The Connecticut Insurance Department has posted the initial proposed health insurance rate filings for the 2021 individual and small group markets. There are 14 filings made by 10 health insurers for plans that currently cover about 214,600 people.

Important: As noted below, the 214,600 figure is Connecticut's individual & small group market combined.

Two carriers – Anthem and ConnectiCare Benefits Inc. (CBI) – have filed rates for both individual and small group plans that will be marketed through Access Health CT, the state-sponsored health insurance exchange.

The 2021 rate proposals for the individual and small group market are on average slightly lower than last year:

Unfortunately, it looks like only some of the 2021 ACA individual market premium rate filings have been uploaded to the SERFF database as of today, so I'm unable to calculate anything even close to an accurate weighted average. There are, however, several noteworthy items on the TX market:

It's been a solid year since Joe Biden rolled out his own official healthcare policy proposal. I did a fairly in-depth writeup on it last summer, but it's the understatement of the year to say that "a lot has changed since then".

The two most obvious developments on this front are 1. Biden has gone from one candidate of two dozen to being the presumptive Democratic Nominee; and 2. The COVID-19 pandemic has completely upended not only the Presidential race but the economy and the entire U.S. healthcare system. A third important (if less consequential) development is that the House has actually passed their own "ACA 2.0" bill in the form of H.R. 1425, the Affordable Care Enhancement Act, which partially overlaps Biden's healthcare plan.

Tennessee has also posted their preliminary 2021 rate filings for both the individual and small group markets. Aside from being one of the few states where a significant number of carriers are including any COVID-19 pandemic factor at all (in both markets), Tennessee has several new entrants and one significant withdrawl (I think).

On the individual market, UnitedHealthcare is newly entering, while Cigna is expanding their coverage areas as noted here. Cigna is also newly entering Tennessee's small group market, as is Bright Health Insurance.

Overall, Tennessee carriers are asking for a 10.3% increase on the indy market (the second highest so far after New York's 11.7% average), mostly driven by Blue Cross Blue Shield, which holds a whopping 83% of the market. On the small group market, the average increase is 5.5%.

COVID-19 accounts for 1.7 points of the increase on average in the indy market and 2.6 points in the small group market. This, again, is the highest statewide average COVID impact I've seen after New York state so far.

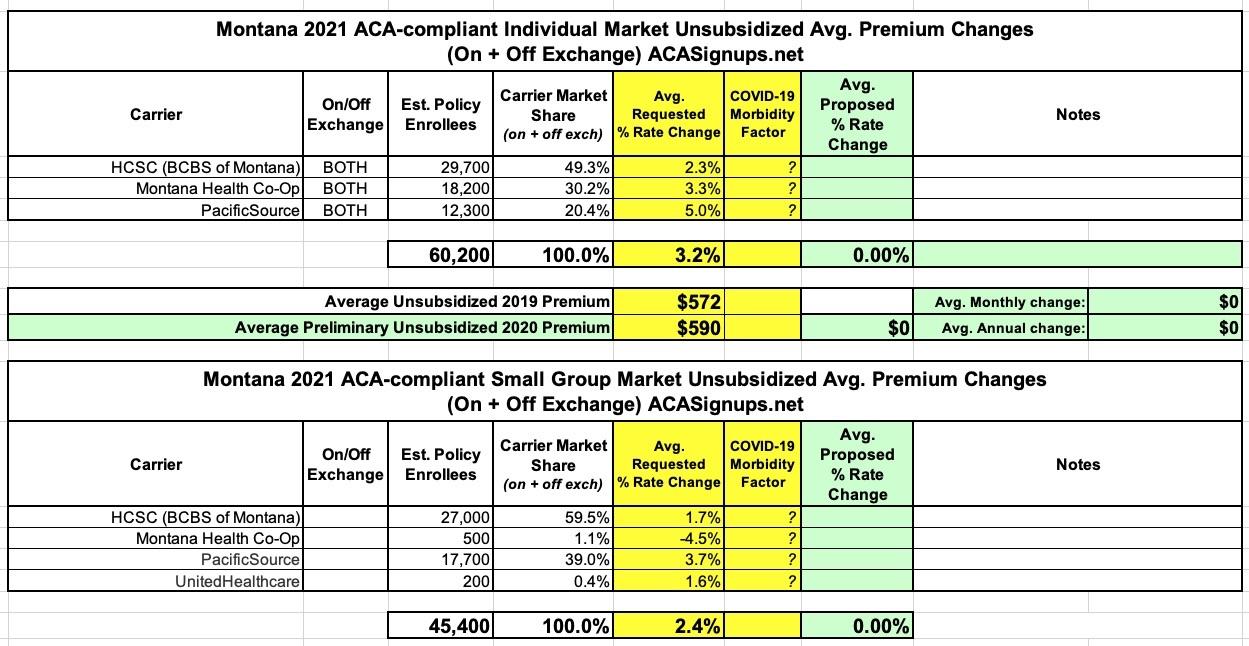

Last year, thanks to the Section 1332 Reinsurance waiver allowed for by the ACA, Montana health insurance carriers reduced their premiums for 2020 by 13.1% on average on the individual market, while raising them by 7% on the small group market (which the reinsurance program doesn't impact).

Between the COVID-19 pandemic and just getting generally swamped, I haven't gotten around to writing about Pennsylvania's state-based ACA exchange, due to launch this fall, since way back in December:

PA’s A Step Closer To Starting A State-Based Health Insurance Exchange

Pennsylvania’s new, state-run health insurance exchange is getting rolling ahead of its launch in 2021.

The commonwealth has chosen a California-based company, GetInsured to run it.

...Zachary Sherman, who heads the newly-created Pennsylvania Health Insurance Exchange Authority, said the contract with GetInsured will cost around $25 million annually, plus startup expenses that’ll be spread over several years.

“That’s compared to what we currently pay for Healthcare.gov, which is in the $90 to $95 million range,” he said.

Sherman said the administration chose GetInsured because it has already contracted with other states, like Nevada and Minnesota.

He said the new exchange is expected to save people between five and ten percent every year on premiums.

When I first read the quote, I assumed it was either a paraphrase, out of context or sarcasm. Sadly, it was none of those:

A series of controversial remarks by Missouri Gov. Mike Parson on a St. Louis radio show are getting widespread attention — and some pushback.

In an interview on Friday with talk-radio host Marc Cox on KFTK (97.1 FM), Parson indicated both certainty and acceptance that the coronavirus will spread among children when they return to school this fall. The virus has killed 1,130 people in the state despite a weekslong stay-at-home order in the spring that helped slow the virus’ spread — and the state set a record on Saturday with 958 new cases.

...Parson’s comment on the coronavirus signaled that the decision to send all children back to school would be justified even in a scenario in which all of them became infected with the coronavirus.

Yesterday Donald Trump was interviewed by Chris Wallace on FOX News Sunday. It was full of the usual batcrap insane lies and babbling on Trump's part, but one exchange in particular caught my attention:

Wallace: "I want to talk to you about Obamacare. Since the pandemic hit, millions of people have lost their jobs, and thereby lost their health insurance. Almost a half million have signed up for Obamacare. Your administration just announced that you're signing onto a lawsuit to overturn Obamacare..."

Trump: "And replace it."

Wallace: "Why does it make sense to overturn Obamacare, which people are now relying on...Democrats are gonna say, the man who's wanted to kill Obamacare is gonna take it away...the protections for pre-existing conditions..."

Trump: "First of all, we got rid of the individual mandate, pre-existing conditions will always be taken care of by me and Republicans, 100%.."

Wallace: "But you've been in office 3 1/2 years, you don't have a plan..."

The data below comes from the GitHub data repositories of Johns Hopkins University, execpt for Rhode Island, Utah and Wyoming, which come from the GitHub data of the New York Times due to the JHU data being incomplete for these three states. Some data comes directly from state health department websites.

Here's the top 100 counties ranked by per capita COVID-19 cases as of Saturday, July 18th (click image for high-res version):

NEARLY 58,000 MARYLANDERS GAIN HEALTH COVERAGE DURING TWO SPECIAL ENROLLMENT PERIODS

BALTIMORE, MD – A total of nearly 58,000 Marylanders enrolled in health coverage during Maryland Health Connection’s two special enrollment periods that began in February and March and ended Wednesday, July 15.

The Maryland Health Insurance Easy Enrollment program launched Feb. 26 as the first of its kind in the nation. The Comptroller of Maryland asked state tax filers to check a box on their state tax return if they lacked health insurance and desired that information to be shared with the Maryland Health Benefit Exchange. Several states are in the process of looking at creating similar programs.

Since February:

More than 41,000 filers checked the box

More than 3,700 enrolled as of July 13

Final numbers are pending, because tax filers had until the July 15 tax filing deadline to check the box on their state tax form, and will have several weeks to enroll.