Prove Me Wrong, America: 4.5 MILLION UNINSURED PEOPLE qualify for FREE Bronze plans in 2018.

Fri, 11/17/2017 - 1:02am

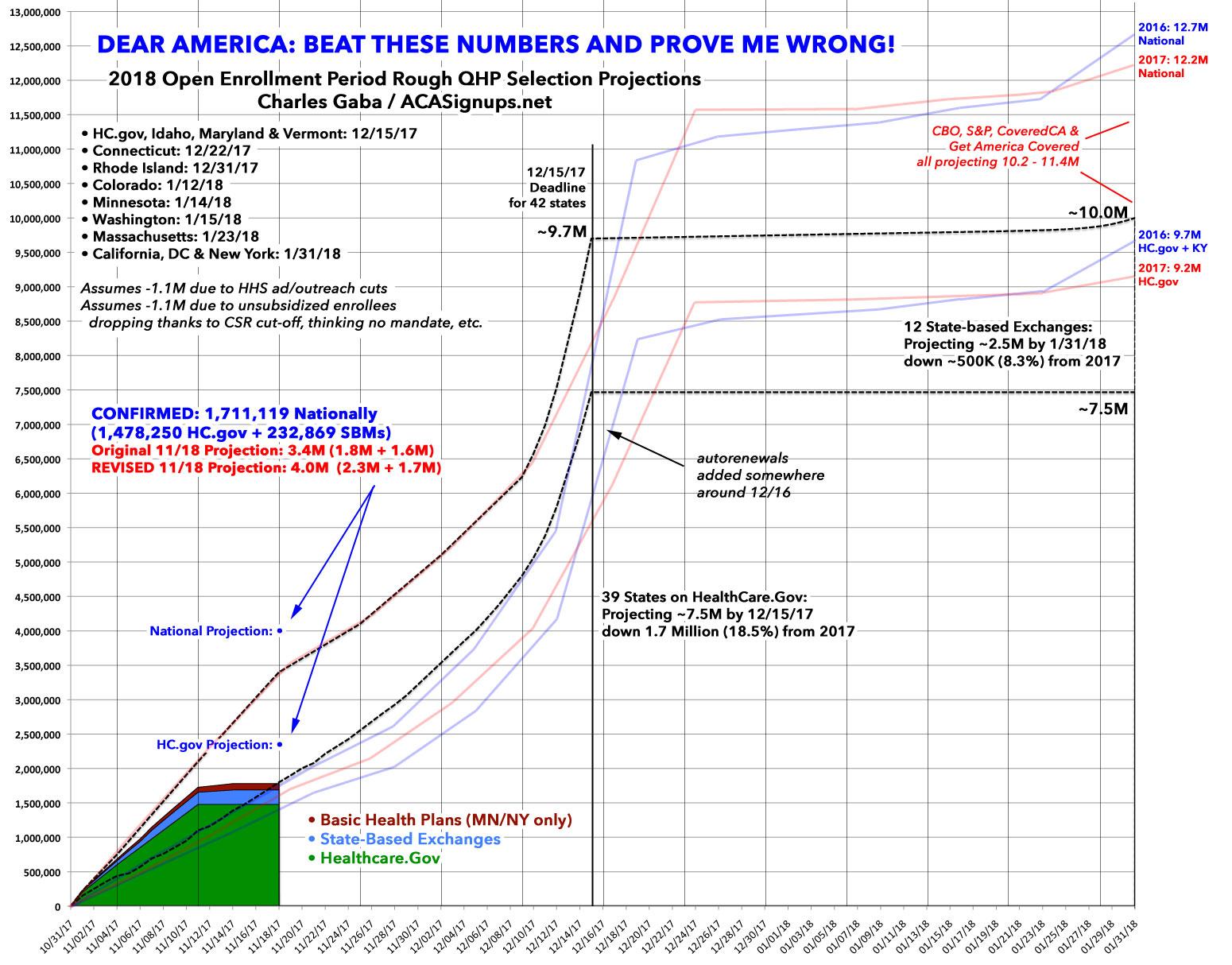

I know there’s a lot going on in The Graph (see below), so lemme break it down:

- The pale blue lines show the enrollment trend for the 2016 ACA Open Enrollment Period via the 38 HealthCare.Gov states (the lower line) and all 50 states + DC (the higher line). This was the all-time record for the ACA: 9.7 million via HC.gov, 12.7 million nationally.

- The pale red lines show the enrollment trend for the 2017 Open Enrollment Period via 39 HC.gov states & all 50 +DC (Kentucky moved from their own exchange to the federal exchange last year). This was down a bit from 2016: 9.2 million / 12.2 million.

- The dotted black lines are my “official” projections for the 2018 Open Enrollment Period: 7.5 million and 10.0 million respectively, both way down from both of the prior years.

- The filled-in green/blue sections are the actual, confirmed 2018 enrollment numbers to date. Note that there are still enrollments missing: HC.gov only runs through 11/11, while other states range from no data at all all the way through 11/15. I’ve confirmed 1.71M to date, but suspect the total is actually closer to 3.0 million as of today.

- The little blue dots are my current projections through this Saturday the 18th: 2.3M and 4.0M respectively.

(you can ignore the thin “Basic Health Plan” section for the moment)

As you can see, at the moment the numbers are running about 27% ahead of my projections, which is a very good thing for several reasons. For one thing, like early voting, it “locks in” enrollments ahead of the deadline (although they can still go back and cancel/switch plans if they wish). For another, it helps lessen the congestion during the final weekend surge.

OK, so we’re 27% ahead of where I figured so far...extrapolate that out to the end of Open Enrollment and we should have a tally of 10.0M x 1.27 = ...12.7 million, exactly as many as 2016, equalling the record! Fantastic, right?

Well, yes...and if we manage to pull that off, it’ll be an astonishing accomplishment given all the insanity, sabotage, undermining, confusion and chaos of the past 10+ months.

HOWEVER...as geeked as I am about these early numbers, I also need to issue a bit of caution. Just like early voting trends don’t necessarily mean anything in terms of the final election day vote outcome, early enrollment trends don’t guarantee the final tally either.

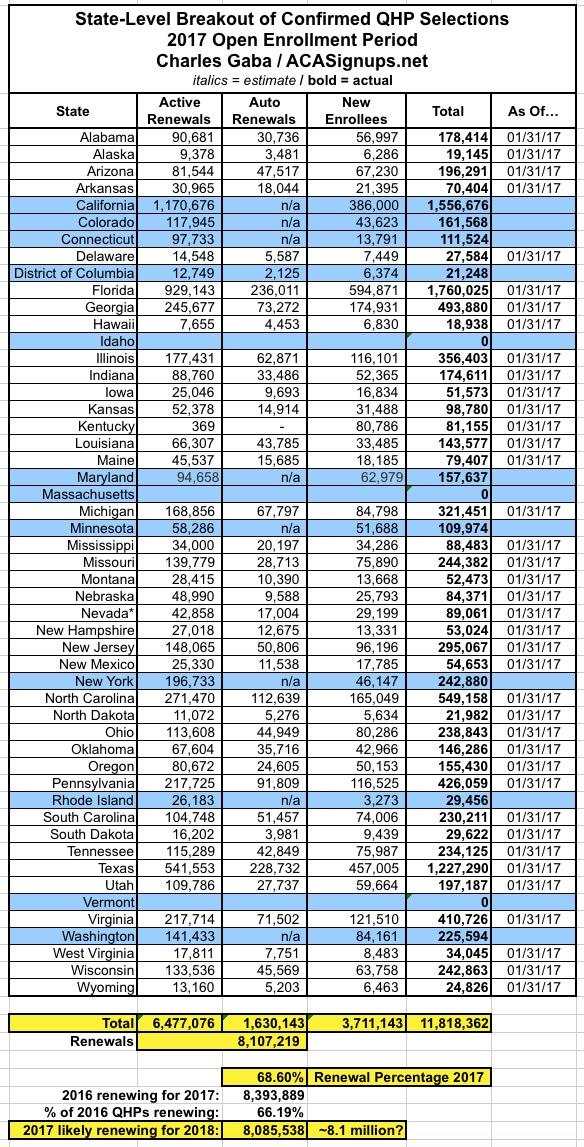

Here’s the state-level breakout of last year’s enrollments (it’s missing 3 states—Idaho, Massachusetts and Vermont, which collectively added up to around 397,000 people, or 3.3% of the total, but I’ve corrected for them at the bottom). As you can see, out of about 12.7 million enrollees from the end of the 2016 enrollment period, only about 68.6%, or 8.4 million actually re-enrolled for 2017. As of the end of 2016, there were roughly 9.1 million people still enrolled in active ACA exchange accounts, which means around 92% of enrollees renewed. The ratios for 2015 and 2016 periods were similar.

Since the 2017 total was about half a million lower (12.2 million), this means that even under the best of circumstances, I wouldn’t expect more than 8.1 million current enrollees (out of about 8.8 million total still enrolled in December) to re-enroll for 2018...and these are not the best of circumstances.

Of those 8.8 million still enrolled in December, about 15% should be unsubsidized, or 1.3 million. Given the 30% unsubsidized rate hike (thanks mostly to Trump/GOP sabotage), I expect most of the unsubsidized enrollees to drop out of the market—call it perhaps 1 million even, bringing the total renewal tally down to perhaps 7.8 million instead.

OK, that’s renewals. What about NEW enrollments?

We’d need about 2.2 million to hit my pessimistic 10.0 million total, 4.4 million to hit last year’s total or 4.9 million to break 2016’s record.

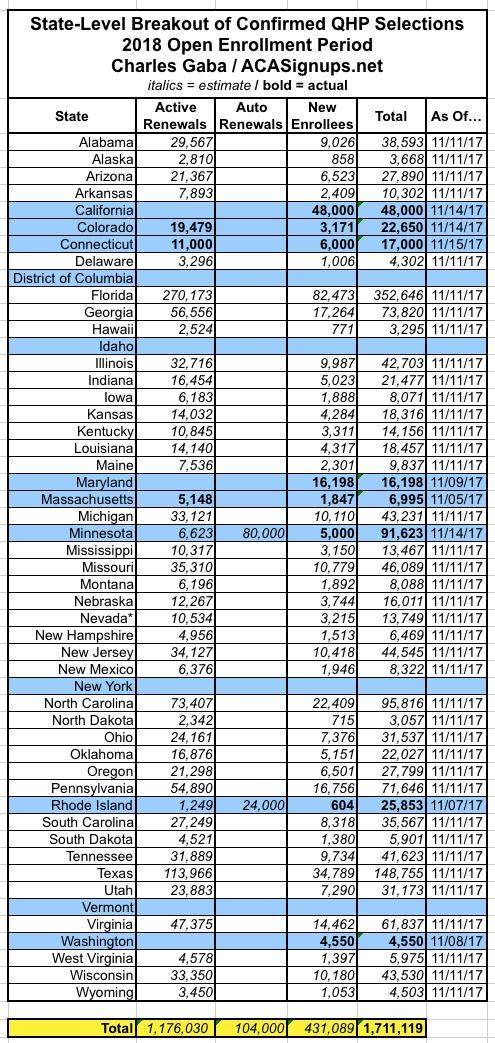

So, how are we doing so far? Well, here’s what I have as of 11/16:

Again, there’s probably a good 1.3 million total enrollees missing through 11/15, but so far I’ve confirmed 1.28 million renewals and 431,000 new enrollees. That means we need the following:

- To hit 10.0M: 6.52 million renewals + 1.77 million new

- To hit 12.2M: 6.52 million renewals + 3.97 million new

- To hit 12.7M: 6.52 million renewals + 4.47 million new

Now, here’s where things get interesting:

Thanks, ironically, to Donald Trump’s failed attempt at sabotaging the ACA by killing CSR subsidies, we find ourselves in the absurd Silver Load/Silver Switcharoo situation in most states, with subsidized enrollees receiving substantially higher premium tax credits than they otherwise would...which in turn means that many people can now buy Gold plans for less than Silver, or can get Bronze plans dirt cheap or even free in many cases.

Until now I’ve focused mainly on the price changes for existing enrollees, but according to the Kaiser Family Foundation, there’s a substantial number of currently uninsured people who not only qualify for ACA tax credits, but could get a fully ACA-compliant exchange policy for next to nothing...either less than the individual mandate penalty ($695 or 2.5% of income) or, for many nothing at all in premiums (they might still have a high deductible, but so what if the premiums are free anyway?)

How many people are we talking about? Well, get this:

We estimate that over half (54%) of the subsidy eligible-uninsured could purchase a bronze plan for 2018 for no premium contribution, after accounting for the premium subsidy. An additional 16% of this group could purchase a bronze plan for less than the cost of the tax penalty if they do not secure minimum essential coverage. Altogether 70% of subsidy eligible-uninsured (5.8 million people) are able to purchase a Bronze plan for nothing or less than the cost of the individual mandate penalty.

So how many people is that? Well, 5.8 million = 70% of 8.3 million, so 54% of that would be about 4.5 million people.

That’s right: 4.5 million uninsured Americans qualify for a FREE Bronze plan for 2018.

(Another 1.3 million qualify for a Bronze plan costing less than the individual mandate penalty, but that might just confuse the issue).

I don’t normally recommend Bronze plans for most people; Silver is usually a more logical value...but if you’re debating between a FREE Bronze plan (or one which costs less than the penalty) and not getting covered at all, it’s a no-brainer.

SHOP AROUND AND GET COVERED.

Advertisement