I haven't written anything about Pennsylvania's surprisingly bipartisan decision to break off of the federal ACA exchange at HealthCare.Gov onto their own state-based exchange since June:

After some last-minute drama in one state and a surprising lack of drama in another, both New Jersey and Pennsylvania have officially passed bills allowing them to each establish their own ACA exchanges and enrollment platforms, splitting off from the federal exchange and HealthCare.Gov:

Pennsylvania is poised to roll out its own online health insurance exchange to take the place of the one run by the federal government for the state's residents since 2014, saying it can save money for hundreds of thousands of policy-buyers.

Over the past few years, more and more of the state-based exchanges have shifted from waiting until the end of Open Enrollment to officially report auto-renewals of existing enrollees...to going ahead and auto-renewing everyone up front, and then subtracting those current enrollees who actively cancel their renewals.

This has caused a bit of confusion, since the exchanges don't always make it clear who's being counted and when.

Case in point: Access Health CT, Connecticut's ACA exchange. Last year they reported 12,777 enrollees during the first two weeks of Open Enrollment...and also noted that there were another 85,000 existing enrollees who hadn't yet actively renewed their policies as of 11/18.

For the past two weeks, along with other noteworthy Open Enrollment data numbers, I've been scratching my head over what the deal is in Mississippi:

Once again, Maine remains the worst-performer year over year, mostly due to their expansion of Medicaid. Idaho isn't listed because they're a state-based exchange and haven't reported any data yet. Mississippi, on the other hand, continues to be the top out-performer vs. last year, which is interesting because there doesn't seem to be any particular reason for it.

Unlike some states, Mississippi hasn't implemented any additional subsidies, a mandate penalty or a reinsurance program of any sort. They haven't had any new carriers join the ACA market, nor have any of them left. I don't think either of the carriers on the exchange have significantly expanded their territory or changed their offerings that much either...in fact, average premiums are essentially flat year over year.

In other words, by all rights, Mississippi should be performing almost exactly as they did last year...but enrollments are up 15.5% to date. Huh.

I just received the following 2020 Open Enrollment report from the Massachusetts Health Connector (via email, no link):

It looks like we’ve pretty much wrapped up auto-renewal, how about an update on 2020 enrollment:

As of Nov. 29, we had a total of 286,640 people enrolled in Jan. 1 coverage, 6 with February or March enrollments, and 10,852 who had selected plans and had not yet paid to enroll. So, by the CMS definition, we are at 297,498. That includes about 17,000 new enrollments from people who did not have coverage as of Nov. 4 with the Health Connector.

I wish every ACA exchange would break out their numbers this way. Simple and to the point, but also with relevant details...not only "renewals vs. new" but also how many are enrolled for Januar vs. Feb. or March coverage and even how many have/haven't paid yet! The last is a bit unfair since Massachusetts is one of only two states, I believe, which actually handle premium payments (Rhode Island does as well...Washington State used to but doesn't anymore).

I'm just putting this out there today because I know there's gonna be a bunch of eye-rolling stories completely misunderstanding the data later on this week.

Last Wednesday, the Week 4 HealthCare.Gov Snapshot Enrollment Report came out and showed a "mysterious" 41% increase in ACA exchange enrollments for the week vs. last year...jumping from 500,437 QHP selections to 703,556 QHP selections for the corresponding week this year.

This Wednesday, the Week 5 snapshot report will come out and will almost certainly show a "mysterious" large drop in ACA exchange enrollments vs. last year...from 772,250 down to perhaps 500,000 or so.

Around 7,000 or so of this drop will likely be due to Nevada splitting off onto their own ACA exchange. A small number will be due to Idaho expanding Medicaid. But the vast bulk of this seemingly disastrous ~35% drop will be for a far simpler reason...the same one which caused the seeming 41% spike last week: Thanksgiving.

The pace of Obamacare enrollment this year is up 9% so far in Georgia, a turnaround from declines since the beginning of the Trump administration. Nationwide, the pace of enrollment is up 2%.

Wait, what? Where on earth is she getting either of these numbers?

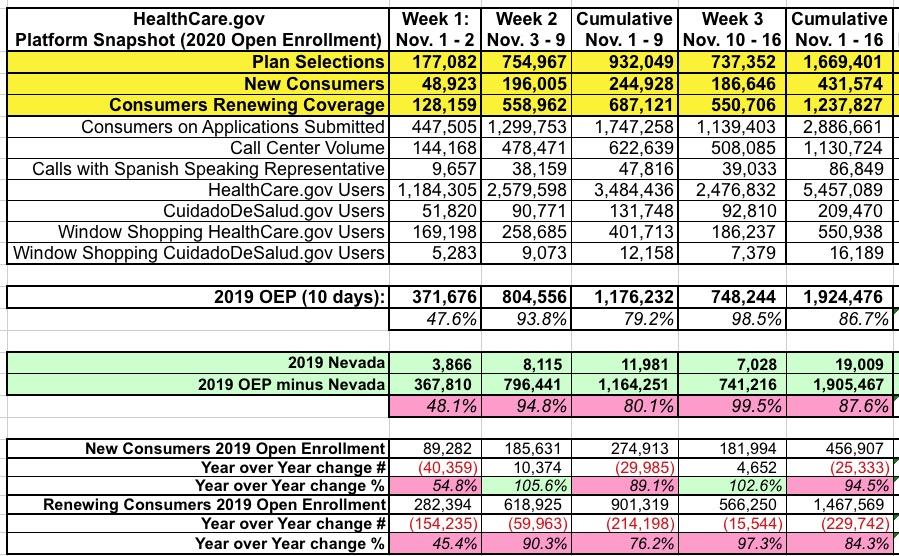

The Week 4 HealthCare.Gov Snapshot Report from CMS should be released at any time, covering enrollment in 38 states from Nov. 10th - Nov. 23th.

As a reminder, here's what the Week 3 report looked like:

There are two major things to account for when comparing the two years: First, there's a day missing due to Nov. 1st falling on a Friday instead of a Thursday this year. This likely accounts for around ~120,000 of the difference. Secondly, Nevada split off from HC.gov this year, which accounts for around ~19,000 of the gap the first 3 weeks. In addition, a small portion of the difference is likely due to Idaho and Maine expanding Medicaid; exchange enrollees earning between 100-138% FPL should be tranferred over to Medicaid instead.

IMPORTANT: As I've noted before, Covered California has arranged to expand and enhance their ACA premium subsidies beyond the official ACA formula starting with the 2020 Open Enrollment Period. Back in October, I posted a detailed analysis, complete with tables and graphs to explain just how much hundreds of thousands of Californians could save under the new, beefed-up subsidy structure.

However, Anthony Wright of Health Access California just called my attention to the fact that I made a major mistake in my analysis which impacted every one of the examples: I was basing them on the draft enhanced subsidy formula from back in May instead of the final version, which is considerably more generous at the upper end of the sliding scale than the draft version was!

In short:

The ACA formula caps premiums (for the benchmark Silver plan) at between 2 - 9.8% of household income but only if you earn between 100 - 400% of the Federal Poverty Level.

The draft California formula is a bit more generous from 100 - 400% FPL and also caps premiums between 9.9 - 25% of income between 400 - 600% FPL.

The final California formula is more generous yet: It's pretty much the same up to 400% FPL, but caps premiums between 9.8 - 18% of income between 400 - 600% FPL.

I've therefore gone back and re-calculated and re-written the entire blog post below with the updated, corrected subsidy formula. My apologies for the error!

----------

There's two important points for CA residents to keep in mind starting this Open Enrollment Period:

First: The individual mandate penalty has been reinstated for CA residents. If you don't have qualifying coverage or receive an exemption, you'll have to pay a financial penalty when you file your taxes in 2021, and...

Second: California has expanded and enhanced financial subsidies for ACA exchange enrollees:

Until now, only CoveredCA enrollees earning 138-400% of the Federal Poverty Line were eligible for ACA financial assistance. Starting in 2020, however, enrollees earning 400-600% FPL may be eligible as well (around $50K - $75K/year if you're single, or $100K - $150K for a family of four). In addition, those earning 200-400% FPL will see their ACA subsidies enhanced a bit.

Increased Visits to Food Pantries During Holiday Season Provide Opportunity to Reach Uninsured New Yorkers

ALBANY, N.Y. (November 25, 2019) – NY State of Health, the state's official health plan Marketplace, today announced its partnership with food pantries for the third holiday season to educate consumers about enrolling in high quality, affordable health insurance. Food pantries across New York will have certified enrollment assistors on-site throughout November and December to answer questions about health coverage options and how to enroll in a health plan. This year, the Marketplace is also offering eligible New Yorkers the option to receive information on the Supplemental Nutrition Assistance Program (SNAP) during the enrollment process.