Tennessee ACA exchange carriers were instructed to provide two sets of rate filings for 2026: One which assumes CSR reimbursement payments won't be reinstated, one which assumes they are reinstated. In addition, both sets of filings assume that IRA subsidies won't be extended; all but one carrier clarified how much extending the IRA subsidies would impact 2026 premium changes.

Alliant Health Plans: Alliant is requesting a nominal 0.3% increase next year if CSR payments aren't reinstated and a 1.0% drop if they are. In both cases, premiums would be 2.8% lower if IRA subsidies were to be extended by Congress:

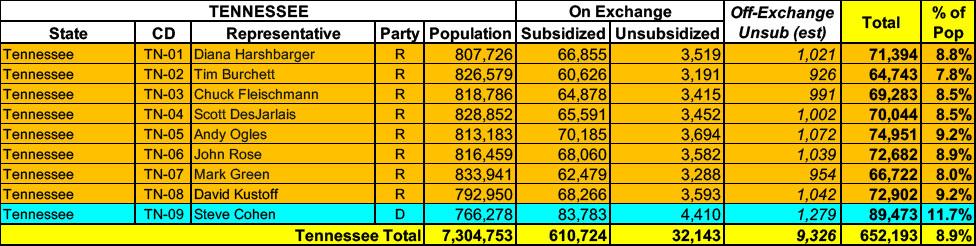

Tennessee has around ~642,000 residents enrolled in ACA exchange plans, 95% of whom are currently subsidized. I estimate they also have another ~9,000 unsubsidized off-exchange enrollees.

With the pending dire threat to several of these programs (primarily Medicaid & the ACA) from the House Republican Budget Proposal which recently passed, I'm going a step further and am generating pie charts which visualize just how much of every Congressional District's total population is at risk of losing healthcare coverage.

USE THE DROP-DOWN MENU ABOVE TO FIND YOUR STATE & DISTRICT.

Tennessee's preliminary 2025 individual & small group market health insurance rate filings are now available. Unfortunately, I can't find any unredacted filing forms for any of them (and in fact most of the rate filings aren't showing up in the SERFF database at all).

For the most part there's not much to see at first glance: Requested rate changes range from a 1.3% drop to a 3.9% increase on the individual market and from a 9.7% to 11.2% increase for small group plans. The unweighted averages are +1.4% and +10.6% respectively.

However, it also looks like several carriers are dropping out of each market in Tennessee: Alliant and US Health & Life (Ascension) don't show up on the federal Rate Review database for the individual market, while Aetna and CIGNA are missing for small group listings.

Assuming the exchange-based market makes up roughly 85% of total individual market enrollment in Tennessee, the total indy market should be around 628,000 people.

Note: I decided that while the original headline accurately reflected my feelings about this WSJ Op-Ed, it was a bit over the top, so I've changed it to something less crude.

For years, the Patient Protection & Affordable Care Act, generally shorthanded as the ACA or, more colloquially known as "Obamacare," was the top policy target of Republicans and other conservatives.

It seemed as though not a day went by without some right-wing opinion piece being published attacking the ACA for one thing or another. Once in awhile these attacks had some validity, but the vast majority were either completely baseless or grossly exaggerated.

And yet, after the dust settled on the infamous 2017 ACA "repeal/replace" debacle, it seemed as though the GOP had pretty much tired of their relentless assault on the healthcare law. They had failed to repeal it even with control of the White House, Senate, House of Representatives and Supreme Court, and ended up settling for zeroing out of the federal Individual Mandate Penalty as a consolation prize.

Tennessee's preliminary 2024 individual & small group market health insurance rate filings are now available, including actual enrollment numbers, which allows me to run weighted averages for both markets.

For the most part they're fairly straightforward: The individual market is looking at average rate increases of around 4.8%, while the small group market averages around +7.8% overall.

UPDATE 10/02/23: Well, all of Tennessee's filings appear to have been approved as is by the state regulatory department...they all say "approved" at the SERFF database and the newest filing versions all predate the original publication of this blog post from 8/17, so I'm concluding the preliminary rates are also the final rates.

Tennessee has posted their approved 2023 individual & small group market health insurance rate filings. For the most part they're fairly straightforward: The individual market is looking at average rate increases of around 8.5% (down a bit from the 9% average via preliminary filings), while the small group market averages around +3.0% overall.

The biggest news here is Bright Health is dropping out of Tennessee's markets. Bright's withdrawal will leave roughly 50,000 Tennessee residents to have to either manually pick a different plan from a different carrier or be automatically "mapped" to a similar plan to what they have now...via a different carrier.

MICHIGAN: Another One (Mostly) Bites The Dust; 12th CO-OP Drops Off Exchange, May Go Belly-Up

It appears that East Lansing-based Consumers Mutual Insurance of Michigan could wind down operations this year as it is not participating in the state health insurance exchange for 2016.

But officials of Consumers Mutual today are discussing several options that could determine its future status with the state Department of Insurance and Financial Services, said David Eich, marketing and public relations officer with Consumers Mutual.

Consumers Mutual CEO Dennis Litos said: "We are reviewing our situation (financial condition) with DIFS and should conclude on a future direction this week.”

While Eich said he could not disclose the options, he said one is “winding down” the company, which has 28,000 members, including about 6,000 on the exchange.

Tennessee has posted their preliminary 2023 individual & small group market health insurance rate filings. For the most part they're fairly straightforward: The individual market is looking at average rate increases of around 9%, assuming they're approved as is by state regulators, while the small group market averages around +2.9% overall.