IMORTANT UPDATE: As I suspected, it turns out that the stray rate filing posted to the California Insurance Dept. website a few days ago was posted prematurely, doesn't reflect the carrier's final* rate filing, and has since been pulled from the California Insurance Dept. website.

I've been asked to remove the filing data, and seeing how there's nothing nefarious about it (I wasn't "whistleblowing" evidence of anything criminal/unethical), I'm complying with that request. Since everything in the post related to that data, there wasn't much point in keeping the rest of it either.

*(Yes, I'm aware that none of these early filings are "final" since they tend to be revised/resubmitted throughout the summer/fall, but you know what I mean.)

...and to absolutely no one's surprise, GOP sabotage of the ACA will be directly responsible for a significant chunk of the individual market premium increases.

Every year for 3 years running, I've spent the entire spring/summer/early fall painstakingly tracking every insurance carrier rate filing for the following year to determine just how much average insurance policy premiums on the individual market are going to increase (or, in a few rare instances, actually decrease).

The actual work is difficult due to the ever-changing landscape as carriers jump in and out of the market, their tendency repeatedly revise their requests, and the confusing blizzard of actual filing forms which sometimes make it easy to find the specific data I need and sometimes make it next to impossible.

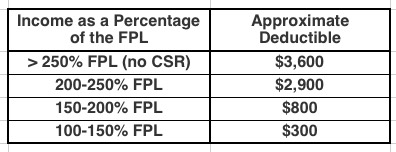

The Affordable Care Act (ACA), in section 1402, requires insurers who participate in the marketplaces established under that act to offer CSRs to eligible people who purchase silver plans through the marketplaces. CBO views that requirement as establishing an entitlement for thoseeligible.

To qualify for CSRs, people must purchase a plan through a marketplace and generally have income between 100 percent and 250 percent of the federal poverty guidelines (also known as the federal poverty level, or FPL). The size of the subsidy varies with income.

CSRs reduce deductibles and other out-of-pocket expenses like copayments. For example, in 2017, by CBOs estimates, the average deductible for a single policyholder (for medical and drug expenses combined) with a silver plan varied according to income in the followingway:

I've written quite a bit about the attempt by the GOP-controlled state legislature to push through work requirements for ACA Medicaid expansion here in Michigan. The bill (SB897) was quickly passed on partisan lines in the state Senate last week, and has now been taken up by the appropriations committee in the state House.

I actually shlepped my butt all the way out to Lansing yesterday morning to attend the committee hearing. Unfortunately, there were so many others who wanted to speak during the Public Comment period, I didn't get a chance to chime in.

As noted a few days ago, I've posted Part One of my latest crudely-produced-but-hopefully-informative video explainer.

The first part gives an overview of how healthcare Risk Pools actually work and why quarantining sick people into a separate High Risk Pool is such a terrible idea.

The second part, which I hope to post in the next few days, will go into why Donald Trump's recent Short-Term/Association Plan executive order will make a problem which already existed in 2017, and which was made worse by the GOP (by design) in 2018, even worse starting in 2019.

NOTE: Just to clarify, here's where the headline comes from:

...Sponsoring Sen. Mike Shirkey, R-Clarklake, created exemptions in the Michigan legislation that would waive the work requirement for parents with young children, pregnant women or caretakers for disabled family members. But asked about people like Maitre who could still lose health care, he told reporters the social safety net “by definition, has a lot of holes in it.”

“The best safety net ever invented by God is family,” Shirkey said, “but I’m not sure that government is supposed to supplement that process.”

Well, here we go:

#BREAKINGtomorrow morning the House Appropriations Committee is taking up SB 897. Another Republican attempt to take away healthcare from Michigan familieshttps://t.co/WsUhyntINj

Virginia’s Republican-led legislature is on the verge of doing something that would’ve been almost unthinkable just a year ago: approving legislation that would use money from the Affordable Care Act to expand Medicaid to as many as 400,000 people.

That coverage expansion would come at a price for Democratic legislators, progressive activists and low-income Virginians, however. Any Medicaid expansion bill that makes it out of the General Assembly will carry with it new work requirements for Medicaid enrollees, a priority for the GOP at large and for President Donald Trump’s administration.

Democrats in the Virginia legislature have tried in vain for six years to persuade their GOP counterparts that accepting federal dollars to extend Medicaid coverage to poor adults is the right thing to do. Accepting a work-requirements policy that would create bureaucratic obstacles to eligible Virginians appears to be the compromise needed to win the bigger fight.

HELENA — There are 91,563 Montanans participating in the Medicaid expansion HELP act as of Jan. 15, generating nearly $40 million in savings in Medicaid benefits, a state panel was told Thursday.

Members of the Legislature’s Children, Families, Health and Human Services Interim Committee reviewed a report on Medicaid expansion. The committee took no immediate action after hearing the report.

As noted earlier, I've been a bit lax with posting for a few days as I've worked on my latest 2-part video explainer about risk pools and #ShortAssPlans.

However, there's been a lot going on, so I figured I should try and at least do a quick update on a few items. First up: Medicaid expansion!

Here in my home state of Michigan, I've written several posts about how the GOP-controlled state legislature trying to shove through a draconian "work requirement" bill for Healthy Michigan, our name for ACA Medicaid expansion program which has been working just fine, thank you very much, for nearly 5 years now. The bill easily passed the state Senate (where the GOP holds a supermajority), and is now under consideration by the state House (where they have a smaller but still solid majority at the moment). The good news is that GOP Governor Rick Snyder--who championed passage of Healthy Michigan in the first place and seems to think it's fine mostly the way it is--is likely to veto the senate version of the bill. The bad news is that it might simply be tweaked somewhat by the House.

Price says that he's not a big fan of the GOP tax bill's 2019 individual mandate repeal-- says it will harm the pool in the exchange markets & drive up costs

Making my eyeballs roll even further back in my head, here's what Price said just nine months ago (shortly before he was given the boot from the HHS Dept.):