Georgia: Congrats, Mr. Hudgens, your self-described obstruction continues to pay off 4 yrs later

Wed, 09/27/2017 - 9:51pm

Earlier today, the Georgia Department of Insurance issued this press release:

INSURANCE DEPARTMENT RELEASES PROPOSED RATES FOR 2018 HEALTHCARE EXCHANGE

Atlanta – Insurance Commissioner Ralph Hudgens announced today that his office had submitted proposed 2018 health insurance rates to the Centers for Medicare and Medicaid Services (CMS) for the federally-facilitated Healthcare Exchange for final federal approval.

“Today my office submitted 2018 Obamacare rates to Washington D.C. for approval,” Hudgens said. “In its fifth year, Obamacare has become even more unaffordable for Georgia’s middle class with potential premium increases up to 57.5 percent. I am disappointed by reports that the latest Obamacare repeal has stalled once again and urge Congress to take action to end this failed health insurance experiment.”

A summary of the filed rate increase percentages from insurers who intend to offer individual coverage in Georgia for 2018 can be found on the Insurance Department’s website at www.oci.ga.gov/Other/ThisAnnouncement.aspx?ID=1091. CMS will post information on their final approved rates at https://ratereview.healthcare.gov.

Open enrollment for the Marketplace begins Nov. 1, 2017, and ends Dec. 15, 2017. Consumers are encouraged to contact a local insurance agent or visit Healthcare.Gov to learn more about plan options and pricing for 2018.

If that isn't a particularly professional-sounding press release from the state insurance commissioner, you shouldn't be surprised: This is the same GA Insurance Commissioner Ralph Hudgens who, on August 27, 2013, said the following:

“Let me tell you what we’re doing (about ObamaCare),” Georgia Insurance Commissioner Ralph Hudgens bragged to a crowd of fellow Republicans in Floyd County earlier this month: “Everything in our power to be an obstructionist.”

After pausing to let applause roll over him, a grinning Hudgens went on to give an example of that obstructionist behavior, this one involving so-called “navigators” who are being hired to guide customers through the process of buying health insurance on marketplaces, or exchanges, set up under the federal program.

“We have passed a law that says that a navigator, which is a position in that exchange, has to be licensed by our Department of Insurance,” Hudgens said. “The ObamaCare law says that we cannot require them to be an insurance agent, so we said fine, we’ll just require them to be a licensed navigator. So we’re going to make up the test, and basically you take the insurance agent test, you erase the name, you write ‘navigator test’ on it.”

Hudgens clearly thought that was a pretty cute way for state officials to obstruct and delay implementation of the program and to ensure that it doesn’t work well for Georgians. Judging from their reaction, his audience thought so too. The question is why he thinks such steps are necessary.

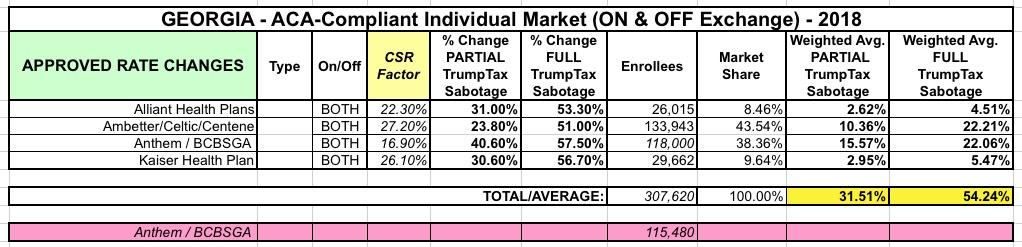

Well, mazel tov, Mr. Hudgens, because between your "grinning obstruction" that you bragged about and a laundry list of other types of sabotage and undermining of the ACA over the years, combined with more recent sabotage efforts by the Trump Administration and, yes, some legitimate issues within the law itself, you've managed to get exactly what you wanted. Here's the final, approved rate changes for the unsubsidized enrollees in the 2018 Georgia individual market:

Anthem is pulling out of about half the state, but is sticking around in the other half; I've confirmed that roughly half of their ~233,000 indy market enrollees will have to shop aroudn for another policy this fall.

Unlike some states which are vague about the impact of CSR reimbursement payments not being made (or at least not being guaranteed) next year, the GA DOI was happy to provide very specific numbers for each of the 4 carriers: Statewide, GA indy market rates are going up 31.5% if CSR payments are locked in (which they won't be)...or 54.2% if they aren't (they won't). That means a full 22.7 percentage points of next year's rate hikes, or about 42% of it, is being caused specifically by the CSR issue.

As it happens, I've also confirmed that at least one of the four carriers, Alliant, plans on utilizing the Silver Switcharoo Gambit, which means that the most of their 26,000 indy market enrollees should not only be protected from these huge hikes but may even come out significantly ahead...but I don't know how the other three are approaching the situation. If they don't do the Silver Switcharoo, unsubsidized enrollees are in deep trouble, and it won't be great for unsubsidized folks even if all 4 carriers do so.

Meanwhile, Ralph Hudgens must've been grinning his way home from work today.

Advertisement