GUEST POST: The Budget Game Has Changed by Jim Stuart

Thu, 08/28/2014 - 1:29pm

Hat Tip To:

Jim Stuart

I post guest entries once in a blue moon, and this one could be huge, if his conclusions are accurate (and still well worth discussion even if they aren't). Recently, both Sarah Kliff over at Vox and Margot Sanger-Katz & Kevin Quealy at the NY Times Upshot have delved into some fascinating and unexpected news regarding Medicare & Medicaid spending in the U.S. over the past few years.

Well, an ACASignups supporter named Jim Stuart (all I really know about him is that he's a retired executive and educator who attended Princeton and lives in Illinois) has gone even deeper into the weeds on this and, well, I'll let those who know more about such things than I do decide how much of a Big Deal this is.

With Jim's request/permission, I'm reposting his piece verbatim, but I'd also advise checking out his own blog.

Full disclosure: Jim has financially contributed to me, but my decision to repost his work has nothing to do with that.

The Budget Game Has Changed

by Jim Stuart

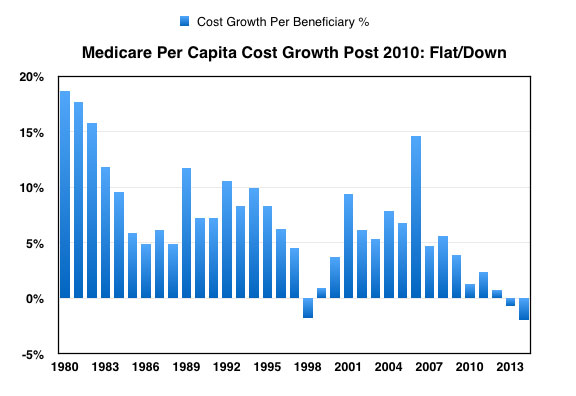

Evidence is mounting that per beneficiary Medicare costs are flattening or dropping. The chart above shows the trend in per beneficiary cost growth since 1980. Before now, the only "off trend" period was 1998-1999. Turns out this short drop in cost growth was caused by the 1997 Balanced Budget Act, which significantly adjusted and cut payment rates. Providers complained loudly, and the Balanced Budget Refinement Act of 1999 reduced many of these cuts and put Medicare back on its strong annual growth in spending per beneficiary.

Beginning roughly in 2010, another slowdown began, this time with no immediate adjustment in Medicare payment rates: the ACA was passed in March, 2010, but the first payment rate adjustment didn't occur until 2012, when the annual market basket inflation adjustment was reduced from 3% to 2%.

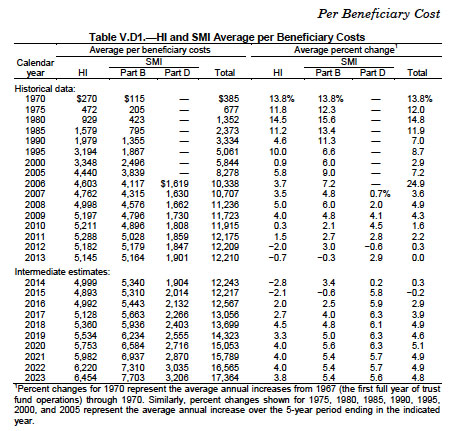

Sarah Kliff of Vox was digging through the most recent CMS Trustees' Report, and she was stunned to come across this "deep data chart" on page 283:

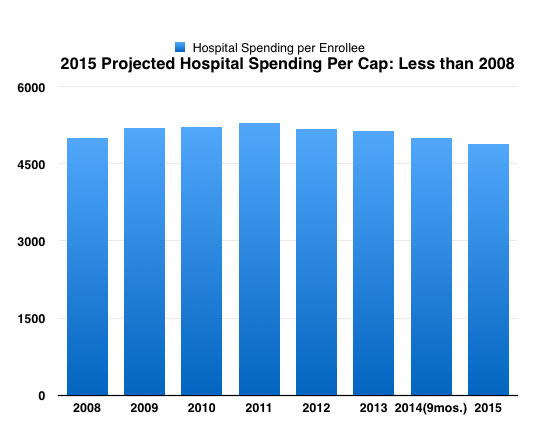

From this she put together the following chart, showing how per beneficiary spending has flatlined in the Hospital Insurance portion of Medicare:

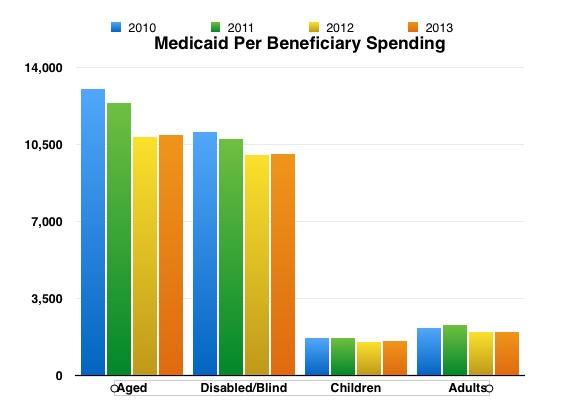

The charts above deal with Medicare per beneficiary cost growth. Information is less plentiful for Medicaid per capita spending, due to high turnover in the membership base, but here is a chart put together from a number of CBO Medicaid Focus Briefs put out before the annual 10 year Budget Outlook, generally published in March each year. Here we see per beneficiary Medicaid costs declining:

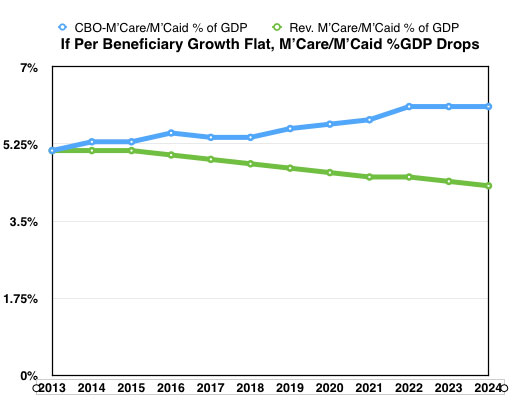

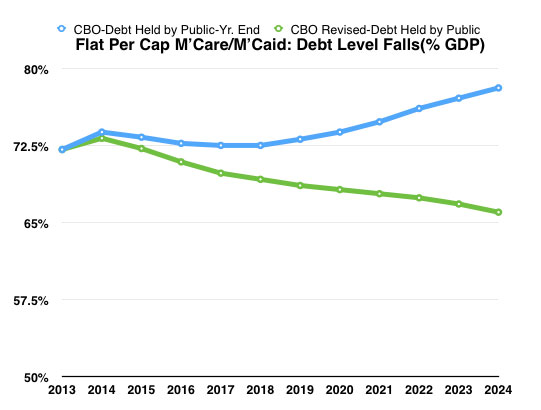

What would happen if this trend continued? What would our budget picture look like if Medicare and Medicaid per beneficiary costs stayed constant? In particular, what would happen to the critical Debt to GDP ration? I downloaded the CBO 2014-2024 Budget Outlook model, then adjusted it to hold per beneficiary cost growth for Medicare and Medicaid at zero. Here are the results for the ratio of combined Medicare/Medicaid spending to GDP and the Debt/GDP levels for two scenarios - current CBO forecast and that forecast revised to hold per beneficiary spending constant:

Because Medicare and Medicaid take a decreasing share of our resources, deficits gradually decline, moving below the rate of GDP growth (and staying there), thus allowing the Debt/GDP ratio to decline.

With zero per capita spending growth - in other words, with Medicare and Medicaid spending growing only with enrollment - Debt to GDP ratios drop gradually over the 10 year period. Budget deficits stay below GDP growth, allowing the debt ratio to improve.

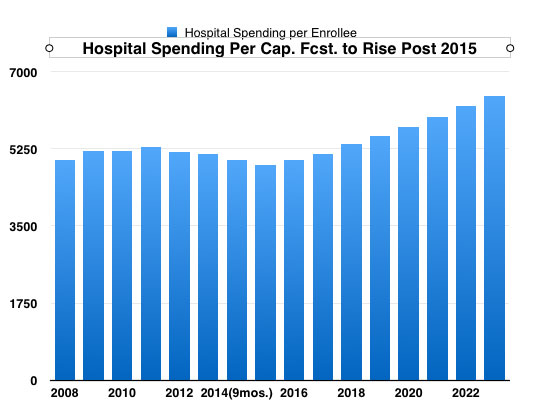

But this is a far cry from what CMS and the CBO are forecasting. Here's CMS' forecast for per capita Hospital Spending:

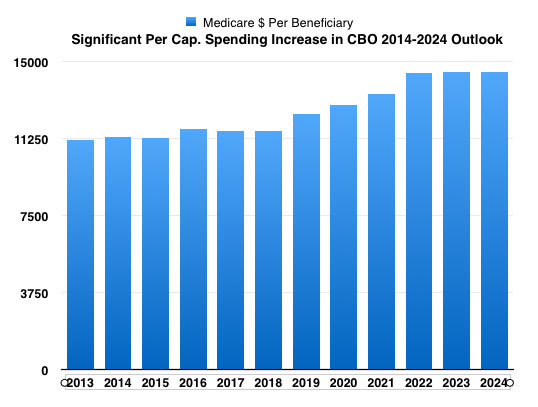

And here's the CBO:

How do they support this resumption in per beneficiary cost growth in 2016, after a five year hiatus? Nothing much is said: CMS is silent; CBO presents some discussion of competing research viewpoints on overall economy-wide healthcare cost trends; mentions one of its own papers (here) saying the Medicare cost slowdown is most likely not recession related; then presumptively uses a 3% per beneficiary annual cost growth average, plus the anticipated 3% annual growth in enrollment as the baby boom is absorbed into Medicare. The result is the same it seems to have always been: we're OK for now, but we're in trouble in the long term, as we watch Medicare/Medicaid take an ever-increasing share of our national resources, leaving the country with an untenable long term structural budget problem.

The "healthcare cost slowdown is recession-related and therefore temporary" school got a big boost last week with the Health Affairs publication of a peer-reviewed research report showing how markets that were the hardest hit by the recession (Las Vegas, Birmingham, AL), measured in local/regional employment trends, showed the biggest healthcare cost slowdown, versus markets (Trenton, Dallas) that were relatively unscathed by the Great Recession. In fact,the hard hit Las Vegas and Birmingham markets showed private insurance-based healthcare costs growing from 5.4-7.2% per annum, where similar costs in the less affected Trenton and Dallas markets grew from 28 to 29%. The research concluded that: the recession/economy/income accounts for 70% of the healthcare cost slowdown; systemic changes in healthcare delivery are not that important, and we can expect cost growth to resume (with a lag effect) as the economy picks up steam.

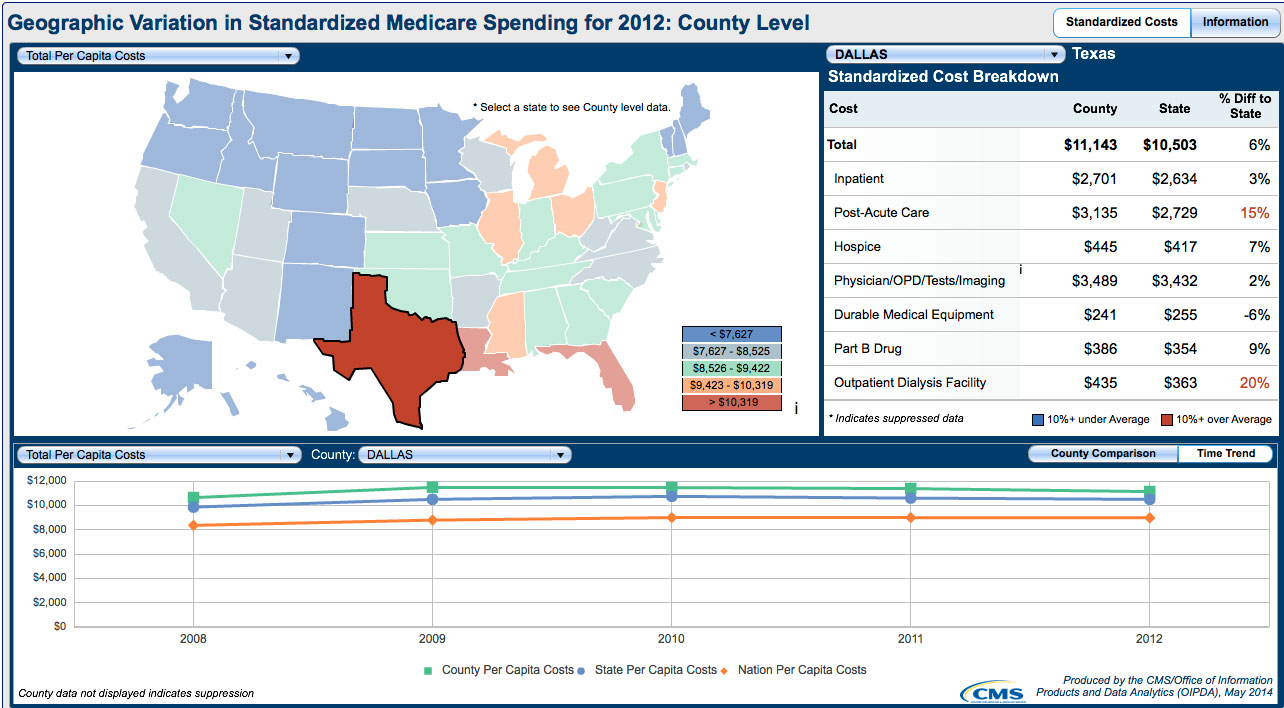

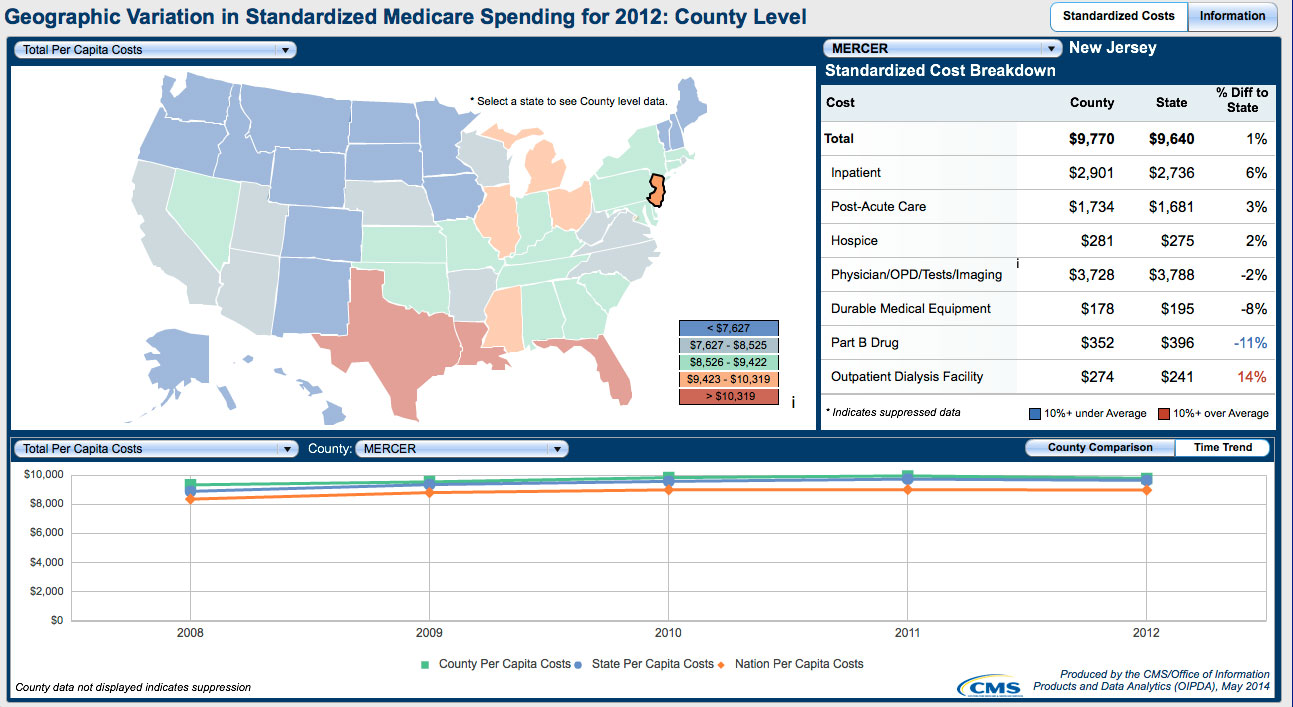

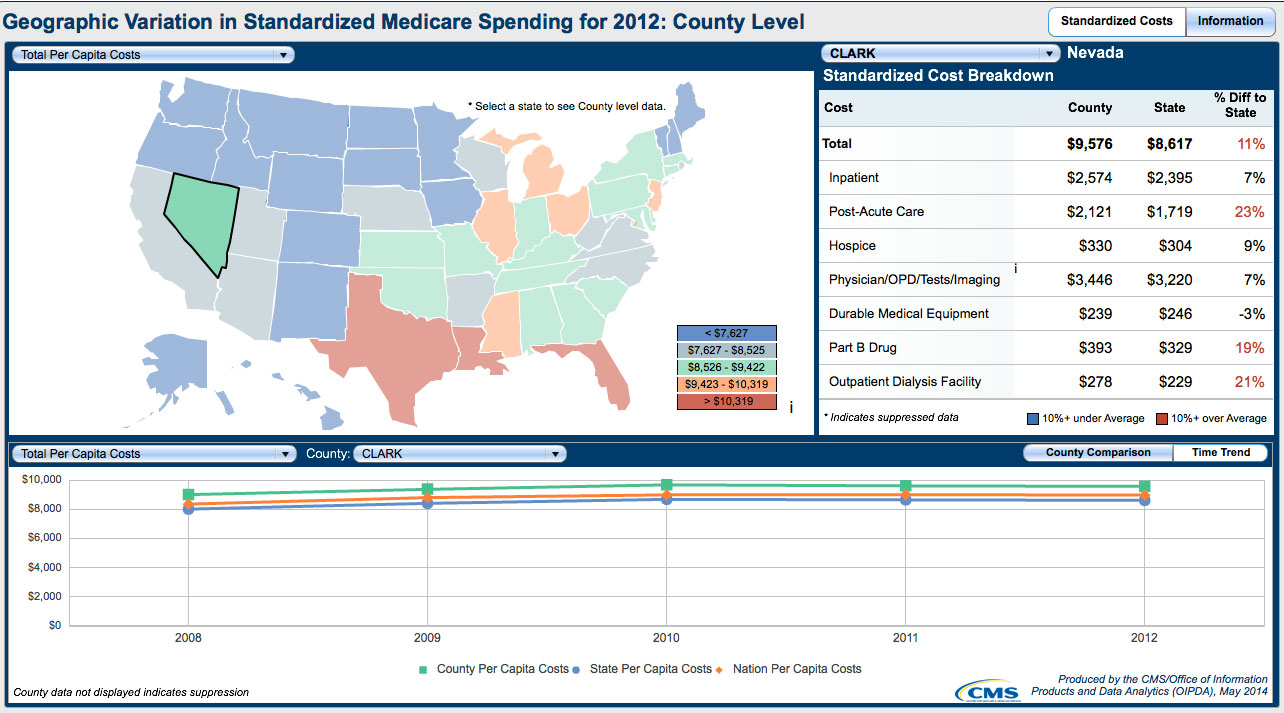

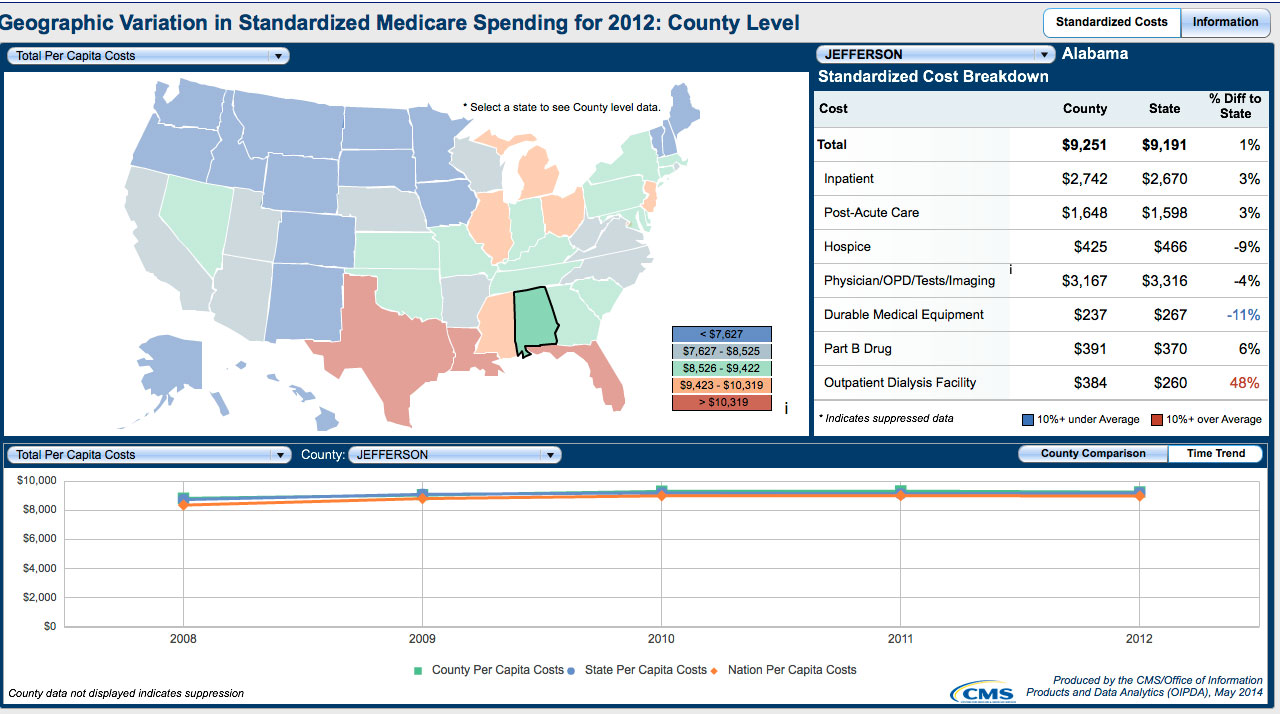

I'm not equipped to argue the case with regards to the private market, but I will claim that the research results simply don't apply to the public, Medicare/Medicaid markets. Enrollees in these programs have minimal out of pocket costs. In fact, for Medicare those already low costs have been coming down: premiums held flat and closing the Part D Prescription Drug Care donut hole. Recession and the resultant changing income levels should have no effect on utilization in either program. Turns out the CBO publishes amazing county-level Medicare per beneficiary spending trends(here). I decided to check the same four counties the Health Affairs researchers had reviewed. Here are per beneficiary Medicare spending results for the two "hard hit" counties (Las Vegas and Birmingham) and the two that came out of the Recession "relatively unscathed" (Trenton and Dallas). As you can see: no difference - the per beneficiary spending slowdown showed almost identical trends in all four counties:

So what IS going on? If the Recession is not the slowdown's cause, and enrollee out-of-pockets are actually coming down (as opposed to going up markedly in the private insurance marketplace), why are per person costs flattening? The fair answer is that I don't really know; but there are things the evidence points to.

First, it's essential to understand what we're looking at (and here, I will focus on Medicare): when reviewing Medicare "spending trends", you are not really looking at spending; rather you are seeing provider billing information. Providers treat patients, then bill Medicare per a preset pricing list according to diagnostic related groups, or DRG's. Medicare spending is a country-wide buildup, provider by provider, of DRG's billed for services provided. The actual costs of providing those particular mix of services are nowhere reflected in Medicare billing. Spending over the allowed DRG limit is simply shifted to other patient categories (private insurance, private pay, charity). Almost all providers bill above the allowed per-DRG Medicare rate; but costs for the more efficient providers can line up with these DRG rates.

So Medicare spending trends over time are an unusually clean and precise look at trends in patient utilization (both usage and mix of services, or complexity of usage). In this light, since we are in a billing, not a spending model, inflation doesn't happen all the time, at different rates throughout the year; it happens once a year, with a different "market basket rate adjustment" depending on service category. For example, the Part A/Hospital Insurance market basket up date for 2012 was 2%, after taking off (for the first time, per ACA) 1% for the multi- factor, economy-wide, 10 year average productivity adjustment.

Billing, not spending. And therefore an unusually good approximation of system utilization for our prototypical average, or composite patient. What's happening here? Some will argue that with the arrival of the Baby Boomers beginning in 2010, the Medicare pool is getting younger, therefore healthier. This is most likely true, though the impact of moving annual enrollment growth from 2-3% to 3-4% is likely quite modest, though certainly helpful. Speaking quite broadly, I think evidence will start to show that the healthcare provider system is getting more efficient - less utilization/complexity to support our "average/composite" patient. We can begin to see this clearly in Medicare (and probably Medicaid); it will take more time in the private insurance sector.

There are two huge and converging trends in healthcare that I believe are causing the entire system to become self-organizing around the desire to reach these difficult, yet attainable objectives: Electronic Health Records (EHR) and the movement away from fee-for-service. There are other initiatives (penalties for hospital readmissions, for example), but these two hold the key. Providers want to achieve both; they are, I believe, convinced that they must achieve both, and quickly, in order to be successful in the evolving healthcare order of things.

Each initiative requires big provider investments and transformational changes in culture. Many providers will fail. Many more will be gobbled up as providers seek scale and more forward, cross-functional integration.The examples of giant organizations like The Mayo Clinic are powerful: where all services are under one ownership/organizational roof,and there is no, or little quantity incentive. Mayo is the quintessential accountable care organization, where patient costs are low, in large part because patient care is brilliantly coordinated, EHR is (and has been) largely in place, and quality care is the obsessive focus, not quantity of procedures performed (often the fee-for-service incentive results).

No one can predict exactly what this will all look like in 5 to 10 years. But what we can say with confidence is that these two powerful trends are happening: the movement to EHR and the shift away from fee-for-service. Just last week, Health Affairs reported on the extraordinary progress the system is making towards EHR: 59% of hospitals now have basic EHR in place, up from 15% in 2010. There are, and will be problems on the way to full adoption, but this train is moving fast.

So moving back into the Medicare/Medicaid cost forecasting arena, do you agree withCMS and the CBO that per beneficiary costs will restart their historical 3-5% growth trend? I don't. If I'm right, how long will it take the system to catch up and adjust their forecasts? I can't say, but my guess is: 2-3 years at a minimum. Democrats will, quite rightly, push this in the 2016 election, if per capita costs stay flat for Medicare and Medicaid. Conservatives will trumpet the news loudly when overall healthcare spending moves up, due to the large ACA coverage expansion . Progressives will need to work hard to keep the focus on per capita costs, not total spending.

As a progressive, feel we are moving into very rich terrain: the healthcare system has been transformed, and now is taking on the job of transforming itself, which all systems will do, when they select a new identity, as long as the system remains open, sufficient information is provided to all relevant players, and relationships between players are well coordinated. Probably the most important policy change needed to speed this change is to find more ways to reward providers for not performing services, in other words by not spending/billing for added procedures because you (the provider) have found a better way to treat the patient and thereby eliminate procedures done in the past.

A system that rewards for services performed (FFS) needs, dare I say, a way to "reward abstinence," if that abstinence is congruent with the best healthcare practices and supports/nurtures the patient. Peter Orzag, formerly CBO Director, now at Citibank, and on the Board of Mt. Sinai Hospital in New York, is a clear voice calling for CMS to find ways to pay for quality, including rewarding providers for not doing procedures in certain circumstances. He tells us that Mt. Sinai is "bleeding money" by finding more and more ways to keep patients out of the OR and out of their hospital, believing that fee for service is on its way out, and the system will start paying for quality, and for doing a better job of keeping patients healthy.

The politics of this is something else. The Right will resist this for as long as possible, because it means they can't scream for budget cuts or the dismantling of entitlements. The CMS and CBO will be typically slow to change their fundamental assumptions about the healthcare future.

But it's happening. We need to get ourselves together to magnify the power of this crucial transformation of our collective healthcare and therefore overall budget future.

Advertisement