This just in via the Massachusetts Health Connector (by email):

253,253 January effectuations

6,247 February and March effectuations

4,643 plan selections

264,143 total enrollments/plan selections

The above includes 22,729 new enrollments, which includes people who never had Health Connector coverage in the past, or who did, dropped exchange at some point, and have come back for 2022.

This is up around 2,000 since December 25th, but is still down over 10% from last year, making Massachusetts one of only 5 state exchanges to see QHP enrollment drop year over year (to be fair, there's still a few days left for MA as well as Kentucky, DC and New York. The fifth is Hawaii. Having said that, enrollments in the other four states only runs through anywhere from December 15th - December 25th, whereas MA's total is current through yesterday.

Health Insurance Sign-Ups Reach Record High at Get Covered New Jersey as Open Enrollment Deadline Nears

Total signups of over 300k are highest ever in NJ since the start of ACA marketplaces in 2014

TRENTON – Department of Banking and Insurance Commissioner Marlene Caride today announced that more than 300 thousand New Jersey residents have signed up for health insurance at Get Covered New Jersey (GetCovered.NJ.gov) so far during the Open Enrollment Period—an increase of 21 percent compared to last year. The number of residents signed up for coverage is a record high for New Jersey, with more consumers signed up for marketplace coverage than during any prior Open Enrollment Period since passage of the Affordable Care Act.

Expanded Cost Savings Fuel Record Health Insurance Sign-Ups Through MNsure

Over 134,000 Minnesotans found coverage through Minnesota’s health insurance marketplace during open enrollment period

ST. PAUL, Minn.—A record number of Minnesotans signed up for private health insurance plans during MNsure’s recent open enrollment period. 134,257 Minnesotans signed up for 2022 health insurance coverage through the state’s health insurance marketplace between November 1, 2021, and January 15, 2022. The record number of sign-ups is 14,988 more than in the previous year’s open enrollment period and represents a 10% increase.

I'd proceed with caution about this figure, however. The official CMS Open Enrollment Periord report seems to always come in a few thousand lower than MNsure's official QHP tallies. Last year, for instance, the CMS report put Minnesota at 112,804, around 6,400 fewer than MNsure's 119,269 total.

NY State of Health and New York State Department of Financial Services Announce Extension of Open Enrollment Period as Federal Public Health Emergency Continues

I've included two of the key slides below, but there's a bunch of other demographic breakout stuff at the link above...financial assistance breakout, metal tiers, net premium data, etc.

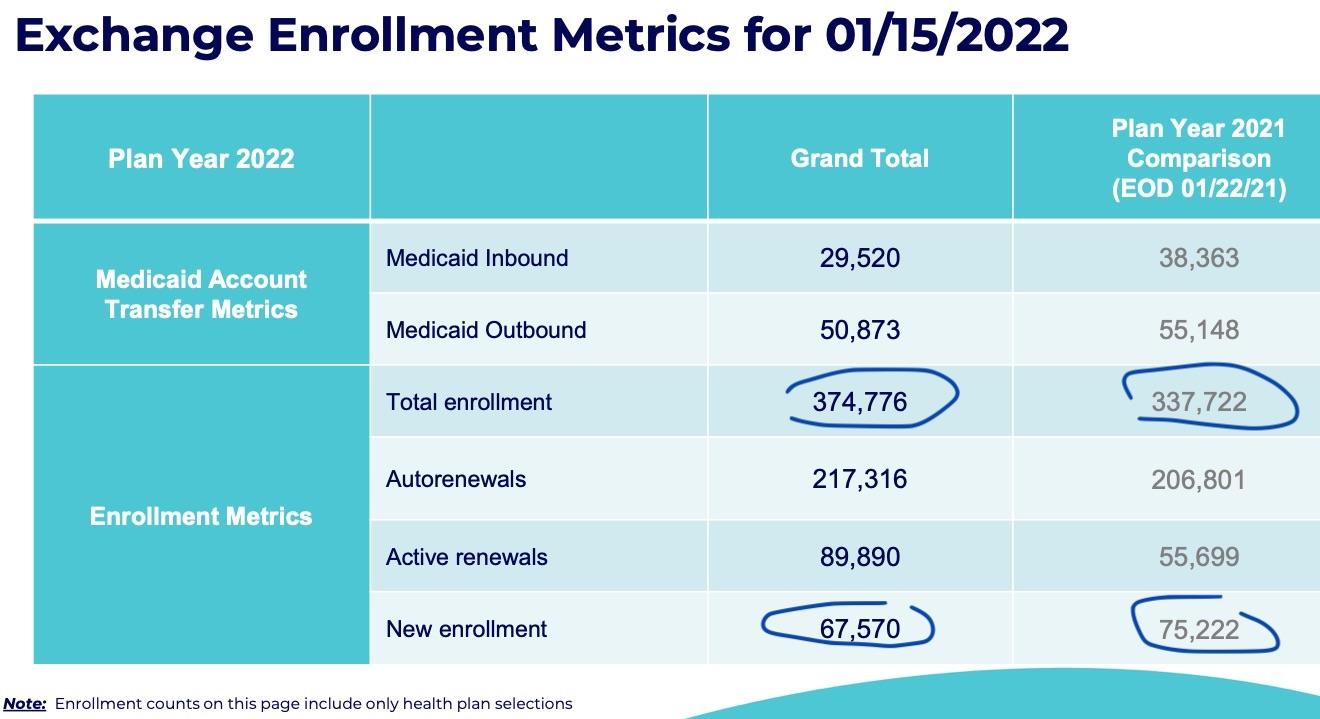

The main number: As of 1/15/21, 374,776 PA residents had selected or re-enrolled in Qualified Health Plans (QHPs) for 2022. This is up 11.0% vs. last year's final OEP total:

Renewals: Up 17.0% y/y

NEW enrollment: Down 10.2% y/y

That final mini-enrollment spike in the last couple of days of Open Enrollment is worth noting:

GOVERNOR ANNOUNCES EXTENSION OF OPEN ENROLLMENT THROUGH MARYLAND HEALTH CONNECTION AFTER A RECORD SEASON

More than 180,000 have enrolled for 2022, an all-time high and a 9% increase over last year

(JAN 18, 2022) ANNAPOLIS, MD – Gov. Larry Hogan today announced that open enrollment will continue on Maryland Health Connection through February in light of the ongoing public health emergency. A record number of Marylanders - 181,603 - have enrolled in coverage for 2022 through the state’s health insurance marketplace. A surge of new enrollees fueled the 9-percent increase over a year ago.

In fact, this is up 9.4% vs. last year, which itself was the previous all-tiime record for MD, I believe.

Donald Gerard McNeil Jr. is an American journalist. He was a science and health reporter for The New York Times where he reported on epidemics, including HIV/AIDS and the COVID-19 pandemic. His reporting on COVID-19 earned him widespread recognition for being one of the earliest and prominent voices covering the pandemic.

Trump Backs Boosters. Clearly, Someone Did the Math for Him.

Trump is losing hundreds of voters a day to Covid — far more than the margins in the swing states.

Math is not Donald Trump’s strong point.

Example: In 1988, he paid $408 million for the Plaza Hotel and spent millions making it gaudier. Seven years later, his creditors sold it for $325 million. And yet he styles himself a business genius.

For months I posted weekly looks at the rate of COVID-19 cases & deaths at the county level since the end of June, broken out by partisan lean (i.e, what percent of the vote Donald Trump received in 2020), as well as by the vaccination rate of each county in the U.S. (nonpartisan).

This basically amounts to the point when the Delta Variant wave hit the U.S., although it had been quietly spreading under the radar for a few months prior to that.

Now that we're a full month into the Omicron Variant wave, I've updated my case/death rate tracking to reflect that as well...because the data so far is showing a completely new chapter as we enter the 3rd year of the Coronavirus Pandemic.

The "start" of the Delta Wave was easy to lock in for my purposes; both cases and deaths from COVID had dropped off dramatically right up until around the end of June. The Delta Wave started showing up in the daily deaths pretty quickly as July started. The transition from the Delta to Omicron was a lot fuzzier, but I've decided to go with December 15th as my transition point.

I go by county residents who have received the 2nd COVID-19 shot only (or 1st in the case of the J&J vaccine).

(data for 3rd/booster shots aren't available at the county level in most states yet)

I base my percentages on the total population via the 2020 U.S. Census as opposed to adults only or those over 11 years old (or even over 4 years old).

For most states + DC I use the daily data from the Centers for Disease Control, but there are some where the CDC is either missing county-level data entirely or where the CDC data is less than 90% complete at the county level. Therefore:

NOTE: I've started using the official state health department dashboard for Virginia this week due to some weirdness in the COVID Act Now data. Unfortunately the VA Health Dept. dashboard doesn't allow you to export, view or download all 95 counties/city-counties at once, making this a tedious effort, so I'm not sure how I'll deal with it going forward.