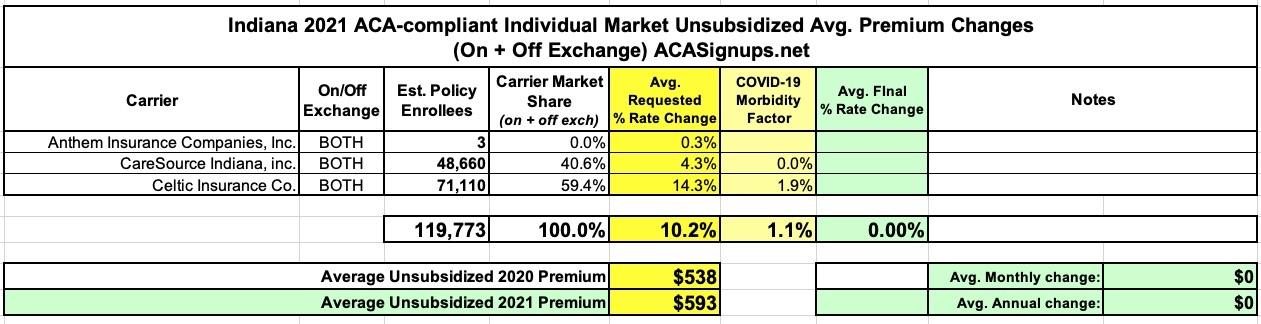

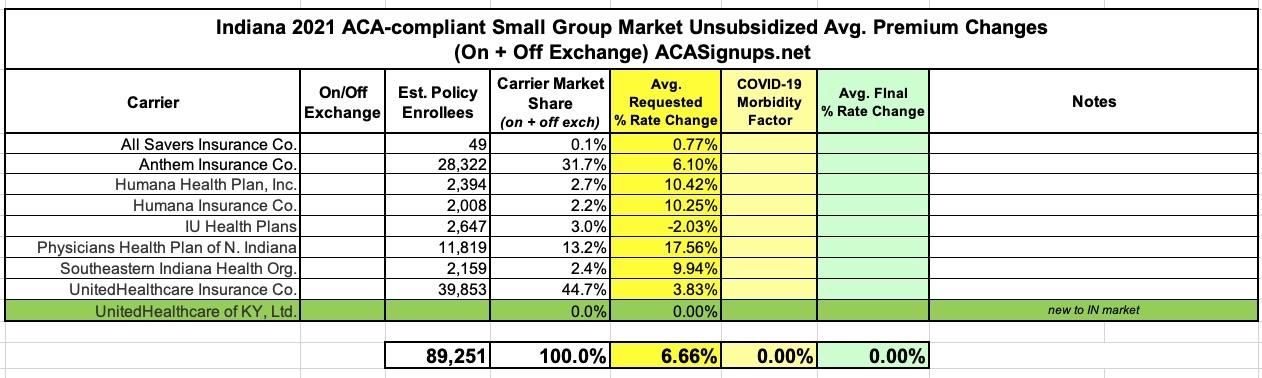

The Indiana Insurance Dept. has posted their 2021 individual & small group rate filings to the SERFF database. Nothing terribly noteworthy other than the average requested rate increase is unusually high for 2021 compared to most other states so far (10.2%, mainly via Celtic), and it looks like a second division of UnitedHealthcare is offering policies on the small group market next year:

Today, the CT DOI issued their final rate change rulings, and the difference are pretty dramatic:

Insurance Commissioner Issues Decisions For 2021 Health Insurance Rates

Insurance Commissioner Andrew N. Mais today announced the Department has made final decisions on health insurance rate filings for the 2021 coverage year. As a result of these decisions, approximately 214,600 Connecticut consumers are projected to save $96 million.

The Department approved an average increase for individual plans of 0.01 percent, down from the average request of 6.29 percent. The average increase for small group plans is 4.1 percent, down from the requested average of just over 11.28 percent.

The sections below include a summary of Ohio’s individual market for 2021. The data is based on product filings the Ohio Department of Insurance is currently reviewing.

Ohio’s Health Insurance Market 2021

For 2020, the department approved 10 companies to sell on the exchange. Based on the plan information the department approved, most counties had at least three insurers. 29 counties had two insurers, and just one county had only one insurer.

For 2021, the department approved those same 10 companies to sell on the exchange. Based on those filings, all counties will have at least two insurers and all but 10 counties will have three or more insurers.

Exactly one month ago, I posted an analysis of the preliminary 2021 premium rate filings for Georgia's individual and small group market carriers. At the time, the requests from the individual market carriers ranged from a 22.8% reduction to as much as an 18.3% increase.

I've also repeatedly noted that estimates by the carriers of the impact of the COVID-19 pandemic is pretty much all over the place. While a few carriers have indeed baked in significant rate hikes in response to COVID, most either don't mention it at all in their preliminary filings or, if they do, state that they expect the net impact to be negligible. However, they also make sure to hedge their bets by reserving the right to re-file their 2021 requests with adjusted COVID impact.

Oklahoma Consumers to Have More Health Options for 2021 ACA Plans

OKLAHOMA CITY – Insurance Commissioner Glen Mulready announced today the 2021 preliminary rate filings for health insurance plans under the Affordable Care Act (ACA). Insurers that currently offer coverage through the Oklahoma Marketplace filed plans requesting average statewide increases of 2.7 percent.

The same three insurers that offered individual health plans on the 2020 Exchange will return for 2021 — Blue Cross Shield of Oklahoma (BCBSOK) , Bright Health and Medica Insurance Company. In addition, Oscar Health, UnitedHealthCare (UHC) and CommunityCare Oklahoma (CCOK) will join the marketplace in Oklahoma for 2021 allowing consumers to have more choices. BCBSOK and Medica offer statewide plans while Bright Health, CCOK, Oscar and UHC serve limited areas of the state.

Moderate rate increase requests and new insurers looking to offer plans in Oklahoma revealed that the Oklahoma insurance market is stable and able to offer multiple health insurance options for all Oklahomans.

As I just noted with my Arizona post, the federal Rate Review database website heavily redacts the rate filing forms submitted by insurance carriers, making it impossible to run a weighted average even when all of the individual and small group market carrier rate change requests are readily available.

The good news is that the federal Rate Review database has now posted the preliminary avg. 2021 rate filings for the individual and small group markets for every state. This makes it very easy to plug in the average requested rate changes in 2021 for every carrier participating in both markets.

The bad news is that most of the underlying filing forms are heavily redacted, meaning I can't use the RR database to acquire the other critical data I need in order to run a proper weighted average: The number of people actually enrolled in the policies for each carrier.

This means that in cases where this data isn't available elsewhere (either the state's insurance department website, the SERFF database or otherwise), I'm limited to running an unweighted average. This can make a huge difference...if one carrier is requesting a 10% increase and the other is keeping prices flat, that's a 5.0% unweighted average rate hike...but if the first carrier has 99,000 enrollees and the second only has 1,000, that means the weighted average is actually 9.9%.

Large Decreases in 2021 Premium Rates Expected in Individual Market

CONCORD, NH – The federal government has published information on proposed rates for New Hampshire’s health insurance exchange (https://ratereview.healthcare.gov/) in 2021.

The New Hampshire Insurance Department is reviewing 2021 forms and rates for individual health plans. For 2020, the second lowest cost silver plan was $404.60. The 2021 second lowest cost silver plan proposed premium rate is $318.95. This represents a 21.2% decrease.

It's important to note that the 21.2% decrease only refers to the difference between the 2020 benchmark and the 2021 benchmark plans. They aren't necessarily from the same carrier, and even if they are, that's not the same as the weighted average rate changes for all policies at all metal levels from all carriers.

Virginia is usually the first state to publicly post their preliminary annual individual/small group market health insurance premium rate filings; historically they've published them as early as mid-April. This year, however, due primarily to the COVID-19 pandemic, I presume, they didn't actually post them until mid-August.

The average premium changes for 2021 on the individual market range from a 13% drop to a 7.7% increase, with the statewide weighted average coming in at around a 7.2% reduction. For the small group market, premiums are increasing by around 3.6% on average, ranging from a 2.4% drop to a 10.9% increase.

Two other noteworthy items: First, Optimum Choice is expanding into VA's individual market (this isn't the same as Optima Health); secondly, VA's indy market has dropped from over 300,000 last year to around 256,000 this year, presumably due to the lingering effects of Medicaid expansion enrollees shifting over from subsidized private plans.

The Indy market is about as simple as it gets since there's only a single carrier offering ACA policies either on- or off-exchange (Highmark BCBS). They're actually cutting premiums on average slightly next year, by half a percent. They state in their summary that "Covid19 is expected to increase claim costs in 2021"...but that's all they have to say about it. The full actuarial memo includes an extensive section about the COVID-19 impact factor...but the numbers/percentages are all redacted: