(Aetna/CVS announced last spring that they're pulling out of the individual market in EVERY state in 2026.)

AmeriHealth Caritas Florida:

Amerihealth Caritas Florida, Inc. (AHC) has offered comprehensive and fully insured coverage to members in the individual ACA market since 2023. AHC is filing a rate increase for 2026 products. The plans associated with this filing will be offered both on and off the Federally Facilitated Marketplace (FFM) in Florida.

Every year, even when the ACA is running smoothly, there are always changes in market participation, as different insurance carriers enter or exit the individual market in certain states or either expand or shrink what parts of the state they offer healthcare policies in.

2026 is no exception, and given the massive turmoil the ACA exchanges are undergoing right now (due primarily to the expiring federal tax credits as well as regulatory changes made by the Trump Regime's so-called "Integrity & Affordability Rule"), there's either 13 or 32 insurance carriers throwing in the towel in one or more states, depending on how you count a carrier operating in multiple states or under multiple subsidiary brandings.

It's important to keep in mind that the following list probably isn't comprehensive--it includes the carriers which I've confirmed are pulling out statewide (with one exception: Meridian Health Plan of Michigan is only pulling out of parts of the state). There's likely one or two that I've missed, especially given that several of these have only made their final decisions within the past week or so.

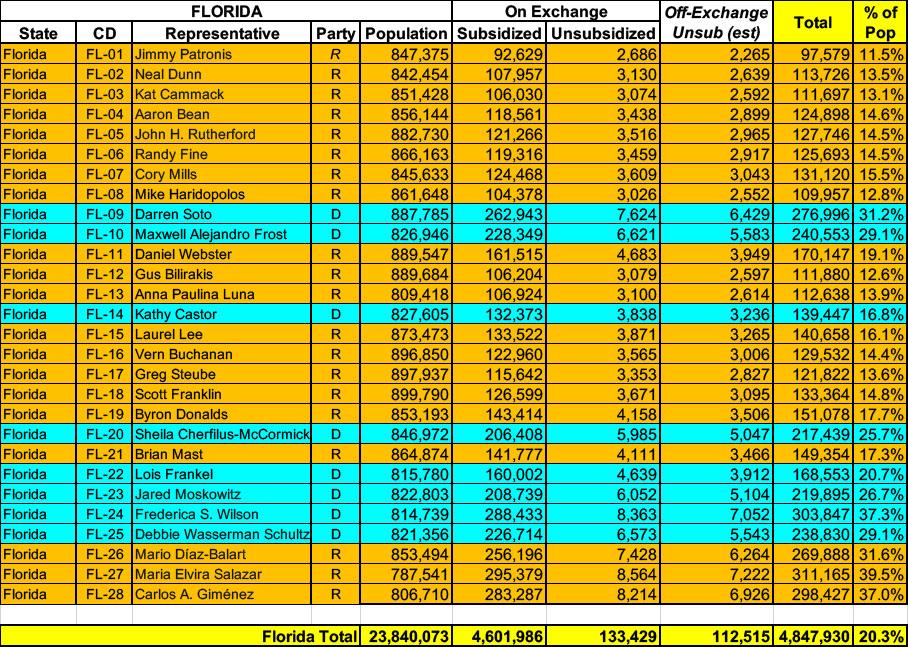

Florida has over ~4.7 MILLION residents enrolled in ACA exchange plans, 97% of whom are currently subsidized. I also estimate they have perhaps ~112,000 unsubsidized off-exchange enrollees.

Combined, that's over 4.8 million people, or a stunning 20.3% of their total population. 1 in 5 Floridians are enrolled in ACA exchange healthcare coverage (assuming CMS's 6.6% net national attrition rate applies to Florida specifically, the actual number of current enrollees is more like 4.5 million, or 19% of the state population).

With the pending dire threat to several of these programs (primarily Medicaid & the ACA) from the House Republican Budget Proposal which recently passed, I'm going a step further and am generating pie charts which visualize just how much of every Congressional District's total population is at risk of losing healthcare coverage.

USE THE DROP-DOWN MENU ABOVE TO FIND YOUR STATE & DISTRICT.

With the pending dire threat to several of these programs (primarily Medicaid & the ACA) from the House Republican Budget Proposal which recently passed, I'm going a step further and am generating pie charts which visualize just how much of every Congressional District's total population is at risk of losing healthcare coverage.

USE THE DROP-DOWN MENU ABOVE TO FIND YOUR STATE & DISTRICT.

Florida state law gives private corporations wide berth as to what sort of information, which is easily available in some other states, they get to hide from the public under the guise of it being a "trade secret." In the case of health insurance premium rate filing data, that even extends to basic information like "how many customers they have."

Gov. Ron DeSantis’ administration has filed suit to challenge a new federal requirement that specifies when children can be removed from the state’s Children’s Health Insurance Program.

...At issue is a Biden administration rule that took effect Jan. 1 requiring states to provide 12 months of continuous eligibility for enrollees ages 18 and younger under Medicaid and CHIP, even if monthly premiums are not paid.

Florida state law gives private corporations wide berth as to what sort of information, which is easily available in some other states, they get to hide from the public under the guise of it being a "trade secret."

In the case of health insurance premium rate filing data, that even extends to basic information like "how many customers they have."

A ‘Nixon goes to China’ moment? Conservative Republican pushes for state Medicaid expansion.

'These are not handouts. We’re not throwing money down the drain. We are helping our working class Americans get ahead.'

A conservative Florida Republican doctor who has been an ally of Gov. Ron DeSantis and his handling of COVID-19 says it’s time for the state to expand Medicaid despite the long-running opposition of GOP legislators.

...[Rep. Joel] Rudman said the loss of Medicaid coverage for hundreds of thousands of Floridians this year illustrates the need for change. A spreadsheet compiled by House Democrats shows of the 524,076 Floridians who have lost coverage in the last four months, nearly 50% are under the age of 21.

During the COVID pandemic emergency, Congress passed legislation which, among other things, required states to provide "continuous coverage" of people who enrolled in Medicaid or the CHIP program.

Normally Medicaid/CHIP enrollees have their eligibility statuses "redetermined" every month (or quarter in some states, I believe) to make sure they were still eligible for the program, but the Families First Coronavirus Response Act (FFCRA) stated that in order to receive increased federal funding of their Medicaid/CHIP programs, states couldn't kick anyone off as long as the public health emergency was in place (unless they died, moved out of state or asked to be disenrolled).

This requirement ended effective April 1st, 2023 via an omnibus bill passed back in December.