IMPORTANT:Premium Alignment is NOT a substitute for making the enhanced ACA tax credits permanent. It does little to help the lowest-income folks who are still better off with Silver plans thanks to robust CSR assistance, and the benefits of it will be mediocre for those over 400% FPL if the enhanced tax credits expire.

Even for those it benefits the most (primarily those who earn between 200 - 400% FPL), it's a complement to the upgraded subsidies, not a replacement for them.

HOWEVER, it's still hugely helpful to those who know how to take advantage of it, and particularly in the states newly implementing it, it should relieve a huge portion of the pain being caused by the enhanced APTC expiring next month.

West Virginia has ~67,000 residents enrolled in ACA exchange plans, 97% of whom are currently subsidized. They also have an unknown number of off-exchange enrollees (likely only a few thousand at most).

(unfortunately, CareSource WV's actuarial memo is heavily redacted)

Highmark BCBS WV:

Highmark West Virgina (“Highmark WV”) is requesting an average ACA individual market rate increase of 17.0%, ranging from 15.2% to 23.3%. Products submitted with this filing will have effective dates from January 1, 2026 to December 31, 2026. This rate change is projected to affect 28,179 members.

Historical Financial Experience:

Highmark WV incurred an underwriting gain in its ACA individual market programs in 2024.

With the pending dire threat to several of these programs (primarily Medicaid & the ACA) from the House Republican Budget Proposal which recently passed, I'm going a step further and am generating pie charts which visualize just how much of every Congressional District's total population is at risk of losing healthcare coverage.

USE THE DROP-DOWN MENU ABOVE TO FIND YOUR STATE & DISTRICT.

Well whaddya know? After years of their actuarial memos being redacted and/or filing summaries missing critical info, this year I'm suddenly able to access all the data I need!

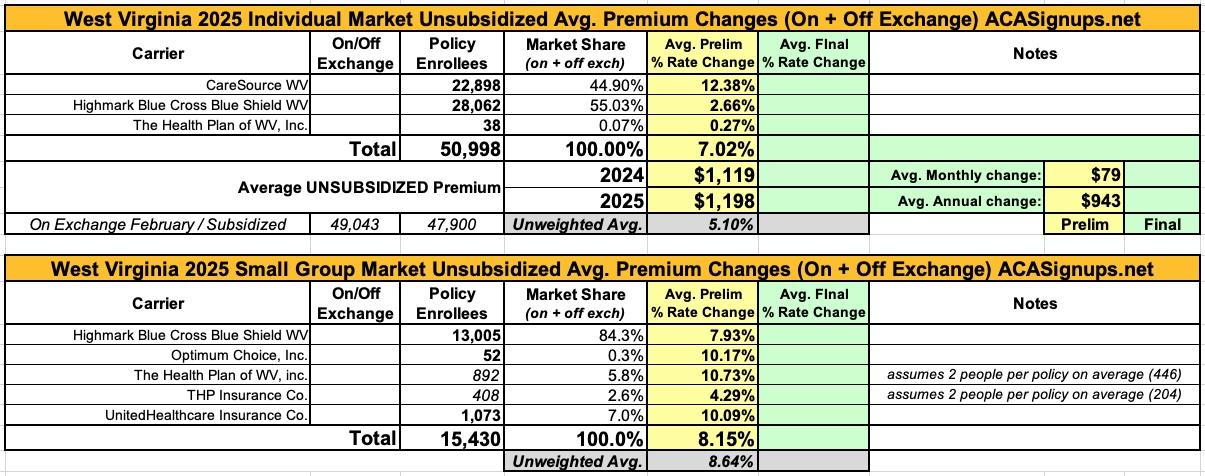

West Virginia carriers are asking for average rate hikes of 7% on the individual market and 8.2% for small group plans.

The 7% hike is pretty close to the average nationally on a percentage basis...but since West Virginia also already has by far the highest average unsubsidized premiums in the nation, that's ugly news, especially if the enhanced ACA subsidies provided by the Inflation Reduction Act are allowed to expire starting in 2026...

West Virginia is yet another state where I'm unable to acquire unredacted actuarial memos and/or filing summaries in order to run weighted average rate changes, so I have to settle for unweighted averages. On the other hand, on the individual market, at least, WV only has three carriers and their requested rate changes for 2024 are in a very narrow range anyway (from flat to a 2.1% increase), so it doesn't matter much.

The good news is that West Virginia's individual market rates are only increasing by around 1% next year, one of the lowest avg. rate increases in the country.

The bad news is that West Virginia already has by far the highest unsubsidized individual market rates in the nation, at nearly $1,200 per month (second highest this year is Wyoming at $965/month).

In any event, small group market carriers are requesting an unweighted average increase of 9.6% overall.

UPDATE 11/08/23: State regulators increased the rate h ikes from 1.1% to 3.0% for CareSource, but otherwise left the other carriers on both markets as is.

Last fall I noted that Oregon (along with Kentucky, although it looks like the latter got cold feet later on) may end up becoming the third state (after Minnesota and New York) to create a Basic Health Plan program which would provide comprehensive, inexpensive (or potentially free) healthcare coverage for residents who earn between 138% - 200% of the Federal Poverty Level (FPL)...basically, the next income tier above the cut-off for ACA Medicaid expansion. A few days ago, the state legislature passed a bill which would create a task force to put together their findings and recommendations no later than September 1st of this year.

West Virginia has by far the highest average unsubsidized premiums in the country (Wyoming and Alaska rank 2nd and 3rd). It also has the second smallest individual market in the U.S. (Alaska has the smallest), with just over 22,000 West Virginians enrolled in ACA policies statewide.

For 2023, they're looking at roughly a 5% rate hike for those who don't qualify for ACA subsidies. The good news is that, being West Virginia, the vast majority of those enrolled (95%) do qualify for financial help.

WV's ACA-compliant small group market is even smaller, just ~14,000 people; they're looking at roughly a 3.4% average rate hike next year.

Today, the U.S. Department of Health and Human Services (HHS), through the Centers for Medicare & Medicaid Services (CMS), approved the extension of Medicaid and Children’s Health Insurance Program (CHIP) coverage for 12 months after pregnancy in Indiana and West Virginia. As a result, up to an additional 15,000 people annually – including 12,000 in Indiana and 3,000 in West Virginia – will now be eligible for Medicaid or CHIP for a full year after pregnancy. With today’s approval, in combination with previously approved state extensions, an estimated 333,000 Americans annually in 23 states and D.C. are eligible for 12 months of postpartum coverage. If all states adopted this option, as many as 720,000 people across the United States annually would be guaranteed Medicaid and CHIP coverage for 12 months after pregnancy.

{kind=link}