More than half a million Georgians have dropped health insurance coverage amid stiff premium price hikes for federally subsidized Affordable Care Act plans, according to data obtained by The Current GA and Georgia Recorder.

The 37% enrollment drop — from 1.5 million Georgians in January 2025 to 950,000 as of April 17, 2026 — dwarfs any previous decline in the state since the launch of so-called Obamacare health insurance plans in 2014.

Cost Increases from Washington’s Inaction Drives nearly 70,000 New Jerseyans to Drop Health Coverage since January

Expiration of Federal Subsidies Increase Health Care Costs for Working and Middle-Class New Jerseyans

Residents Urged to Stay Covered to Protect Their Health and Avoid Higher Out-of-Pocket Health Care Costs

TRENTON — -- Inaction by the Trump Administration and Congress to extend federal enhanced premium tax credits for consumers purchasing coverage through health insurance marketplaces under the Affordable Care Act has resulted in nearly 14% of those initially enrolled in health plans through Get Covered New Jersey to drop their coverage. As of April 15, 2026, total enrollment on the State Exchange stood at 440,362 – reflecting a net loss of 68,830 enrollees since the end of Open Enrollment.

The Massachusetts Health Connector is one of the handful of states operating their own ACA exchanges which publishes effectuated enrollment data on a monthly (actually weekly) basis, so let's take a look...

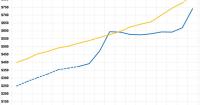

Officially, Massachusetts is one of the ten states in which Qualified Health Plan (QHP) selections during Open Enrollment actually increased year over year (by 3.7%).

However, as I expected and have warned about repeatedly, the year over year change in effectuated enrollment is a different story: While effectuated enrollment in January was actually 8.5% higher than January 2025, it has since dropped off rapidly and April 2026 enrollment is actually 4.3% lower than it was a year earlier...that's a swing of 14,000 more plan selections to over 15,000 fewer people actually enrolled.

Overall, average monthly effectuated enrollment is still up slightly for the first four months, but only by around 1,600 people.

Covered California, the state's ACA exchange, has published effectuated enrollment data for January & February 2026, so it's time to dig in and see what this might say about national trends.

Officially, Qualified Health Plan (QHP) selections during Open Enrollment were only 2.6% lower than they were in 2025. However, as I expected and have warned about repeatedly, the year over year drop in effectuated enrollment was higher than that in January (down to 1,839,000, a 2.8% drop y/y), and the gap more than tripled in February:

A couple of weeks ago, I received an email from a journalist who included this eyebrow-raising comment:

When I interviewed our Congressman, he said the ACA was a massive giveaway to insurers -- that premiums have increased 26% per year on average. That doesn't seem to match what little data I can scrape up, so I wanted to ask you: Since implementation in 2010, how much have premiums risen annually overall? Do you have data on how much or little they've risen or fallen for each year?

To this reporter's credit, he was skeptical about such a claim and reached out to me.

...I'm bringing all of this back up again today because I strongly suspect that the situation is about to reverse itself, with the Trump Administration already preparing to brag about impressive-sounding ACA enrollment numbers for 2026 in spite of the enhanced tax credits expiring less than 60 hours from now...even though the actual negative impact of the expiring tax credits (along with several other administrative policy changes made by CMS this year) likely won't be known for several months after Open Enrollment officially ends in January.

Connect for Health Colorado, the state's ACA exchange, has published effectuated enrollment data for January, February and March 2026, so it's time to dig in and see what this might say about national trends.

Unfortunately, it doesn't provide much demographic data (metal levels, income levels, etc), but it does at least provide the number of effectuated enrollees as well as new and terminated enrollments.

Below is what it looks like compared to the same months in prior years. I'm disregarding the COVID years (2020 - 2023) but am including 2016 - 2019 (none of which included the enhanced federal tax credits) as well as 2024 & 2025.

Officially, Qualified Health Plan (QHP) selections during Open Enrollment were only 1.9% lower than they were in 2025. However, as I expected and have warned about repeatedly, the year over year drop in effectuated enrollment was double that in January (3.8%), and the gap grew in both February and March. For the first quarter of 2026, effectuated enrollment in Colorado is down 5.3% vs Q1 2025.

Finally, there's nearly 1.1 million exchange enrollees who earn more than 400% FPL...although this total is actually closer to 2.15 million if you include enrollees whose household income is either "other" or "unknown:"

The application only collects household income data when consumers are requesting financial assistance.

Consumers that do not request financial assistance do not enter their household income information and are classified as having an “Other/Unknown FPL.”

There are a few SBEs that classify consumers who enter their household income information but are determined not eligible for financial assistance as “Other/Unknown FPL”. As a result, some SBEs report zero plan selections in certain income categories. Please refer to the Public Use Files Definitions document for additional information on these data.

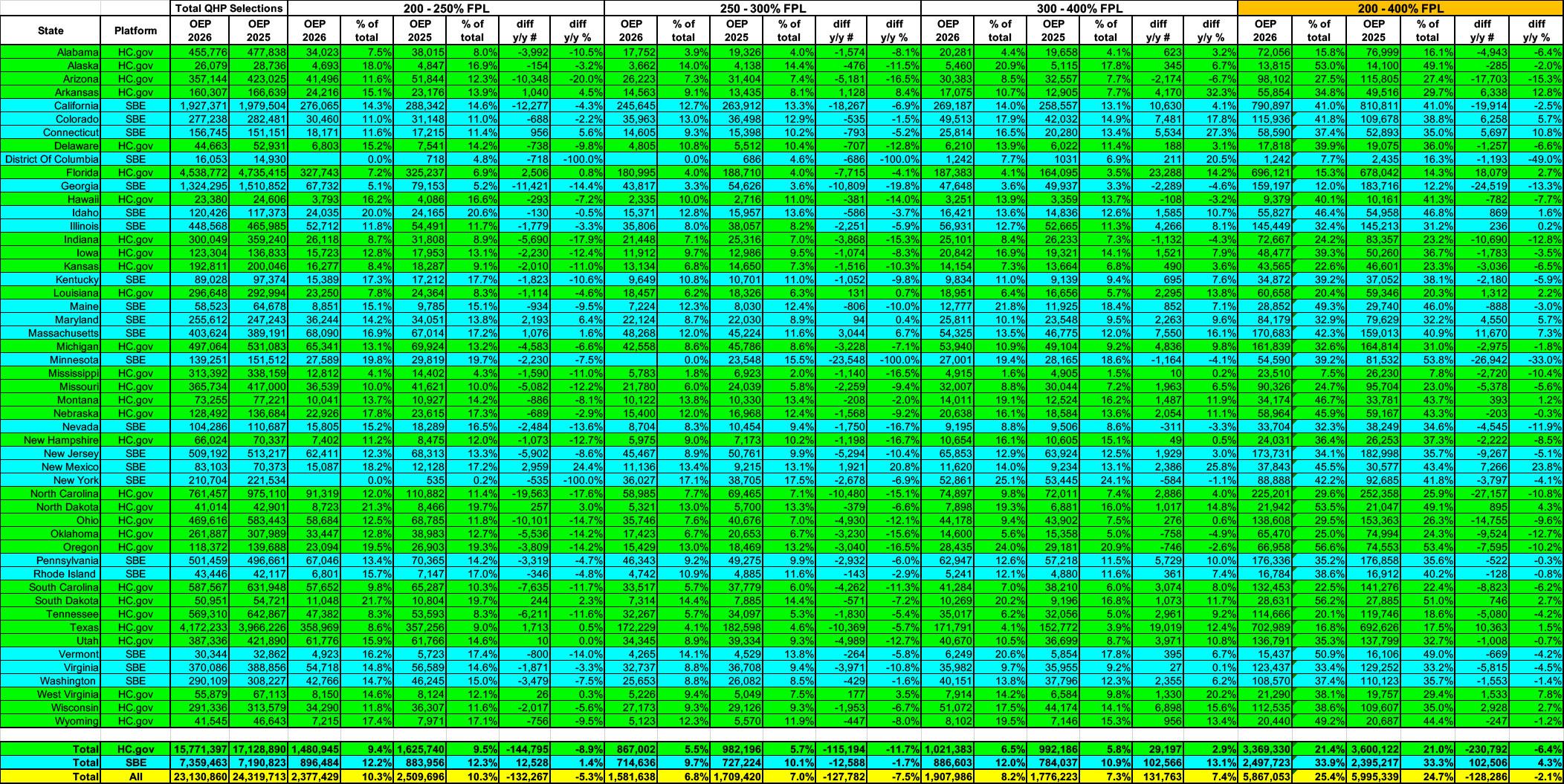

Next, let's look at the 200-400% FPL bracket. These make up just over 1/4th (25%) of total ACA exchange enrollment this year, up slightly from last year.

Overall enrollment in this bracket only dropped by about 2.1% (128,000 people), which makes sense for several reasons:

First, they were the least-impacted by the enhanced subsidies expiring (most of them still saw their premiums jump dramatically, just not as dramatically as those below 200% FPL or over 400% FPL)

Second, the Trump Regime policy change making recent (under 5 years) documented immigrant residents ineligible for federal tax credits doesn't really apply to this population anyway.

However, there's a third reason for the relatively small drop-off in this income range which I'll address below....