The first thing that's important to understand about the Indiana insurance market is that there are two carriers leaving the individual (ACA) market, and one possibly (?) leaving the small group market next year.

Every year, even when the ACA is running smoothly, there are always changes in market participation, as different insurance carriers enter or exit the individual market in certain states or either expand or shrink what parts of the state they offer healthcare policies in.

2026 is no exception, and given the massive turmoil the ACA exchanges are undergoing right now (due primarily to the expiring federal tax credits as well as regulatory changes made by the Trump Regime's so-called "Integrity & Affordability Rule"), there's either 13 or 32 insurance carriers throwing in the towel in one or more states, depending on how you count a carrier operating in multiple states or under multiple subsidiary brandings.

It's important to keep in mind that the following list probably isn't comprehensive--it includes the carriers which I've confirmed are pulling out statewide (with one exception: Meridian Health Plan of Michigan is only pulling out of parts of the state). There's likely one or two that I've missed, especially given that several of these have only made their final decisions within the past week or so.

Rate Watch is a convenient way for Hoosiers to access key data on Accident and Health rate filings submitted to the IDOI on or after May 1, 2010. Use it to determine which companies have requested rate changes, their originally requested overall % rate change, and the overall final % rate change approved. These are overall rate changes and are not individually specific. The table below is searchable and sortable. You can also download your filtered results by pressing the Save Excel File button at the bottom of the table. If you need the full data set, including a few additional columns, you can download the CSV file.

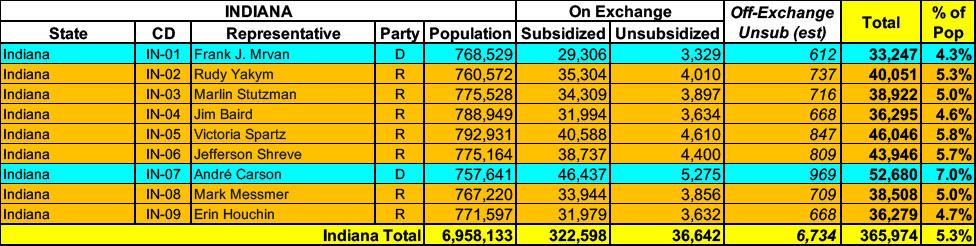

Indiana has around 359,000 residents enrolled in ACA exchange plans, 90% of whom are currently subsidized. I estimate they also have another ~6,700 unsubsidized off-exchange enrollees

Every year around this time I start my annual individual & small group market rate filing analysis project. This involves spending months painstakingly tracking every insurance carrier rate filing for the upcoming year to determine just how much average insurance policy premiums on the individual market are projected to change.

Carriers tendency to jump in and out of the market, repeatedly revise their requests, and the confusing blizzard of actual filing forms sometimes make it next to impossible to find the specific data I need.

The actual data I need to compile my estimates are actually fairly simple, however. I really only need three pieces of information for each carrier: How many effectuated enrollees they have in ACA-compliant policies this year; the average projected rate change for those policies; and, ideally, a breakout of the rationale behind the changes.

Usually the reasons given are fairly vague things like "increased morbidity" (ie, a sicker risk pool) or the like. Sometimes, however, there's a very specific reason given for some or all of the premium changes. Major examples of this include:

With the pending dire threat to several of these programs (primarily Medicaid & the ACA) from the House Republican Budget Proposal which recently passed, I'm going a step further and am generating pie charts which visualize just how much of every Congressional District's total population is at risk of losing healthcare coverage.

USE THE DROP-DOWN MENU ABOVE TO FIND YOUR STATE & DISTRICT.

The overall proposed average rate increase for 2025 Indiana individual marketplace plans is -1.6%.

The IDOI will finalize the review of the 2025 ACA compliant filings both on and off the federal Marketplace by August 16, 2024. The Centers for Medicare and Medicaid Services (CMS) will issue the ultimate approval for the Marketplace plans sold in Indiana. CMS will issue its approval on or before September 18, 2024.

Indianapolis – The Indiana Department of Insurance is issuing a warning to Hoosiers seeking health insurance coverage through the Federal Marketplace. The department advises caution regarding websites offering rewards like debit or cash cards in exchange for signing up through them. These “lead generating” websites collect users’ personal information and may provide inaccurate information about insurance coverage. The department urges Indiana residents to exercise skepticism regarding third-party websites promoting marketplace health plans and incentives.

“Consumers should verify information directly through official marketplace resources before entering any personal details or selecting a plan,” stated Alexandria Peck, Indiana Department of Insurance Chief Deputy Commissioner of Compliance. If you suspect fraud, contact the Indiana Attorney General’s office.

The IDOI will finalize its review of the 2024 ACA compliant filings both on and off the federal Marketplace by August 17, 2023. The Centers for Medicare and Medicaid Services (CMS) will issue the ultimate approval for the Marketplace plans sold in Indiana. CMS will issue its approval on or before September 20, 2023.