Covered California’s Enrollment Surges as People Sign Up to Benefit From the New Financial Help and Lower Premiums Now Available Through the American Rescue Plan

More than 76,000 people signed up for health insurance during Covered California’s special-enrollment period between April 12 and May 15.

The surge is more than 2.5 times higher than a traditional special-enrollment period, reflecting an increase of more than 46,000 people, compared to the same time period in 2019.

Covered California launched a special-enrollment period to allow the uninsured and those enrolled directly through a health insurance carrier to enroll and benefit from lower premiums due to the American Rescue Plan.

More than half of the Covered California households which are benefiting from the new and expanded financial help provided by the American Rescue Plan are getting high-quality coverage for $1 per month.

In order to start saving, Californians need to enroll by May 31 so they can begin benefiting from the new law on June 1.

Nevada Health Link Saves Thousands of Nevadans Money Through 2021 Special Enrollment Periods

CARSON CITY, Nev. (May 17, 2021) –Nevada Health Link, the online health insurance marketplace operated by the state agency, the Silver State Health Insurance Exchange (Exchange), has enrolled more than 7,600 Nevadans since the implementation of two Special Enrollment Periods in 2021, including more than 4,500 enrollees since April 20, attributed to the American Rescue Plan Act (ARPA or American Rescue Plan).

The American Rescue Plan, which was signed into law on March 11, provides Nevadans with a Special Enrollment Period where insured and uninsured Nevadans can take advantage of new, drastically reduced insurance premiums from now until August 15.

Huh. Vermont's ACA exchange website, Vermont Health Connect, has looked pretty much the same for at least the past 5-6 years, but a month or so ago they quietly overhauled the layout & design interface of the site. I have no idea if they actually updated the back-end, however.

There's no formal press release yet, but I've confirmed that the Nevada Health Link ACA exchange has enrolled 6,908 additional Nevadans in ACA exchange coverage via the COVID Special Enrollment Period as of yesterday (5/06) so far.

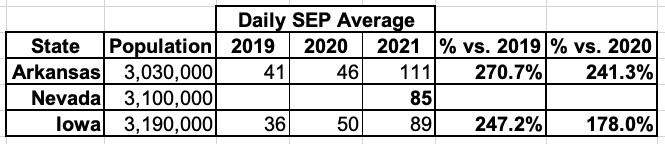

This breaks out to around 85 per day from 2/15 - 5/06.

Unfortunately, I don't have Nevada's 2019 or 2020 SEP enrollment handy for comparison, but NV's statewide population (3.10) is right in between Arkansas (3.03 million) and Iowa (3.19 million), which at least allows for a rough comparison:

This strongly suggests that Nevada's 85/day average is perhap 2.5x higher than 2019 and perhaps twice as high as 2020, although 2020 is a fuzzier comparison since HC.gov didn't have a COVID SEP last year while the Nevada Health Link did.

New television ads began airing today in four languages – Mandarin, Cantonese, Korean and Vietnamese – to let California’s Asian Americans know about the new savings provided by the American Rescue Plan.

The new ad campaign coincides with the start of Asian American and Pacific Islander Heritage Month.

More than 400,000 Asian Americans in California, including the uninsured and people enrolled directly through a health insurance carrier, stand to benefit from the new financial help that is now available.

Many Californians will be able to get a high-quality plan for as little as $1 per month, while currently insured consumers could save up to $700 per month on their coverage if they sign up through Covered California.

SACRAMENTO, Calif. — Covered California launched a new television ad campaign on Monday to raise awareness in California’s Asian American community about the new financial help now available through the American Rescue Plan. The ads, which are in Mandarin, Cantonese, Korean and Vietnamese, highlight how 400,000 Asian Americans can now get lower health insurance premiums starting June 1.

Every year, I spend months painstakingly tracking every insurance carrier rate filing for the following year to determine just how much average insurance policy premiums on the individual market are projected to increase or decrease, and over the years I have a pretty good track record of nailing the average unsubsidized premium changes in each state.

However, it's never going to be dead on target, for a number of reasons: Rounding errors in the rate filings, missing enrollment data, outdated enrollment data, last-minute filing changes and so forth. In some states I'm only able to find on-exchange enrollments and have to estimate the corresponding off-exchange number for each carrier; in some cases the percent changes being approved don't match from the official Uniform Rate Review Template (URRT) form to the Actuarial Filing Memo, and sometimes neither of them match up with what shows up at RateReview.HealthCare.Gov!

The American Rescue Plan provides new and expanded financial help that will dramatically lower health care premiums for people who purchase health insurance through Covered California.

Nearly 200,000 San Diegans, including the uninsured and people enrolled directly through a health insurance carrier, stand to benefit from the new financial help that is now available.

In order to maximize their savings, San Diegans need to enroll before the end of this month so they can begin benefitting from the new law on May 1.

Many people will be able to get a high-quality plan for as little as $1 per month, while currently insured consumers could save up to $700 per month on their coverage if they sign up through Covered California.

SACRAMENTO, Calif. — Covered California announced that San Diegans have until April 30 to sign up for health insurance coverage, and start benefitting from new financial help available through the American Rescue Plan as early as May 1st. The landmark law provides new and increased federal tax credits that will lower health care premiums for an estimated 200,000 people in the region.

The American Rescue Plan provides new and expanded financial help that will dramatically lower health insurance premiums for people who purchase coverage through Covered California

More than 400,000 Asian Americans in California, including the uninsured and people enrolled directly through a health insurance carrier, stand to benefit from the new financial help that is now available.

In order to maximize their savings, consumers need to enroll before the end of this month so they can begin benefitting from the new law on May 1.

Many Asian Americans will be able to get a high-quality plan for as little as $1 per month, while currently insured consumers could save up to $700 per month on their coverage if they sign up through Covered California.

SACRAMENTO, Calif. — Covered California announced the state’s Asian American community has until April 30 to sign up for health insurance coverage, and start benefitting from new financial help available through the American Rescue Plan as early as May 1. The landmark law provides new and increased federal tax credits that will lower health care premiums for more than 400,000 Asian Americans in California.

Final Deadline for 2021 Health Insurance is April 30

Last Chance for Idahoans to Receive Enhanced Subsidies

BOISE, Idaho – Your Health Idaho, the state health insurance exchange, announced the final day to enroll in 2021 health insurance, without a Qualifying Life Event, is April 30.

“This is the last chance for Idahoans to take advantage of the increased tax credits and enroll in 2021 coverage,” said Pat Kelly, Your Health Idaho Executive Director. “These savings can be significant for Idaho families who may have thought health insurance was out of reach prior to the American Rescue Plan Act.”

I've confirmed that unlike other state exchanges which have bumped out their deadlines repeatedly, Your Health Idaho explicitly does not intend on extending this deadline out again: April 30th is the final deadline.

After extending the special enrollment period deadline from March 31, exchange officials are urging Idahoans to apply for savings from a health insurance tax credit and make their final plan selection by 11:59 p.m. (MT) on Friday, April 30.

Nevada Health Link Announces Health Insurance Savings Through the American Rescue Plan Act

Nevadans seeking health coverage can access increased or expanded subsidies and premium savings, healthcare tax credits, expanded COBRA protections and increased plan options

CARSON CITY, Nev. (April 16, 2021) – Nevada Health Link, the online health insurance marketplace operated by the state agency, the Silver State Health Insurance Exchange (Exchange), is offering even bigger coverage savings to eligible uninsured and insured off-Exchange Nevadans. These new enhancements are in accordance with the newly-enacted American Rescue Plan Act (ARPA or American Rescue Plan) of 2021 passed by Congress and signed into law by President Biden on March 11, 2021.