Bloomberg family profile is both sympathetic and infuriating at once

Tue, 11/13/2018 - 5:31pm

Over at Bloomberg News, Aziza Kasumov has written up what is, for the most part, an excellent profile of a middle-class family who crystalize the single biggest real flaw in the design of the Affordable Care Act (as opposed to the bullshit ones made up by opponents over the years): Those enrolled in individual market policies who earn more than 400% of the Federal Poverty Level (around $48,000/year for an individual, or $98,000 for a family of four):

David and Maribel Maldonado seem the very definition of making it in America. David arrived in the U.S. from Mexico as a small child...His wife Maribel, whose family is also from Mexico, worked as a hairstylist while caring for the couple’s two children. David’s annual salary reached about $113,000 by the time the children were in their teens. It was more than enough to live in a pretty suburban house outside Dallas, take family vacations, go to restaurants and splurge at the nearby mall. And to afford health insurance.

The bold-faced bit above has some relevance later in the story.

Then, in 2012, Maribel discovered she had breast cancer. “Your world comes crumbling down,” David says.

Maribel had a double mastectomy, paid for by the insurance David obtained through his job, a small welding business with fewer than a dozen employees.

But two years into Maribel’s recovery and treatment, David’s boss gathered his staff into his office. Don’t worry, he said, business is good. Your jobs are safe. But there would be one change: Health insurance offered through the company would soon be discontinued. It had simply become too expensive for the small company to provide it.

For David, the responsible head of a thriving middle-class family, having health insurance was non-negotiable. But the coverage he found to replace the company plan cost $1,375-a-month, up from the $260 a month he had been paying. Suddenly, the family’s health insurance tab “was more than what we were paying for our mortgage,” David says.

Whenever healthcare pundits and reporters write about those earning less than 100% FPL in states which haven't expanded Medicaid, they refer to that population as being caught in the "Medicaid Gap". I hereby propose that we start referring to those earning over 400% FPL who aren't covered by Medicare or employer insurance as being caught in the "Unsubsidized Gap".

Overall, it's a very well-written article, but there's one important omission in the paragraph above which was flagged by Louise Norris:

Caveat: He compares his unsubsidized indiv. market premium to what he used to pay for employer-sponsored insurance, which was only $260/month.

But the employer was paying most of his insurance premium. Avg ESI family premium in 2016 was $1,511/month https://t.co/snoq4nixvL https://t.co/UWZlTXEZxv

— Louise Norris (@LouiseNorris) November 13, 2018

Assuming "two years" into her recovery from cancer diagnosed in 2012 means 2014, that means the Maldonado's ACA policy cost $1,375/month as of 2015...likely around 9% less than the actual cost of the Employer-Sponsored Insurance (ESI) policy which their employer had discontinued offering.

Assuming the ESI policy was roughly 6% less expensive the prior year (perhaps $1,425/mo), that means David's employer had been covering over 80% of the cost before they stopped offering it, or $1,165/month...roughly $14,000/year.

Did his boss increase David's salary by $14,000/year in return? Apparently not...and that wouldn't make much sense anyway, since the whole point of discontinuing the employer insurance was that he couldn't afford to keep doing so.

Put another way, Mr. Maldonado's employer effectively cut his pay by $14,000 per year.

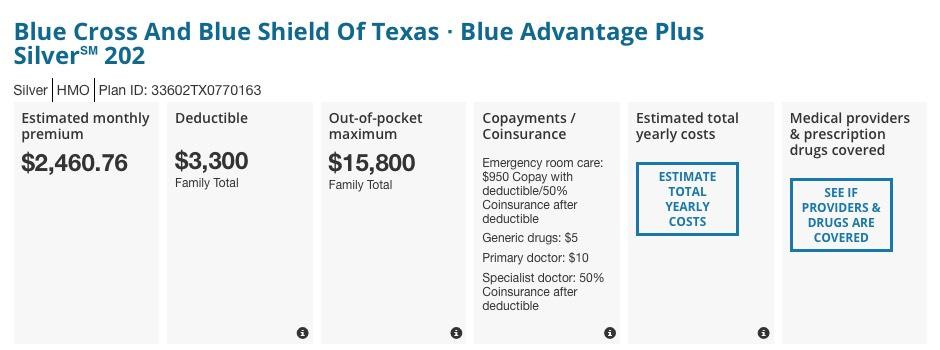

This article is supposed to be sympathetic towards the Maldonados, and most of it absolutely is--they are very much caught in the "Unsubsidized Gap" of people who earn more than 400% FPL and therefore don't qualify for financial assistance. I did a little checking for 2019 using the information provided in the article (he and his wife are 49 & 48, two teenage children, living in Dallas, Texas). Here's what one of the two Blue Cross Blue Shield Silver ACA policies would cost them for next year (the other BCBS Silver plan was close to this):

Ouch indeed...that's nearly $30,000/year, or a whopping 26% of their income.

Of course, roughly $2,400 of that is due specifically to the ACA's individual mandate being repealed and #ShortAssPlans being expanded by the Trump Administration, while another $2,700 or so was due to Trump's CSR cut-off last year, for a total likely Trump/GOP-created premium increase of over $5,000/year for this family.

In a universe where the ACA was the same as it is today except for the assorted Trump/GOP sabotage of the past two years, the policy would cost the family around $25K instead of $30K...much better, of course, but still nearly 22% of their income.

Now, how much would it cost if the 400% FPL cap for APTC assistance was removed?

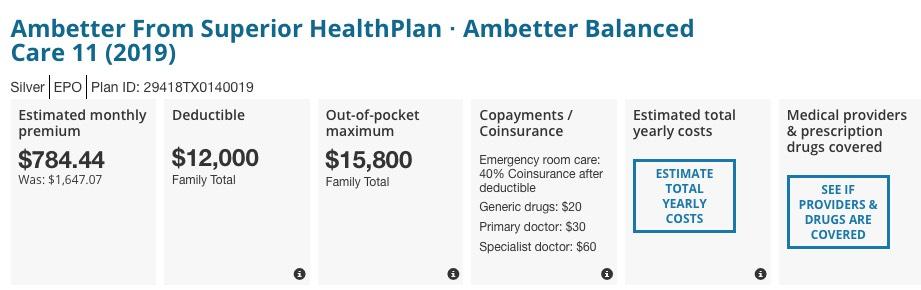

Well, 100% FPL will be $25,100 for a family of 4 next year, so 400% would be $100,400. If they earned $100,399 they'd qualify for $863/month in tax credits, or $10,356 for the year. As far as I can tell, the benchmark plan in Dallas is this one from Ambetter:

$1,647.07 x 12 = $19,765/year. Assuming you removed the 400% FPL cap, the family wouldn't have to pay any more than 9.6% of their income for the benchmark plan, or $10,848 for the year. That means they'd still qualify for around $8,917 in subsidies, or $743/month.

Put another way: Removing the 400% FPL cap would restore at least 2/3 of the subsidies which the family used to receive from David's employer...before they stopped offering coverage due to it being too expensive.

The family income was too high to qualify for financial aid, so the Maldonados began borrowing the roughly $13,000 a year they needed to cover their savings gap for Cristian’s tuition during his college years. Then, a few weeks before the 2016 presidential election, David received a letter from his insurer, Blue Cross Blue Shield of Texas, Inc., announcing a 38 percent increase in premiums for the upcoming year. His monthly premiums would shoot up to almost $1,900.

That’s the day David says he decided to vote for Donald Trump.

On the one hand, as a self-employed, middle-class suburban family man enrolled in an ACA plan myself, I feel David's financial pain, believe me: As I've written many times before, my own family is being squeezed terribly by the unsubsidized cost of ACA policies as well. Our income varies widely from year to year, crossing over and under the critical 400% FPL threshold, which means that a $1 difference in it could potentially mean the difference between saving or spending a whopping $4,800 per year.

However, 1) Trump was clearly lying through his teeth about his intentions regarding healthcare policy in 2016, and 2) David Maldonado was born in Mexico, which means that there's a damned good chance that Trump's racist, xenophobic immigration policies will end up with him being deported even as a naturalized citizen.

Having said that, let's get back to the main point of the article. I might be willing to forgive the "$260/month" error if it didn't explicitly come up again later on:

David has trouble accepting that, just a few years ago, he was paying merely $260 a month for the entire family’s coverage. “If something happens to me, who’s going to pay the bills?” He briefly considered getting health care in Mexico, but the idea quickly fizzled. “If I were closer to the border, I would go to Mexico every time,” he says. “It’s about eight to nine hours driving. It would be cost-ineffective.” But not impossible: He holds dual citizenship, while his wife and children are eligible for Mexican passports. Still, it wouldn’t be an easy road. “It’s a process and it’s paperwork—and anything with the Mexican government, they make it so complicated,” David says. Plus, he’s wary of the quality of care and availability of care under Mexico’s socialized medical system. “It’s fine if you break an arm,” David says, “but if you have anything big, you’re going to be put on the waiting list.”

He "has trouble accepting it"? I don't mean to sound heartless here--again, my own family is at risk of being in the same situation ourselves depending on the year--but the answer again is that his employer was paying around 80% of his family's coverage until 2015.

He's considering going to Mexico for treatment because it's so much less expensive for really expensive services...but then complains about being put on a waiting list for those services...which make the final paragraphs of the article even more telling:

The midterm elections have only reinforced David’s sense that Washington isn’t up to the task of improving the family’s health-care options. He’s still a firm Trump supporter...David was relieved to see the candidate he voted for prevail over Democrat Beto O’Rourke, who ran on a platform that listed single-payer health care as one of its cornerstones.

“I’m all for health care for all,” David says, “but I’m also realistic. Where are you going to cut the money to pay for that?”

So, to summarize, David Maldonado...

- was born in Mexico, meaning Trump wants to deport him...but strongly supports Donald Trump.

- likes Mexico's inexpensive healthcare services but complains that too many other people use them as well

- wants everyone to have healthcare coverage as long as he doesn't have to pay for it himself.

I absolutely sympathize with Mr. Maldonado and his family...but it'd be easier to do so if he understood that:

- his employer effectively cut his annual income by $14,000/year in 2015, which means he's lost roughly $60,000 over the past 4 years.

- if you want everyone to have healthcare coverage, that means everyone is going to utilize healthcare coverage.

- Donald Trump wants to, and very well might, deport him.

Meanwhile, there's a simple solution to most of the Maldonado's woes: REMOVE THE 400% FPL APTC CAP.

Advertisement