (the table below isn't too far off from the actual trend in both premiums and claims over the past six years:

Their MLR was way too high the first two years...in fact, they lost money in 2014 and probably in 2015 as well, since administrative overhead/etc. costs more than 5%. things started to stabilize in 2016, and starting in 2017 they actually overshot the mark. In 2018 they seriously overpriced, so they instituted a price freeze in 2019.

The three-year average for 2014-2016 is nearly 90%, and for 2015-2017 it was still above 80%, so they didn't have to pay back any rebates. For 2016-2018, however, they fell below 77%, so they'll have to cut checks to their enrollees later this year, and they'll have to cut slightly larger checks next summer as well, since the 3-yr average is down to 75%.

To give you an idea about how much money we're talking about, here's how much was paid out in MLR rebates to Individual market enrollees over the years:

- 2011: $1.1 billion nationally (breakout not available)

- 2012: $519 million to 8.8 million people ($59/apiece on average)

- 2013: $332 million to 6.8 million people ($49/apiece on average)

- 2014: $469 million to 5.5 million people ($85/apiece on average)

- 2015: $396 million to 4.8 million people ($82/apiece on average)

- 2016: $446 million to 4.0 million people ($113/apiece on average)

- 2017: $706 million to 6.0 million people ($119/apiece on average)

The 2018 payments won't be announced until sometime in August or September, I'd imagine, but I expect them to be pretty large possibly up to $200 or so on average?...and 2019's will likely be larger still, paid out in summer of 2020. (NOTE: Not every carrier has to pay MLR rebates every year, and the amounts vary widely. The whole point of the program is to encourage carriers not to price gouge by keeping their premiums, and therefore their profit margins, within a limited range. I've been enrolled in an ACA exchange plan since 2014 and I've never received a rebate check yet, though I do know a few people who have).

OK, so what's all this have to do with the Risk Corridor Massacre and the impending Supreme Court Case?

Well, did you notice anything about the dollar amounts above? They range from around $400 million/year up to $1.1 billion nationally.

If the Supreme Court rules in favor of the plaintiffs, and if they order the federal government to pay out the years-past-due Risk Corridor funds, that will likely mean a whopping $12 billion windfall being dumped into the laps of several hundred insurance carriers around the country all in one shot.

As Dave Anderson noted, a lot depends on how that income is categorized by the carriers, but if it gets counted as 2020 premium revenue, that means any insurance carrier which is already hovering around the 80% MLR threshold could very well have to pay a large chunk of that money to their enrollees...likely in August of 2021, since SCOTUS probably won't even hear the case until next year.

Again, none of this is guaranteed. SCOTUS might shoot down the lawsuit, in which case nothing changes. They might rule for the plaintiffs but include some unusual rules about how the risk corridor payments are made or accounted for. Who knows?

But if everything falls into place as I've described here, we could be talking about some pretty hefty rebate checks in 2021...all thanks to the Affordable Care Act, otherwise known as Obamacare.

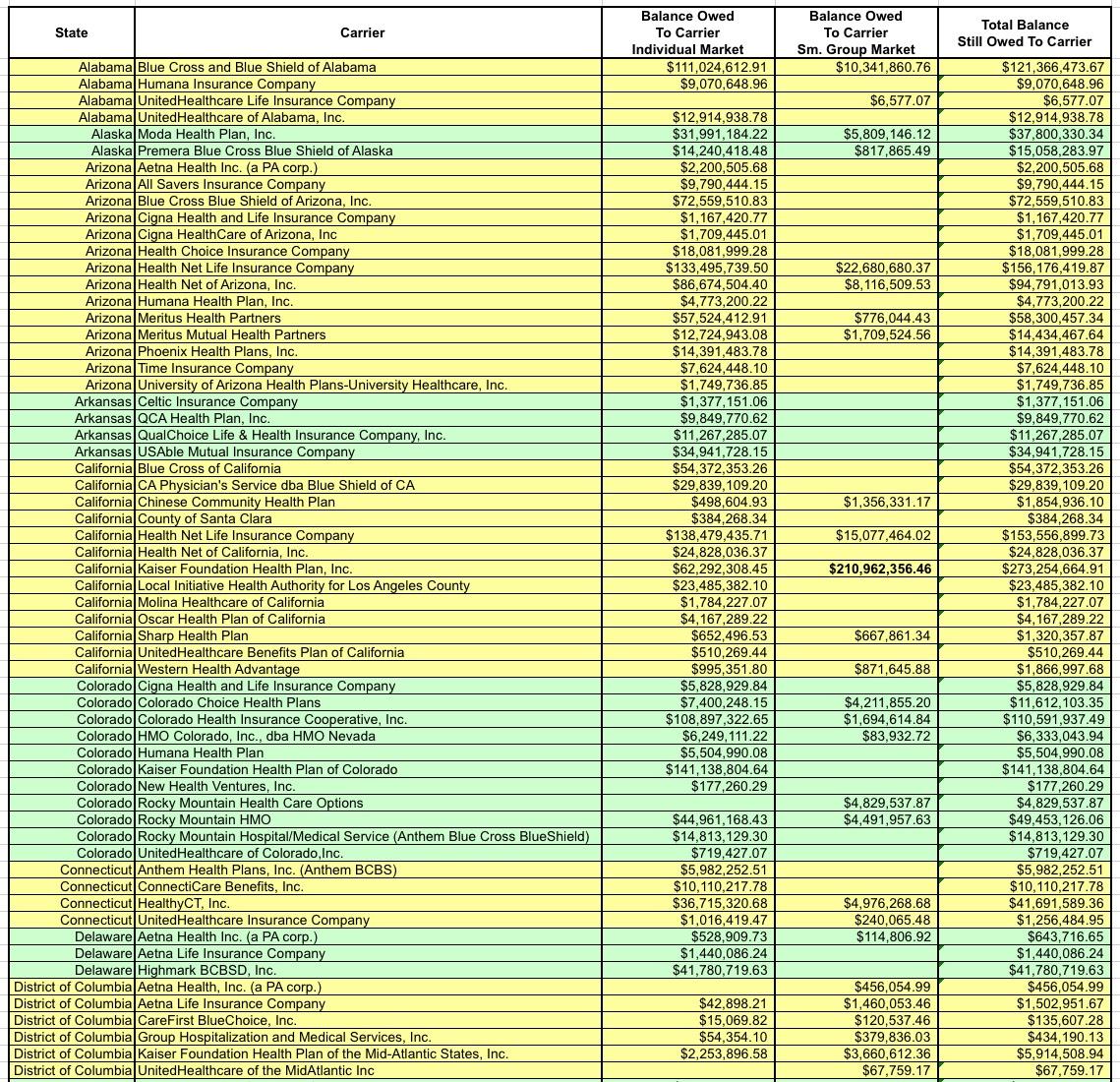

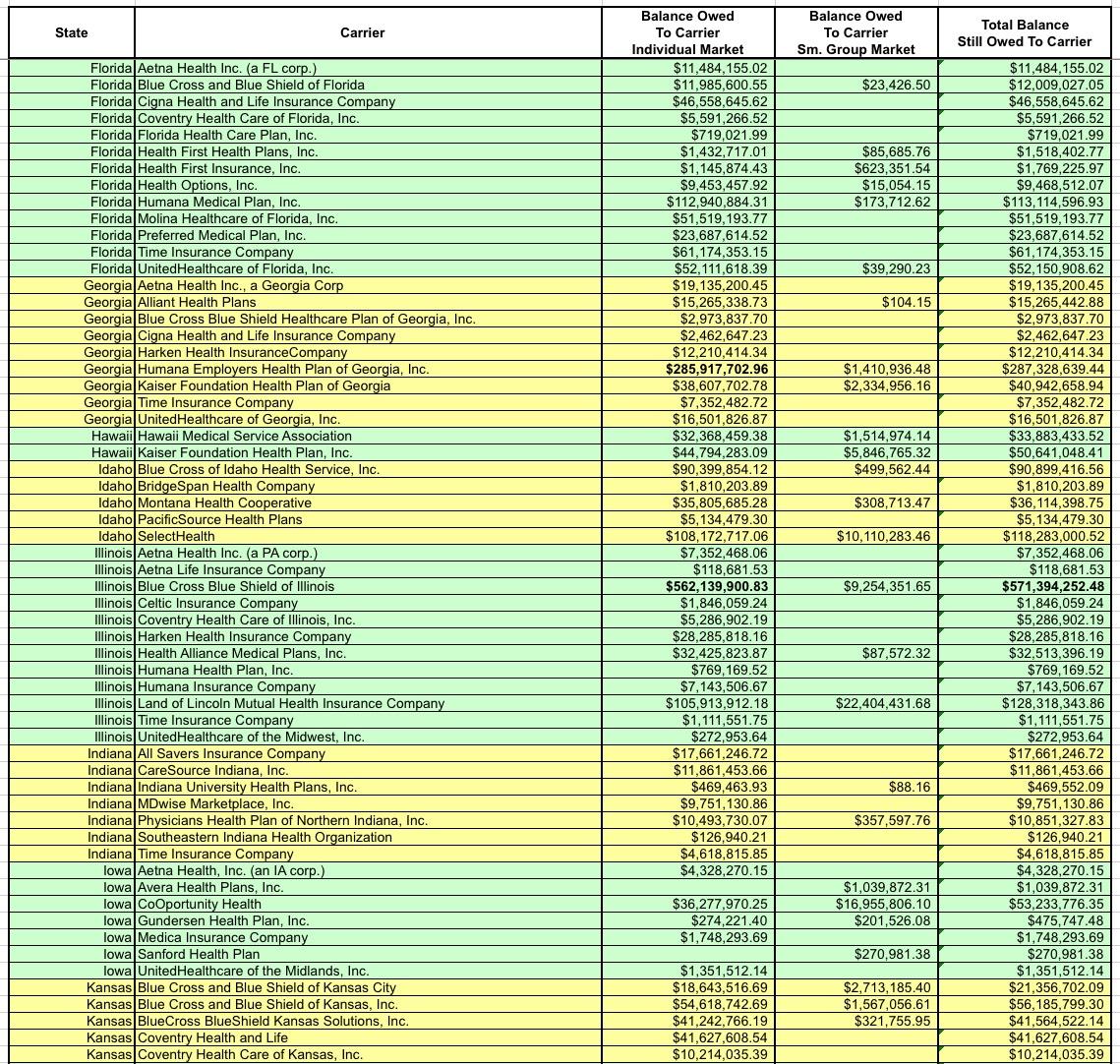

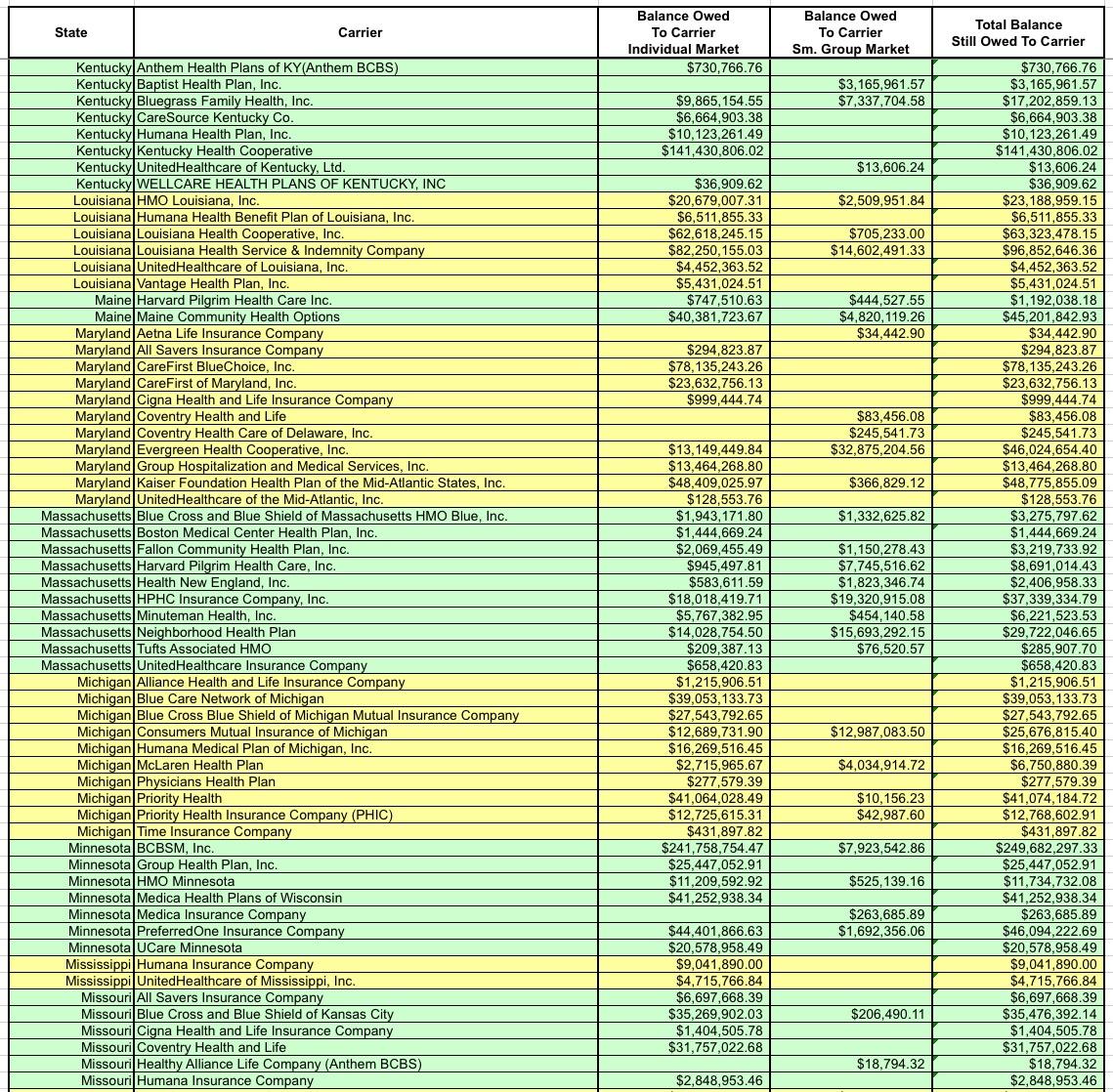

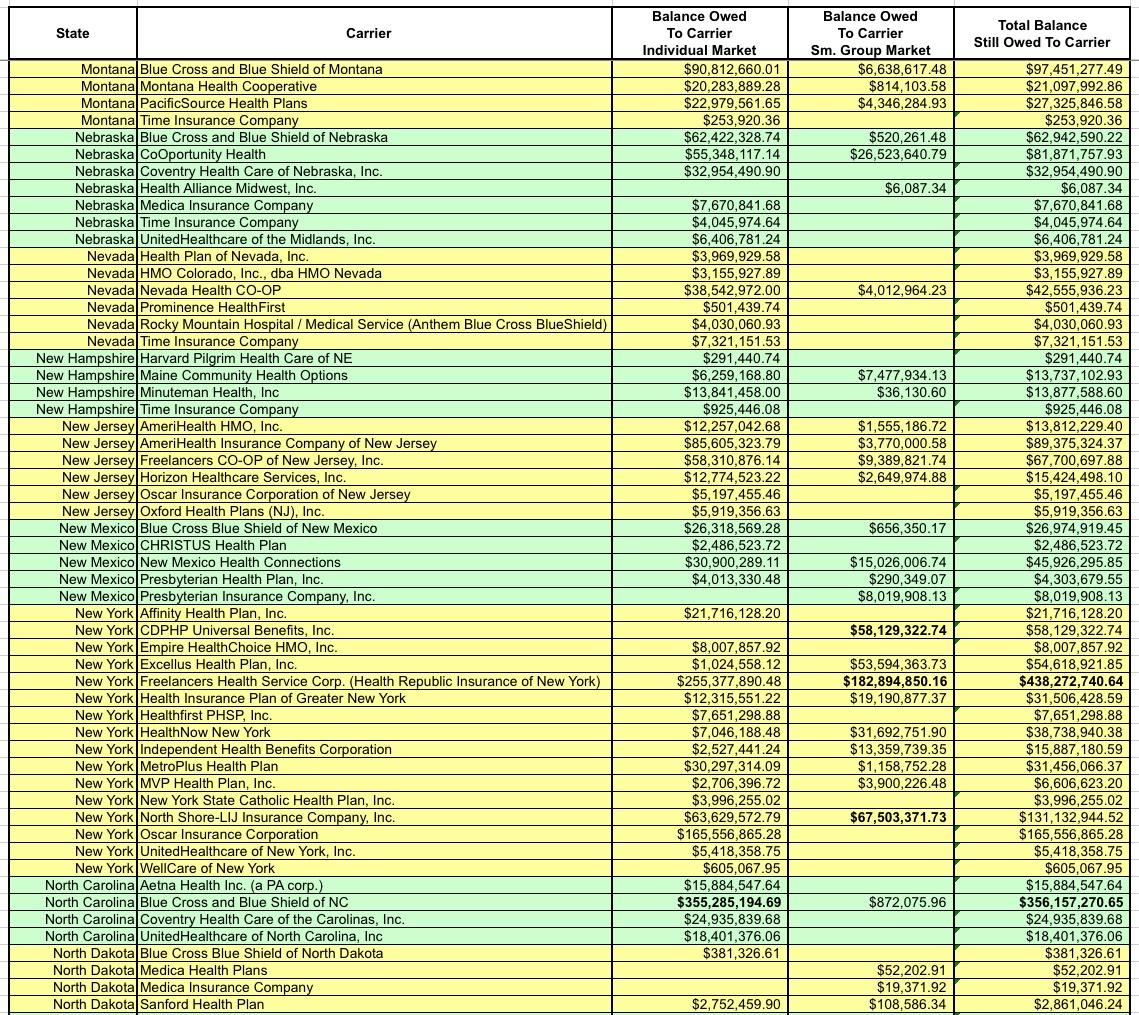

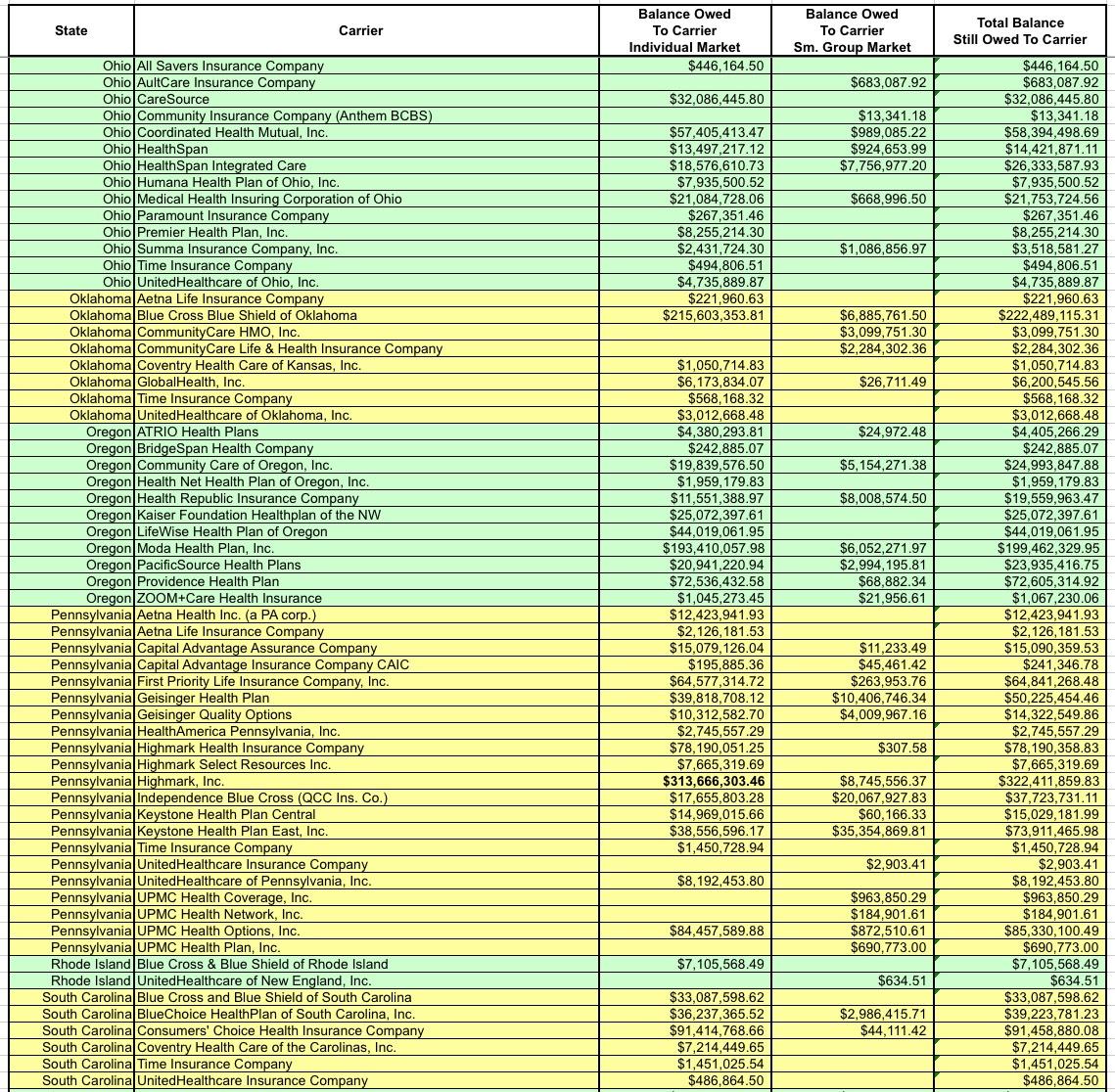

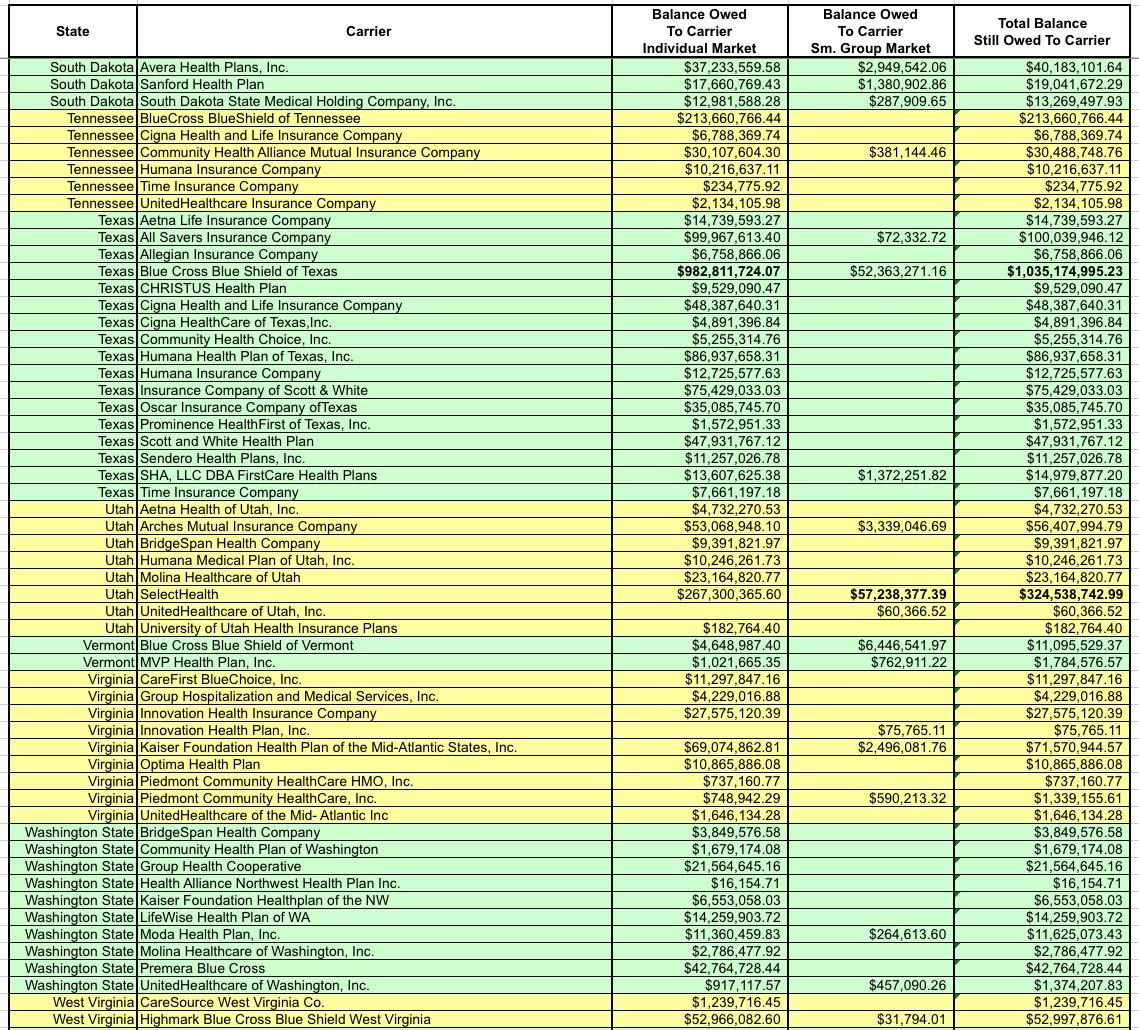

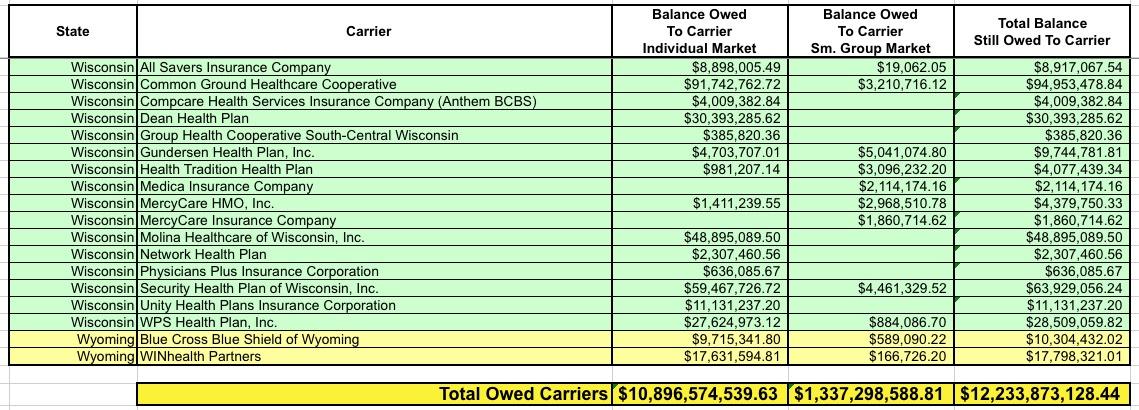

How large? Well, that's what I spent all day Tuesday slaving over a hot spreadsheet to figure out. Here's the raw Risk Corridor tables for 2014, 2015 and 2016. They're broken out by state, by individual & small group market, and by how much each insurance carrier had to pay into the fund as well as, more importantly, how much they were owed for each year.

Oh yeah...and as you can also see, they're only available in static PDF format.

So what did I do? Yes, I copied and pasted the entire thing into plain text format, then spent hours cleaning up the formatting, converting spaces into tabs and so forth to prepare all three of them to be entered into Excel.

After wrestling with the formatting some more and cleaning everything up, I think I've successfully boiled it down to the following (click images for full-size versions):

I've bold-faced the five highest dollar amounts in each category (Individual Market, Small Group Market and Total):

- Individual Market: BCBS Texas; BCBS Illinois; BCBS North Carolina; Highmark (Pennsylvania); and Humana (Georgia)

- Small Group Market: Kaiser Foundation (California); Health Republic (New York); North Shore-LIJ (New York); CDPHP (New York) and SelectHealth (Utah)

- Total: BCBS Texas; BCBS Illinois; Health Republic (NY); BCBS North Carlina and SelectHealth (Utah).

I noted earlier that a good twenty or so carriers have actually gone bankrupt...including Health Republic of NY. I assume their risk corridor payment would go to pay back the creditors. A few others have merged with or been acquired by other carriers; I have no idea how that will be handled.

Not only is Blue Cross Blue Shield of Texas owed more risk corridor money than any other carrier, it's not even close--they're owed over $1 billion, nearly twice as much as BCBS Illinois ($571 million). Nearly all of that consists of the $982 million BCBSTX is owed for their Individual Market business.

I don't know how many Indy market enrollees BCBSTX will have in 2020, but as of last year I have that number down as 390,000 Texans. IF that proves to be accurate, and if BCBSTX gets their $982 million, and if their MLR was already at or below the 80% threshold over the next 3 years, that would mean enrollees would receive three checks totalling around $2,500 apiece. NICE!

But wait, there's more!

Guys, it gets even weirder! Some of the issuers who could get big RC receivables are barely even in there individual market anymore. So the enormous rebates could be getting paid out to a TINY number of residual enrollees.

— Christen Linke Young (@clinkeyoung) June 25, 2019

Wait…so that means if they had, say, 30,000 #ACA enrollees in 2014-2016 owed a total of $3 million, but only 300 are enrolled today, those 300 people get $10,000 apiece? Good grief.

What happens if they’ve since pulled out completely, though?

— Charles Gaba (@charles_gaba) June 25, 2019

Don't get me wrong: I realize that Blue Cross Blue Shield of Texas is not likely to pull up stakes. Nor are they likely to pare down their individual market enrollment by 99% (although they did completely cut out all indy market PPO policies back in 2015, kicking 367,000 enrollees to the curb...and from the table above, it's pretty clear why)...

...but what if they did?

What if they only have 240,000 enrollees next year? Each of them could be looking at $4,100 in rebates.

What about 100,000? They might each receive $9,800.

And what about...well, you read the headline.

OK, that's absurd...but so is everything else surrounding ACA lawsuits, so what the hell?

Advertisement