In U.S. politics, the Hyde Amendment is a legislative provision barring the use of federal funds to pay for abortion, except to save the life of the woman, or if the pregnancy arises from incest or rape. Before the Hyde Amendment took effect in 1980, an estimated 300,000 abortions were performed annually using federal funds.

HealthSource RI Open Enrollment 2026 closes with falling enrollment trend

Mar 9, 2026

PROVIDENCE, RI – HealthSource RI (HSRI) concluded its annual Open Enrollment (OE) period January 31, with enrollment totals and the mix of plan selections bearing out expectations, as customers faced increased monthly costs upon the expiration of enhanced federal premium tax credits. Individual and Family enrollments totaled 38,557 during this Open Enrollment, a 10-percent decline from the record-high close of OE2025 (42,695). Overall enrollment decreased by 20% from year-end (48,060) to the end of OE, a highly unusual development, as the marketplace has recorded growth nearly every year in that same span.

Over the past week or so, a few more state-based ACA exchanges have quietly published their final, official 2026 ACA Open Enrollment Period data, including Connecticut (157,246 plan selections), New Jersey (509,192), the District of Columbia (16,053) and Virginia (370,088). With these updates, practically all of the official 2026 OEP topline numbers are now filled in except for the following:

About a month ago, I once again reiterated that the official year over year ACA Open Enrollment Period plan selection drop from OEP 2025 to OEP 2026, which currently stands at around 1.26 million people (23.06M in 2026 vs. 24.32M in 2025) was incredibly misleading for a number of reasons:

Not only are there always some people who never have their enrollment effectuated in the first place due to either the policyholder actively cancelling their policy before it even begins or having it terminated by the carrier due to them not paying their first monthly premium, but that effectuated enrollment can vary widely from month to month due to the "churn" of people either starting or ending exchange coverage.

The main reason for pushing for 51 separate websites in the first place was mainly just an attempt to win over a few conservative "states rights" votes in Congress from Republicans and some conservative Democrats. There were some practical advantages to doing it this way as well (potential innovations from trying things different ways, plus a few states like Vermont and Massachusetts wanted to offer additional financial assistance beyond the normal tax credits/cost sharing provisions, and Hawaii already has an existing state law which is actually better than some of the provisions included via the federal exchange)...but on the whole, the sheer economy of scale advantages of one federal site make the downsides seem pretty small in comparison for most states.

Earlier this week the New Jersey Dept. of Banking & Insurance put out a press release with the final 2026 ACA Open Enrollment Period data for the state:

Enrollment Expected to Decline As Federal Changes Continue to Impact Affordability

TRENTON —More than 509,000 New Jersey residents enrolled in health insurance coverage for 2026 through Get Covered New Jersey, the state’s Official Health Insurance Marketplace, during the Open Enrollment Period. However, the state is cautioning that the full effect of the loss of federal subsidies has not impacted the marketplace yet and is predicting a material drop off in enrollment this Spring.

Today at the White House, Vice President J.D. Vance, Secretary of Health and Human Services (HHS) Robert F. Kennedy, Jr., and Administrator of the Centers for Medicare & Medicaid Services (CMS) Dr. Mehmet Oz announced new steps to crack down on fraud in Medicare and Medicaid to protect patients and taxpayers and improve affordability. The actions include deferring $259.5 million of quarterly federal Medicaid funding in Minnesota to prevent payment of questionable claims while further investigation is completed; a nationwide moratorium on Medicare enrollment for certain Durable Medical Equipment, Prosthetics, Orthotics, and Supplies (DMEPOS) suppliers; and a nationwide call to action for Americans to support fraud prevention, including stakeholder input on how CMS can continue to expand and strengthen its efforts.

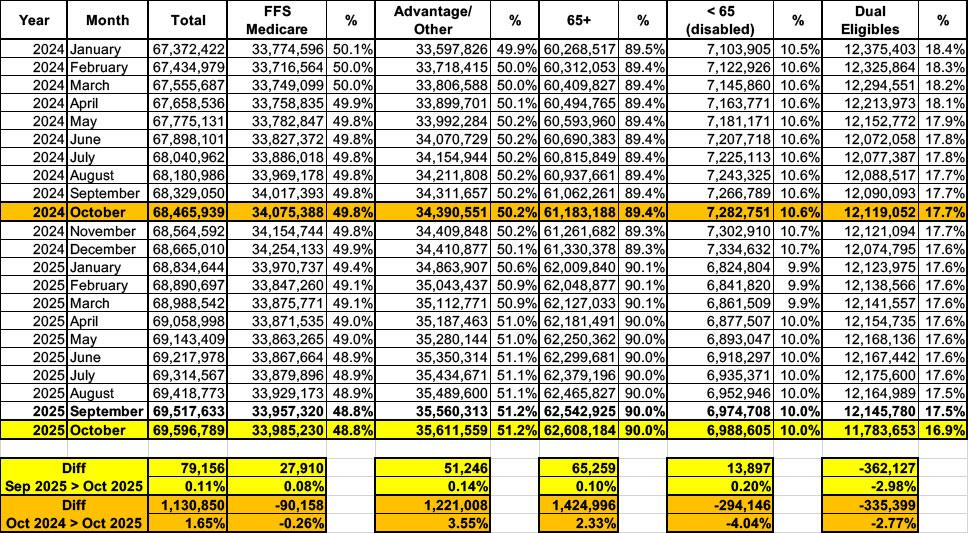

Whether the data posted since January 20, 2025 is accurate or not, I can't say for certain, but at least they're updating it...and so far, at least, I don't see anything in their monthly reports which is setting off any obvious red flags.

In any event, according to the latest report, as of November 2025:

{kind=link}