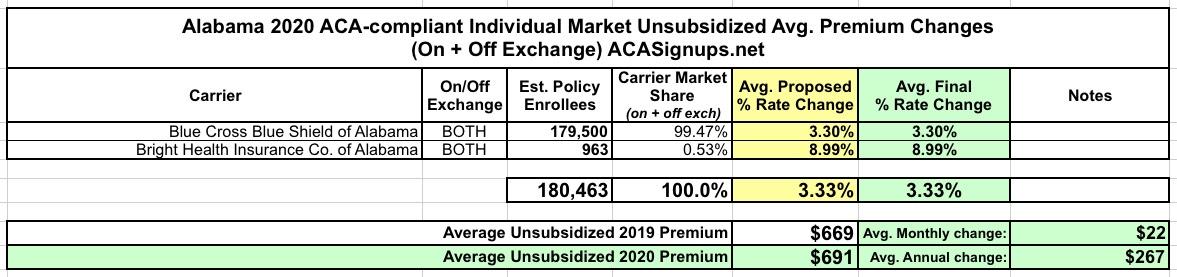

When I first ran the preliminary 2020 ACA premium rate filing requests for Alabama in August, I came up with a weighted average increase of 3.9%.

CMS has just posted the final, approved rates for Alabama's 2 carriers (Blue Cross Blue Shield and Bright Health). Both carriers had their requested rate hikes approved without any changes, but the final weighted average for unsubsidized enrollees still dropped a bit to 3.3%...because I had the wrong market share ratios. It looks like Bright has an even smaller share of the market than I thought (less than 1%), bringing the weighted average down a bit.

Back in March I wrote an analysis of H.R.1868, the House Democrats bill which comprises the core of the larger H.R.1884 "ACA 2.0" bill. H.R.1884 includes a suite of about a dozen provisions to protect, repair and strengthen the ACA, but the House Dems also broke the larger piece of legislation down into a dozen smaller bills as well.

Some of these "mini-ACA 2.0" bills only make minor improvements to the law, or in ways which are important but would take a few years to see obvious results. Others, however, make huge improvements and would be immediately obvious, and of those, the single most dramatic and important one is H.R.1868.

The official title is the "Health Care Affordability Act of 2019", but I just call both it and H.R.1884 (the "Protecting Pre-Existing Conditions and Making Health Care More Affordable Act of 2019") by the much simpler and more accurate moniker "ACA 2.0".

Back in March I wrote an analysis of H.R.1868, the House Democrats bill which comprises the core of the larger H.R.1884 "ACA 2.0" bill. H.R.1884 includes a suite of about a dozen provisions to protect, repair and strengthen the ACA, but the House Dems also broke the larger piece of legislation down into a dozen smaller bills as well.

Some of these "mini-ACA 2.0" bills only make minor improvements to the law, or in ways which are important but would take a few years to see obvious results. Others, however, make huge improvements and would be immediately obvious, and of those, the single most dramatic and important one is H.R.1868.

The official title is the "Health Care Affordability Act of 2019", but I just call both it and H.R.1884 (the "Protecting Pre-Existing Conditions and Making Health Care More Affordable Act of 2019") by the much simpler and more accurate moniker "ACA 2.0".

It's also important to keep in mind that due to how the ACA's subsidy formula is structured (combined with Silver Loading and Silver Switching), a lower benchmark premium will actually result in higher net premiums for many subsidized enrollees (although it's still good news for those who are unsubsidized). Here's why:

Let's say the unsubsidized premiums for a given enrollee in 2019 is $400 for Bronze, $600 for the benchmark Silver and $700 for Gold.

Let's say that enrollee earns exactly $32K/year (256% FPL), meaning they only have to pay 8.54% of their income for the benchmark plan.

That means they qualify for ($7,200 - $2,733) = $4,467 in subsidies ($372/month).

This would leave them paying $228/month for the benchmark Silver...but they can apply that towards a Bronze plan if they wish so they'd only pay $28/month, or a Gold plan so they only pay $328/month.

A week or so ago I noted that several of the 13 state-based exchanges (remember, Nevada split off of HC.gov this year) had opened up their ACA exchange websites for prospective enrollees to window shop for 2020 coverage. One of them, Covered California, actually started allowing people to enroll already; the rest were for comparison shopping only.

Well, as of today, residents of every state can window shop for 2020 healthcare policies, because HealthCare.Gov has followed suit and is now letting you plug in your household & income info to see what plans are available next year, what the unsubsidized premiums are, and (most importantly for a lot of people) what sort of financial assistance you may be eligible for.

There have been some interesting modifications to the interface and workflow of HC.gov this year:

OK, I know, I know, I'm obsessing over this and I promise to stop soon.

Yesterday I noted that due to a surreal, Rube Goldberg-esque series of events dating back to a different lawsuit filed back in 2014 by then-Speaker of the House John Boehner (!), it's looking very likely that the federal government will have to shell out at least $1.6 billion in Cost Sharing Reduction (CSR) reimbursement payments to over 100 health insurance carriers even though those carriers have already made up most of their losses elsewhere in the form of increased premium rates.

As I've noted several times recently, the "break off of HealthCare.Gov & establish your own state-based ACA exchange" train continues to pick up steam, with the following states having committed to either firing up their own, separate exchange website platform or at the very least going halfway by establishing their own exchange entity (which includes a board of directors, their own marketing/outreach budget, the ability to dictate which plans are allowed onto the exchange and so forth) if they haven't already done so.

HEARING ON "SABOTAGE: THE TRUMP ADMINISTRATION'S ATTACK ON HEALTH CARE"

Date: Wednesday, October 23, 2019 - 10:00am

Location: 2123 Rayburn House Office Building

Subcommittees: 116th Congress, Energy and Commerce (116th Congress), Oversight and Investigations (116th Congress)

The Subcommittee on Oversight and Investigations of the Committee on Energy and Commerce will hold a hearing on Wednesday, October 23, 2019, at 10 a.m. in the John D. Dingell Room, 2123 of the Rayburn House Office Building.

Premiums for HealthCare.gov Plans are down 4 percent but remain unaffordable to non-subsidized consumers

Today, the Centers for Medicare & Medicaid Services (CMS) announced that the average premium for the second lowest cost silver plan on HealthCare.gov for a 27 year-old will drop by 4 percent for the 2020 coverage year. Additionally, 20 more issuers will participate in states that use the Federal Health Insurance Exchange platform in 2020 bringing the total to 175 issuers compared to 132 in 2018, delivering more choice and competition for consumers. As a result of the Trump Administration’s actions to stabilize the market, Americans will experience lower premiums along with greater choice for the second consecutive year.