I don't want to get out over my skis here; a single Senator saying that she supports something in an interview is a far cry from them actually voting to do so, especially when you'd need several more members of both the House and Senate (including the leadership of both chambers) to even hold that vote.

Even so, this is still a pretty significant development, given how thin the odds are of the improved subsidies included by the IRA getting extended are at the moment.

Nathaniel Herz: On the specific issue of the enhanced tax credits for the premiums for the individual marketplace health insurance plans — it seems like there is a real question about whether those continue...

Several fellow health wonks have chimed in. I spitballed perhaps 95%. Fann puts it at 96-97%. Cynthia Cox of the Kaiser Family Foundation thinks it could be even higher:

For several years now, I've been urging Congress to upgrade the Affordable Care Act via a series of major improvements. Most notable among these is the need to #KillTheCliff...that is, to eliminate the so-called "Subsidy Cliff" which kicks in for ACA individual market enrollees who earn more than 400% of the Federal Poverty Line (roughly $50,000 for a single adult or $103,000 for a family of four).

As I've explained many tmes, the ACA's subsidy structure works pretty well for those earning between 100 - 200% FPL, and is at least acceptable for those earning 200 - 400% FPL (in fact, thanks to #SilverLoading, it works quite well for most of that population as well). The real problem kicks in above 400% FPL (and to a lesser extent below 138% FPL for those living in the 14 states which still haven't expanded Medicaid). In addition, the subsidy formula still doesn't make policies truly affordable for many of those receiving them.

In short, both the upper- & lower-bound Subsidy Cliffs need to be eliminated, and the underlying formula needs to be strengthened as well.

For several years now, I've been urging Congress to upgrade the Affordable Care Act via a series of major improvements. Most notable among these is the need to #KillTheCliff...that is, to eliminate the so-called "Subsidy Cliff" which kicks in for ACA individual market enrollees who earn more than 400% of the Federal Poverty Line (roughly $50,000 for a single adult or $103,000 for a family of four).

As I've explained many tmes, the ACA's subsidy structure works pretty well for those earning between 100 - 200% FPL, and is at least acceptable for those earning 200 - 400% FPL (in fact, thanks to #SilverLoading, it works quite well for most of that population as well). The real problem kicks in above 400% FPL (and to a lesser extent below 138% FPL for those living in the 14 states which still haven't expanded Medicaid). In addition, the subsidy formula still doesn't make policies truly affordable for many of those receiving them.

In short, both the upper- & lower-bound Subsidy Cliffs need to be eliminated, and the underlying formula needs to be strengthened as well.

Regular readers know that I've been calling for Congress to #KillTheCliff for years:

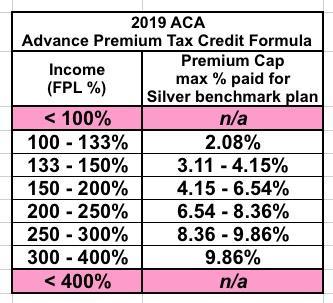

Once again: Under the ACA, if you earn between 100-400% FPL (between $12,140 and $48,560 for a single person), you're eligible for APTC assistance on a sliding scale. The formula is based on the premium for the Silver "benchmark" plan available in your area, which averages around $611/month in 2019.

Here's how the formula works under the current ACA wording:

...Here's the problem: If they earn exactly 400% FPL ($48,560), they'll also only have to pay 9.86% ($4,802), receiving $2,530 in subsidies for the year....