American Academy of Actuaries patiently explains Insurance 101 to GOP (w/pictures!)

Fri, 07/14/2017 - 3:58pm

Yes, that's GOP Speaker of the House of Representatives, 2nd in line to the Presidency, utterly clueless about the basic concept of how health insurance (or any type of insurance, really) works.

The American Academy of Actuaries has chimed in on the GOP Senate's #BCRAP Obamacare replacement bill, and I have to imagine that they had to bite their tongues clean through while composing this primer explaining the most rudimentary concepts behind "insurance", "risk pools" and "adverse selection" to Paul Ryan, Ted Cruz, Mike Lee and Mitch McConnell:

Risk Pooling: How Health Insurance in the Individual Market Works

What is risk pooling?

The pooling of risk is fundamental to the concept of insurance. A health insurance risk pool is a group of individuals whose medical costs are combined to calculate premiums. Pooling risks together allows the higher costs of the less healthy to be offset by the relatively lower costs of the healthy, either in a plan overall or within a premium rating category. In general, the larger the risk pool, the more predictable and stable the premiums can be.

Is the size of a risk pool the only factor?

No. Although larger risk pools are typically more stable, a large risk pool does not necessarily mean lower premiums. The key factor is the average health care costs of the enrollees included in the pool. Just as a pool with healthy individuals can result in lower-than-average premiums, a large pool with a large share of unhealthy individuals can have higher-than-average premiums.

What is “adverse selection”?

“Adverse selection” describes a situation in which an insurer (or an insurance market as a whole) attracts a disproportionate share of unhealthy individuals. It occurs because individuals with greater health care needs, when given the opportunity, are more likely to purchase health insurance and to purchase health insurance with richer benefits than individuals with fewer health care needs.

Why is adverse selection a problem?

Adverse selection increases premiums for everyone in a health insurance plan or market because it results in a pool of enrollees with higher-than-average health care costs. Adverse selection is a byproduct of a voluntary health insurance market in which people can choose whether and when to purchase insurance coverage, depending in part on how their anticipated health care needs compare with the insurance premium charged.

Before anyone accuses me of being condescending: I fully admit that I didn't fully understand some of these concepts 4 years ago myself. HOWEVER, these are U.S. Senators. And while I don't expect them to be experts in every field of study, that's why they a) have a staff to assist them in learning such things and b) why they're SUPPOSED to hold hearings, listen to testimony and LEARN about such matters from PEOPLE WHO DO UNDERSTAND IT.

Instead, they've held zero hearings with actuaries, hospital officials, patient advocacy groups, insurance brokers, doctor/nursing groups, patients or any other people who actually understand the impact of what the bill they're supposed to be voting on next week.

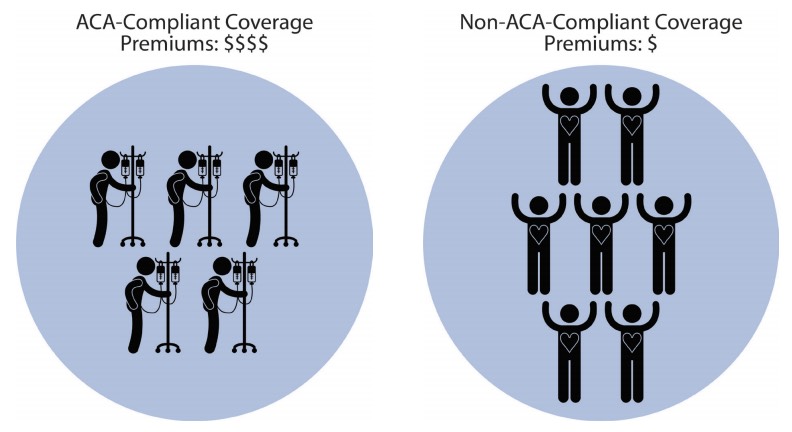

Not only did the AAA find it necessary to spell basic insurance concepts out in small words for Sen. Cruz & Co., they even resorted to using stick figures as well. I guess those are mostly for Donald Trump's benefit.

Advertisement