Unfortunately, Alaska's 2021 rate filings aren't available via the state insurance department website or the SERFF database, and the actuarial memos posted to the federal Rate Review database are heavily redacted, so I can't run a weighted average rate change for either the individual or small group market.

The unweighted average changes, however, are a 2.0% reduction on the indy market and a 1.9% reduction for small group plans.

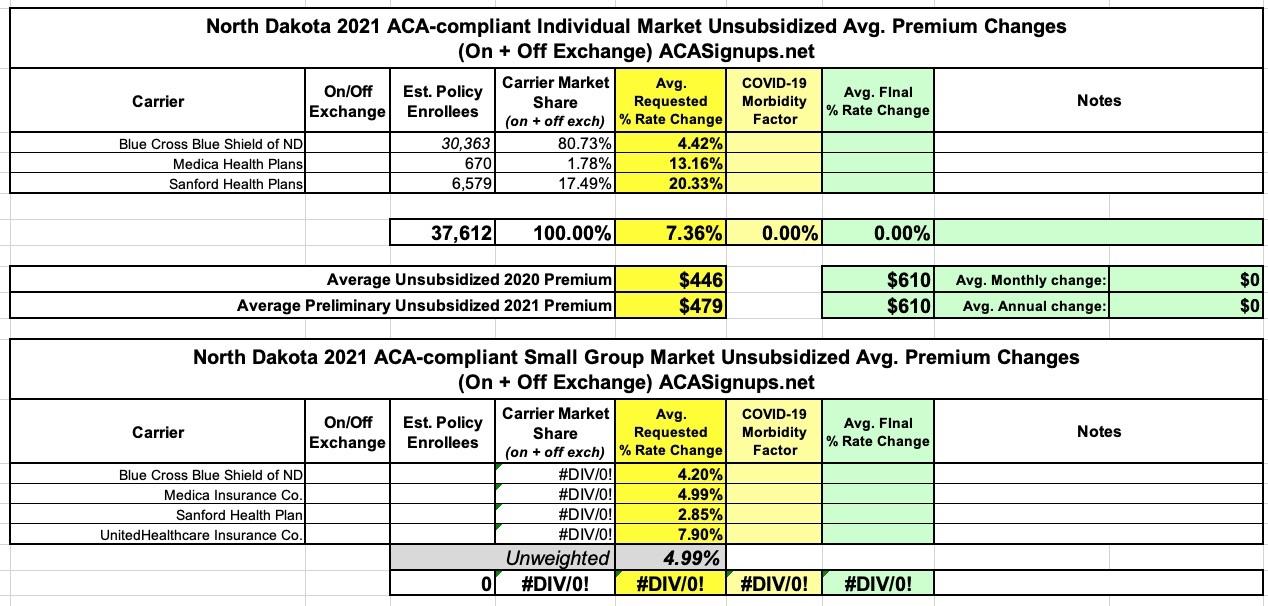

Here's North Dakota's 2021 individual & small group market rate change filings. Note that all of the small group filings are heavily redacted and the memos aren't available in the SERFF database for any of them, so I can't run a weighted average and had to go with the unweighted 5.0% increase.

For the individual market, Blue Cross Blue Shield's memo isn't available, so I had to plug in an estimate based on the average 2019 enrollment; I'm assuming it's fairly close to that this year as well. Weighted average on the indy market is a 7.4% increase.

The South Carolina Insurance Dept. released their final/approved 2021 Individual and Small Group Market premium rate changes.

I actually never got around to analyzing the preliminary rate filings for SC, so I don't actually know whether any of these are changes from the original filings, but whatever. In the end, the Palmetto State's individual market premiums will be dropping by about 1.5%, while their small group rates will be increasing by 4.7% on average.

It's also worth noting that UnitedHealthcare of SC is joining the South Carolina small group market for the first time next year (not to be confused with "UnitedHealthcare Insurance Co." and "UnitedHealthcare Insurance Co. of the River Valley...no confusion there I'm sure...)

South Dakota's 2021 individual & small group market rate filings are up, and there's not much to say about any of them: Individual premiums are going up around 2.6%, small group market policies around 2.8% overall statewide.

Now I have most of the data needed to analyze the individual market for 2021: Assuming no major changes in the approved rates, carriers are averaging around a 7.4% premium increase next year. This is actually unusually high for 2021 so far...other states are averaging less than 2% overall.

Most of the rate hike seems to be caused by Celtic/Ambetter ("Superior Health Plan"), which holds 1/3 of the entire market and is raising rates by nearly 12%. Blue Cross Blue Shield, which has another 36% market share, is only raising rates 3%, while the third and fourth largest carriers in the market, Molina and Oscar, are raising rates by 5.3% and 14.7% respectively.

There's also a couple of misleading numbers--both divisions of "Scott & White" are massively DROPPING their premiums for 2021, by 33% and 54%...but they have fewer than 2,000 people enrolled total to begin with; make of that what you will.

Utah's preliminary (and possibly final?) 2021 individual and small group market rate filings are listed below. Unless there's a change in the final/approved rates, individual marekt plan premiums will drop slightly by around 1.2% on average next year, while small group plans will increase by around 4.3%.

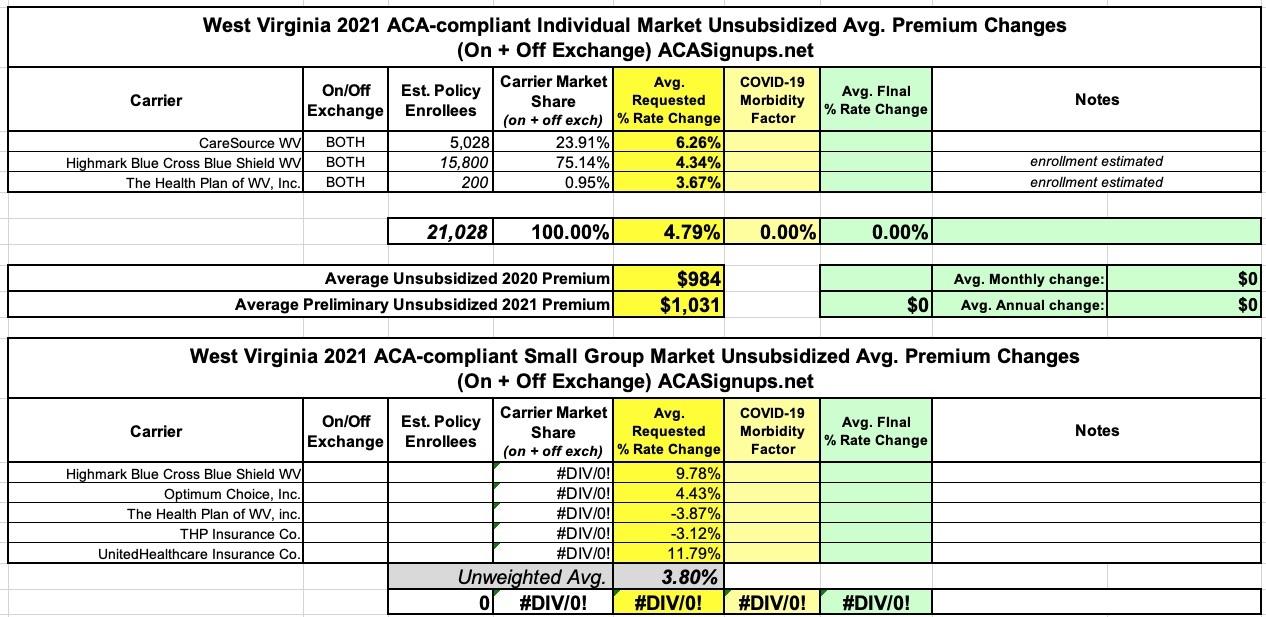

There are three insurance carriers offering ACA-compliant individual market plans in West Virginia: CareSource, Highmark BCBS and Optum, although Optum has barely any enrollees at all, and the other two combined only total around 21,000 people in the state. The preliminary 2021 rate filings for the WV individual marekt is around a 4.8% average increase.

I have no idea what the enrollment numbers are for WV's small group carriers, so I can't run a weighted average, but the unweighted average increase for 2021 comes in at around 3.8% across the five sm. group carriers:

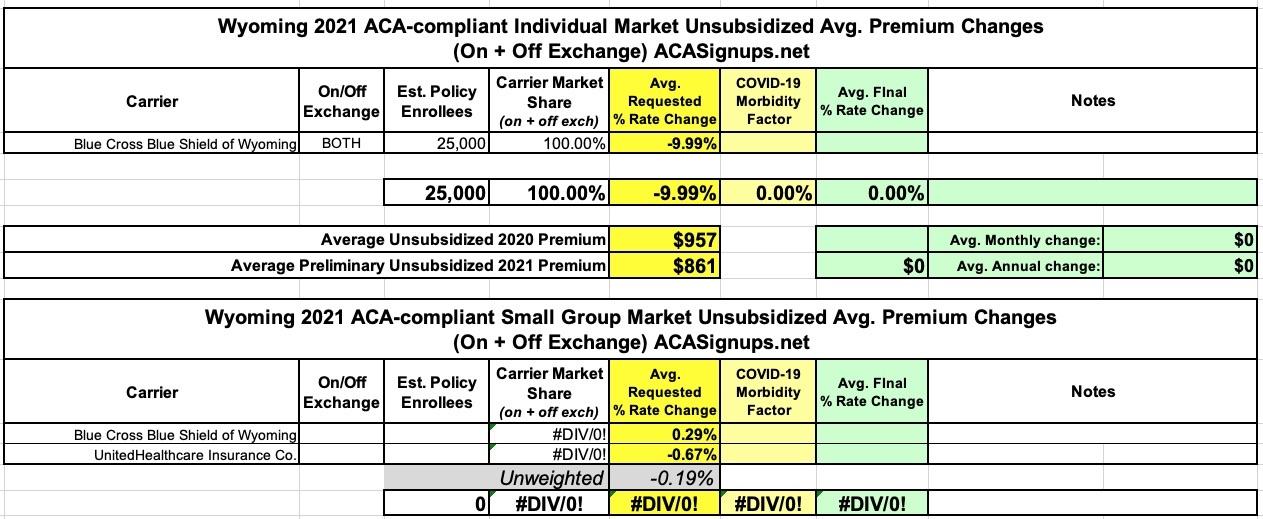

Not much to this one: Wyoming has just a single carrier selling ACA-compliant individual market policies to their 577,000 residents, Blue Cross Blue Shield...which, after raising rates 1.6% for 2020 is now reducing them by a solid 10% on average for 2021. The ~25,000 enrollment figure is an estimate.

For the small group market there are two carriers: BCBSWY and UnitedHealthcare, asking for an unweighted average rate reduction of 0.2% (I don't have a clue how many enrollees either one has).

First, CA's Small Group Market premiums are increasing by just 1.5% in 2021 (the lowest average increase since the ACA passed)

Second, CA's Individual Market premiums are increasing by just 0.6% on average in 2021 (identical to the preliminary rate requests)

Third, that Open Enrollment technically already started back on October 1st...sort of.

The official launch of Open Enrollment in every state isn't until November 1st, but for the past couple of years California has allowed current enrollees already in their system to actively renew/re-enroll for the upcoming year starting on October 15th. This year, it turns out they quietly moved that date back even earlier--current enrollees have been able to re-enroll starting as early as October 1st! I don't recall them ever making a big public announcement about this; I sort of stumbled upon it by accident.

Any music fan eager to bulk up their collection in the ’90s knew where to go to grab a ton of music on the cheap: Columbia House. Started in 1955 as a way for the record label Columbia to sell vinyl records via mail order, the club had continually adapted to and changed with the times, as new formats such as 8-tracks, cassettes, and CDs emerged and influenced how consumers listened to music. Through it all, the company’s hook remained enticing: Get a sizable stack of albums for just a penny, with no money owed up front, and then just buy a few more at regular price over time to fulfill the membership agreement. Special offers along the way, like snagging discounted bonus albums after buying one at full price, made the premise even sweeter.