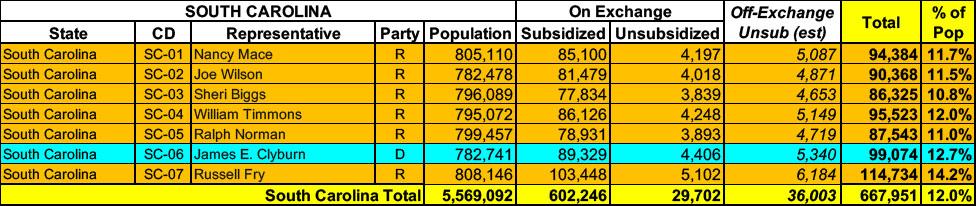

South Carolina has around ~632,000 residents enrolled in ACA exchange plans, 95% of whom are currently subsidized. I estimate they also have another ~36,000 unsubsidized off-exchange enrollees.

The proposed rate change of 27.3% applies to approximately 204,837 individuals. Absolute Total Care’s projected administrative expenses for 2026 are $90.21 PMPM. Administrative expense does not include $17.94 for taxes and fees. The historical administrative expenses for 2025 were $78.35 PMPM, which excludes taxes and fees. The projected loss ratio is 82.6% which satisfies the federal minimum loss ratio requirement of 80.0%.

With the pending dire threat to several of these programs (primarily Medicaid & the ACA) from the House Republican Budget Proposal which recently passed, I'm going a step further and am generating pie charts which visualize just how much of every Congressional District's total population is at risk of losing healthcare coverage.

USE THE DROP-DOWN MENU ABOVE TO FIND YOUR STATE & DISTRICT.

Unfortunately, South Carolina is another state where they don't make unredacted rate filings available, either on the state insurance dept website, the federal Rate Review websiteor the SERFF database.

As a result, I'm limited to unweighted averages for both the individual and small group markets:

It's worth noting that Cigna Healthcare is dropping out of the South Carolina individual market next year, while Aetna is pulling out of the small group market (see below).

Unfortunately, South Carolina is another state where they don't make unredacted rate filings available, either on the state insurance dept website, the federal Rate Review websiteor the SERFF database.

As a result, I'm limited to unweighted averages for both the individual and small group markets:

Individual Market: +3.7%

Small Group Market: +8.9%

UPDATED 11/07/23: A couple of interesting modifications were made in the individual market by state regulators: Blue Cross Blue Shield had their rate hikes cut from 6% to 2.7%; BlueCHoice was cut from 2.1% to essentially flat; Cigna will see a 17.8% average increase instead of their requested 10.5% hike; Molina drops from +6.4% to +4.6%; and Select Health, which had planned on reducing premiums by 4.6 points will instead see an average 1.3% increase. Huh.

The South Carolina Insurance Dept. has posted their final/approved 2023 rate filings for both the Individual and Small Group markets. Unlike the preliminary filings, which they didn't make easily available, the final filings are pretty clear cut. They don't include the enrollment data for each carrier, but most of that is available via the the federal Rate Review website and/or SERFF databases for the indy market. For the small group market, I was only able to find the number of policyholders, not actual enrollees, although that should still give a fairly close approximation to the relative market share.

On the individual market, average rates are going up around 7.3%, which is down a solid amount from the originally-requested average rate hike of 10.4%. The biggest news on SC's indy market is that Bright Health is dropping out (as they are everywhere else as well), while Cigna and Select Health are joining the ACA exchange.

On the small group market it doesn't look like there are any changes to who's participating. The average rate increase is 4.6%, which is actually down a bit from the 5.5% requested average (mostly due to Blue Cross/Blue Choice having their increases shaved down).

MICHIGAN: Another One (Mostly) Bites The Dust; 12th CO-OP Drops Off Exchange, May Go Belly-Up

It appears that East Lansing-based Consumers Mutual Insurance of Michigan could wind down operations this year as it is not participating in the state health insurance exchange for 2016.

But officials of Consumers Mutual today are discussing several options that could determine its future status with the state Department of Insurance and Financial Services, said David Eich, marketing and public relations officer with Consumers Mutual.

Consumers Mutual CEO Dennis Litos said: "We are reviewing our situation (financial condition) with DIFS and should conclude on a future direction this week.”

While Eich said he could not disclose the options, he said one is “winding down” the company, which has 28,000 members, including about 6,000 on the exchange.

The South Carolina Insurance Dept. website isn't particularly helpful when it comes to getting the annual rate filing data for these analyses--they post a link to the federal Rate Review website and the SERFF database, but that's it...and most of the filings don't show up in SERFF, while many Rate Review database actuarial memos are all heavily redacted.

Fortunately, this year the Rate Review database has Consumer Justification Narratives for 4 of the 5 carriers participating in SC's individual market (Bright Health Co. appears to be dropping out of the state's indy market). While the fifth one is missing (Molina), I can make an educated guess as to their enrollment based on South Carolina's total individual market size, which should be roughly 300,000 people, give or take.

Based on that, it looks like SC carriers are asking for around a 10.4% average rate hike in 2023.

For the small group market, all of the actuarial memos are redacted, so all I have is the unweighted 2022 average rate changes, which comes in at +5.4%.

Today, the Centers for Medicare & Medicaid Services (CMS) announced that Tennessee and South Carolina can begin offering Medicaid and Children’s Health Insurance Program (CHIP) coverage for 12 months postpartum to an estimated 22,000 and 16,000 pregnant and postpartum individuals, respectively, through a new state plan opportunity made available by the American Rescue Plan.

Tennessee and South Carolina join Louisiana, Michigan, Virginia, New Jersey, and Illinois in extending Medicaid and CHIP coverage from 60 days to 12 months postpartum. CMS is also working with another nine states and the District of Columbia to extend postpartum coverage for 12 months after pregnancy, including California, Indiana, Kentucky, Maine, Minnesota, Oregon, New Mexico, Pennsylvania, and West Virginia. As a result of these efforts, as many as 720,000 pregnant and postpartum individuals across the United States could be guaranteed Medicaid and CHIP coverage for 12 months after pregnancy.