NEARLY 40,000 MARYLANDERS HAVE ENROLLED DURING CORONAVIRUS EMERGENCY SPECIAL ENROLLMENT PERIOD

Less than a week left for uninsured residents to get marketplace coverage

BALTIMORE, MD – The Maryland Health Benefit Exchange today is urging uninsured Marylanders to enroll in coverage before the June 15 deadline through the state’s health insurance marketplace, Maryland Health Connection, under the Coronavirus Emergency Special Enrollment Period. To date, nearly 40,000 residents have received health coverage during this special enrollment period that began in March with Gov. Larry Hogan’s announcement of a State of Emergency in Maryland.

Over a year ago, I wrote an analysis of H.R.1868, the House Democrats bill that comprises the core of the larger H.R.1884 "ACA 2.0" bill. H.R.1884 includes a suite of about a dozen provisions to protect, repair and strengthen the ACA, but the House Dems also broke the larger piece of legislation down into a dozen smaller bills as well.

Some of these "mini-ACA 2.0" bills only make minor improvements to the law, or make improvements in ways which are important but would take a few years to see obvious results. Others, however, make huge improvements and would be immediately obvious, and of those, the single most dramatic and important one is H.R.1868.

The official title is the "Health Care Affordability Act of 2019", but I just call both it and H.R.1884 (the "Protecting Pre-Existing Conditions and Making Health Care More Affordable Act of 2019") by the much simpler and more accurate moniker "ACA 2.0".

Health Carriers Propose Affordable Care Act (ACA) Premium Rates for 2021

BALTIMORE – Health carriers are seeking a range of changes to the premium rates they will charge consumers for plans sold in Maryland’s Individual Non-Medigap (INM) and Small Group (SG) markets in 2021.

The rates submitted for the INM market include the estimated impacts from the state-based reinsurance program (SBRP) enacted in 2019 via a 1332 State Innovation Waiver, approved by the federal Centers for Medicare & Medicaid Services.

“As CEO of the Washington Health Benefit Exchange, I have been saddened and horrified by the brutal death of George Floyd while in police custody. His death represents one of the most recent in a long history of violence against black people, including Philando Castile, Breonna Taylor, and Ahmaud Arbery, and far too many others. As communities across the state and the nation voice their justified anger and frustration, we stand with the Black community and all communities of color. This tragic event reminds our leadership and staff of the urgent need to continue to address structural racism as a way to narrow health disparities, especially in communities of color.

“We, too, are deeply concerned about the property damage taking place in our cities. It is harmful to so many people, including the communities who are working to make their voice heard. We choose to focus on the protestors’ message of racial justice over the damage being committed by a disorganized few, because property is replaceable and Black lives are not.

Now that I've brought all 50 states (+DC & the U.S. territories) up to date, I'm going to be posting a weekly ranking of the 40 U.S. counties (or county equivalents) with the highest per capita official COVID-19 cases and fatalities.

Again, I've separates the states into two separate spreadsheets:

Most of the data comes from either the GitHub data repositories of either Johns Hopkins University or the New York Times. Some of the data comes directly from state health department websites.

Here's the top 40 counties ranked by per capita COVID-19 cases as of Saturday, June 6th:

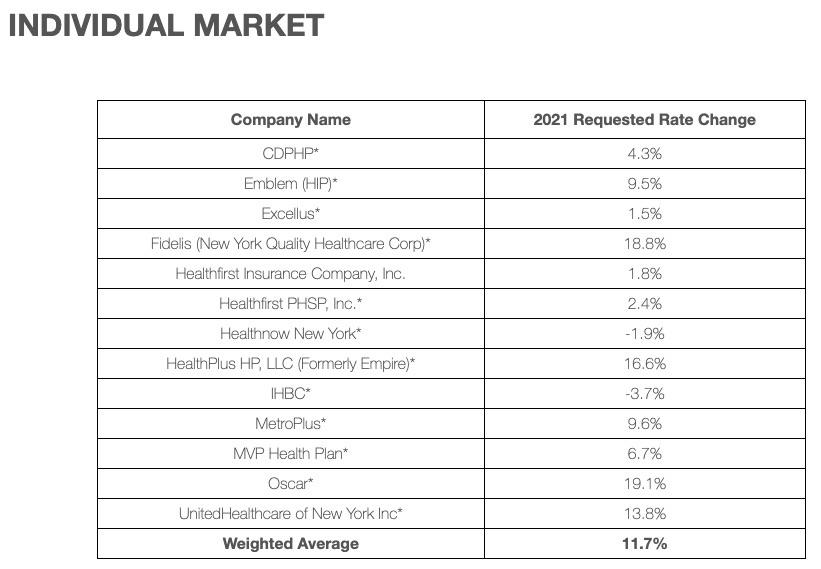

New York is the fifth state (well, fourth really) to announce their preliminary 2021 health insurance policy premium rate changes for the individual and small group markets (thanks to Michael Capaldo for the heads up):

NEW YORK STATE DEPARTMENT OF FINANCIAL SERVICES

2021 INDIVIDUAL AND SMALL GROUP REQUESTED RATE ACTIONS

6/5/2020

Health insurers in New York have submitted their requested rates for 2021, as set forth in the charts below. These are the rates proposed by health insurers, and have not been approved by DFS.

At long last, after many hours of data entry, here it is: The spread of COVID-19 across all 50 states over time, from March 20th through June 3rd, 2020, in official cases per capita.

I decided to only use every 3rd day (3/20, 3/23, 3/26, etc) in order to avoid as many one-day data reporting issues as possible (i.e., there were some cases where a state didn't update their numbers for 2 days in a row). I also gave up trying to tie every trend line to the state name; it simply gets too crowded near the bottom even with a small font size, so I've grouped some of them together where necessary.

I still hope to add the District of Columbia and U.S. territories (Guam, Puerto Rico, etc) but otherwise I should have everything fully up to date now, and should only have to plug in one day at a time going forward. I'll update this chart once a week if possible.

Since I've been neglecting other ACA/healthcare posts the past couple of weeks, I figured I should at least provide regular updates on why I've been mostly absent.

I've made major progress in updating and revising my breakout of COVID-19 cases and fatalities at not just the state level but the county level. Again, I've separates the states into two separate spreadsheets:

Denver -- Connect for Health Colorado® Chief Executive Officer Kevin Patterson released the following statement on the Health Care Coverage Easy Enrollment Program (HB 20-1236) after the bill passed through the General Assembly:

“I am excited that we can extend access to affordable health coverage for Coloradans with the simple act of checking a box. Easy Enrollment can provide financial stability and improve health outcomes for thousands of residents, many of whom are unfamiliar with the sign up process, or do not know they qualify for help. Through legislation such as Easy Enrollment, we work toward our goals of reducing the uninsured rate and educating Coloradans on the financial help we provide.”