Once again: The true measure of ACA healthcare coverage enrollment isn't how many people select policies during the Open Enrollment Period, it's how many actually have those policies in effect (aka "effectuated enrollment") as well as how comprehensive the policy is (ie, its "Actuarial Value").

New Mexico is a massive positive outlier on both fronts in 2026, and it's pretty obvious how they're pulling it off: Not only is it the only state which is fully backfilling 100% of the enhanced federal tax credits which Congressional Republicans allowed to expire back in December for 100% of all enrollees, they doing this in addition to their existing state-based supplemental subsidy program.

Last night, the 2026 ACA Open Enrollment Period (OEP) concluded across most states, including New Mexico (there are 10 other states with later deadlines).

BeWell NM, New Mexico's ACA exchange, is among the only ACA exchanges with ongoing daily enrollment data reports, last updated early this morning. Here's how they wrapped things up compared to the 2025 OEP (barring any clerical corrections in this year's data):

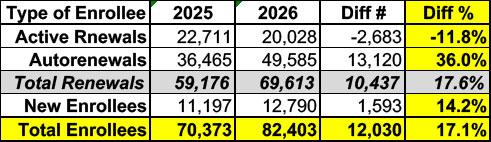

Overall enrollment in the Land of Enchantment is up a whopping 17%!

In other words, new enrollments are up 27% while active renewals are down about 10%; they pretty much cancel each other out compared to the same point last year.

While it appears that Congress will allow enhanced federal Premium Tax Credits to expire, New Mexico’s Health Care Affordability Fund (HCAF) will cover the loss of the enhanced premium tax credits for households with income under 400% of the Federal Poverty Level (or $128,600 for a family of four), providing up to $68 million in premium relief for working families who enroll in coverage through BeWell in 2026. Federal and state premium assistance will continue to reduce the impact of the rate increases.

New Mexico Open Enrollment 2026 - Enrollment Summary

Last Refreshed On: December 2, 2025

Officially, they're reporting 75,926 Qualified Health Plan (QHP) enrollments already, which is actually 8% higher than the 70,373 which they ended with during the 2025 Open Enrollment Period (OEP) last January.

HOWEVER...and this is a major caveat...that 75,926 includes all current enrollees being auto-renewed for 2026, which doesn't really count for my purposes. Most state exchanges used to hold off on lumping in the auto-renewals until after the initial December deadline, only reporting current enrollees who actively re-enroll along with new enrollees.

New Mexico Open Enrollment 2026 - Enrollment Summary

Last Refreshed On: November 12th 2025

Officially, they're reporting 70,485 Qualified Health Plan (QHP) enrollments already, which is actually slightly higher than the 70,373 which they ended with during the 2025 Open Enrollment Period (OEP) last January.

HOWEVER...and this is a major caveat...that 70,485 includes all current enrollees being auto-renewed for 2026, which doesn't really count for my purposes. Most state exchanges used to hold off on lumping in the auto-renewals until after the initial December deadline, only reporting current enrollees who actively re-enroll along with new enrollees.

IMPORTANT:Premium Alignment is NOT a substitute for making the enhanced ACA tax credits permanent. It does little to help the lowest-income folks who are still better off with Silver plans thanks to robust CSR assistance, and the benefits of it will be mediocre for those over 400% FPL if the enhanced tax credits expire.

Even for those it benefits the most (primarily those who earn between 200 - 400% FPL), it's a complement to the upgraded subsidies, not a replacement for them.

HOWEVER, it's still hugely helpful to those who know how to take advantage of it, and particularly in the states newly implementing it, it should relieve a huge portion of the pain being caused by the enhanced APTC expiring next month.

I've written multiple times in the past about "Silver Loading," the ACA health insurance policy pricing strategy in which insurance carriers load the extra cost of their Cost Sharing Reduction financial burden (the portion of deductibles, co-pays & coinsurance which they're required to cover themselves for low-income enrollees who select Silver plans) onto the gross premium of those same Silver plans.

It gets a bit wonky, but the bottom line is that Silver Loading results in the gross price of Silver ACA plans increasing significantly even if the price of Bronze, Gold & Platinum plans only go up modestly. This may sound bad, but stay with me.

From the carriers perspective, how the CSR load is allocated doesn't matter much as long as they aren't left stuck with the bill...but pricing the plans in this fashion has major implications for the enrollees themselves.

Last week I noted that six states have launched window shopping for the 2026 ACA Open Enrollment Period (OEP), allowing residents of the following states to plug their household information into their states ACA exchange website to see just how much their net health insurance premiums are going to increase starting January 1st, 2026:

As anyone not under a rock for the past few months knows by now, the improved federal Affordable Care Act tax credits which were put into place by President Biden and Congressional Democrats starting in 2021 are currently scheduled to expire at the end of December, just 2 1/2 months from now.

On top of this, the Trump Regime has also made administrative regulatory changes to how the ACA is structured resulting in the remaining tax credit formula becoming even less generous yet, while also eliminating eligibility for either financial assistance or even ACA enrollment whatsoever to many other Americans.