As anyone not under a rock for the past few months knows by now, the improved federal Affordable Care Act tax credits which were put into place by President Biden and Congressional Democrats starting in 2021 are currently scheduled to expire at the end of December, just 2 1/2 months from now.

On top of this, the Trump Regime has also made administrative regulatory changes to how the ACA is structured resulting in the remaining tax credit formula becoming even less generous yet, while also eliminating eligibility for either financial assistance or even ACA enrollment whatsoever to many other Americans.

New Mexico has around ~70,000 residents enrolled in ACA exchange plans, 85% of whom are currently subsidized. I estimate they also have another ~8,000 unsubsidized off-exchange enrollees.

I already wrote about this over a month ago but it didn't get the attention it deserved at the time, and given that we're much closer to the actual 2026 ACA Open Enrollment Period starting and that there's been another important development since then, I figured I should post an updated entry about it.

Santa Fe, NM – The New Mexico Office of the Superintendent of Insurance (OSI) has approved 2026 rates for individual market Affordable Care Act (ACA) plans sold on and off BeWell, the New Mexico Health Insurance Marketplace, with an average increase of 35.7%. Today, 75,000 New Mexicans buy health insurance through BeWell and 88% of enrollees qualify for federal and state premium assistance.

Santa Fe, NM – The New Mexico Office of the Superintendent of Insurance (OSI) has approved 2026 rates for individual market Affordable Care Act (ACA) plans sold on and off BeWell, the New Mexico Health Insurance Marketplace, with an average increase of 35.7%. Today, 75,000 New Mexicans buy health insurance through BeWell and 88% of enrollees qualify for federal and state premium assistance.

However, there's an important caveat:

While it appears that Congress will allow enhanced federal Premium Tax Credits to expire, New Mexico’s Health Care Affordability Fund (HCAF) will cover the loss of the enhanced premium tax credits for households with income under 400% of the Federal Poverty Level (or $128,600 for a family of four), providing up to $68 million in premium relief for working families who enroll in coverage through BeWell in 2026. Federal and state premium assistance will continue to reduce the impact of the rate increases.

Blue Cross and Blue Shield of New Mexico (BCBSNM) is filing new rates to be effective January 1, 2026, for its Individual ACA metallic coverage. As measured in the Unified Rate Review Template (URRT), the range of rate changes for these plans is an increase of 18.4% to an increase of 49.6%.

The cost relativities among plans are different from the experience period to the prospective rating period due to anticipated non-uniform changes in network reimbursement levels. Additionally, the rates vary by plan due to the leveraging and utilization differences driven by variations in member cost sharing. Therefore, the proposed rates and rate changes may vary by plan.

Changes in allowable rating factors, such as age and geographical area, may also impact the premium amount for the coverage.

With the pending dire threat to several of these programs (primarily Medicaid & the ACA) from the House Republican Budget Proposal which recently passed, I'm going a step further and am generating pie charts which visualize just how much of every Congressional District's total population is at risk of losing healthcare coverage.

USE THE DROP-DOWN MENU ABOVE TO FIND YOUR STATE & DISTRICT.

For over a decade, State-Based Marketplaces have provided private health coverage to tens of millions of Americans, ensuring their health, well-being, and economic security. The Americans who depend on the Marketplaces include working parents, small business owners, farmers, gig workers, early retirees, and lower and middle-class individuals of all ages, political views, and backgrounds who drive our local economies and make both our rural and urban communities thrive.

The legislation under consideration in the House will severely impact the ability of these millions of Americans to continue to access this coverage and the health and financial security they depend on today. This will make for a sicker, less financially secure American public and strain hospitals and health care providers by increasing uncompensated care.

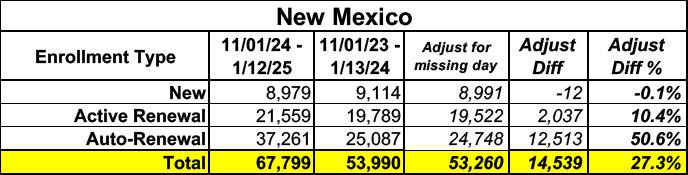

Not only is New Mexico's exchange enrollment up a whopping 28% vs. the same point last year, it's 20% higher than the 2024 OEP's final total of 56,472.

Not only is New Mexico's exchange enrollment up a whopping 28% vs. the same point last year, it's actually already 16.6% higher than the 2024 OEP's final total of 56,472!

Not only is New Mexico's exchange enrollment up a whopping 29% vs. the same point last year, it's actually already 16% higher than the 2024 OEP's final total of 56,472!