But that's not all! In addition to the actual 2018 MLR rebates, I've gone one step further and have taken an early crack at trying to figure out what 2019 MLR rebates might end up looking like next year (for the Individual Market only). In order to do this, I had to make several very large assumptions:

Alabama only has two carriers offering Individual Market policies. Unfortunately, the rate filing forms are redacted in some states, so I'm having to patch together bits & pieces of data to try and estimate the weighted average rate changes. In the case of Alabama, the filing for Blue Cross Blue Shield lists 179,500 total individual market enrollees in 2018, but there's no data for 2019...while the filing for Bright Health Insurance (a relative newcomer to the market) doesn't list any enrollment data at all.

I'm assuming that BCBSAL holds a solid 90% of the market and that their total enrollment is around the same year over year. If so, that would give Bright around 20.5K enrollees and make the total Alabama Individual Market around an even 200,000 people. Again, assuming all of this is accurate, that means a weighted average increase of 3.9%, which in turn means unsubsidized enrollees are looking at average premium increases of around $26/month or $312 for the year.

NOTE: This has been corrected from an earlier version.

I realize this may seem a bit late in the game seeing how the 2019 ACA Open Enrollment Period has already started, but I do like to be as complete and thorough as possible, and there were still 9 states missing final/approved premium rate change analyses as of yesterday which I wanted to check off my 2019 Rate Hike Project list.

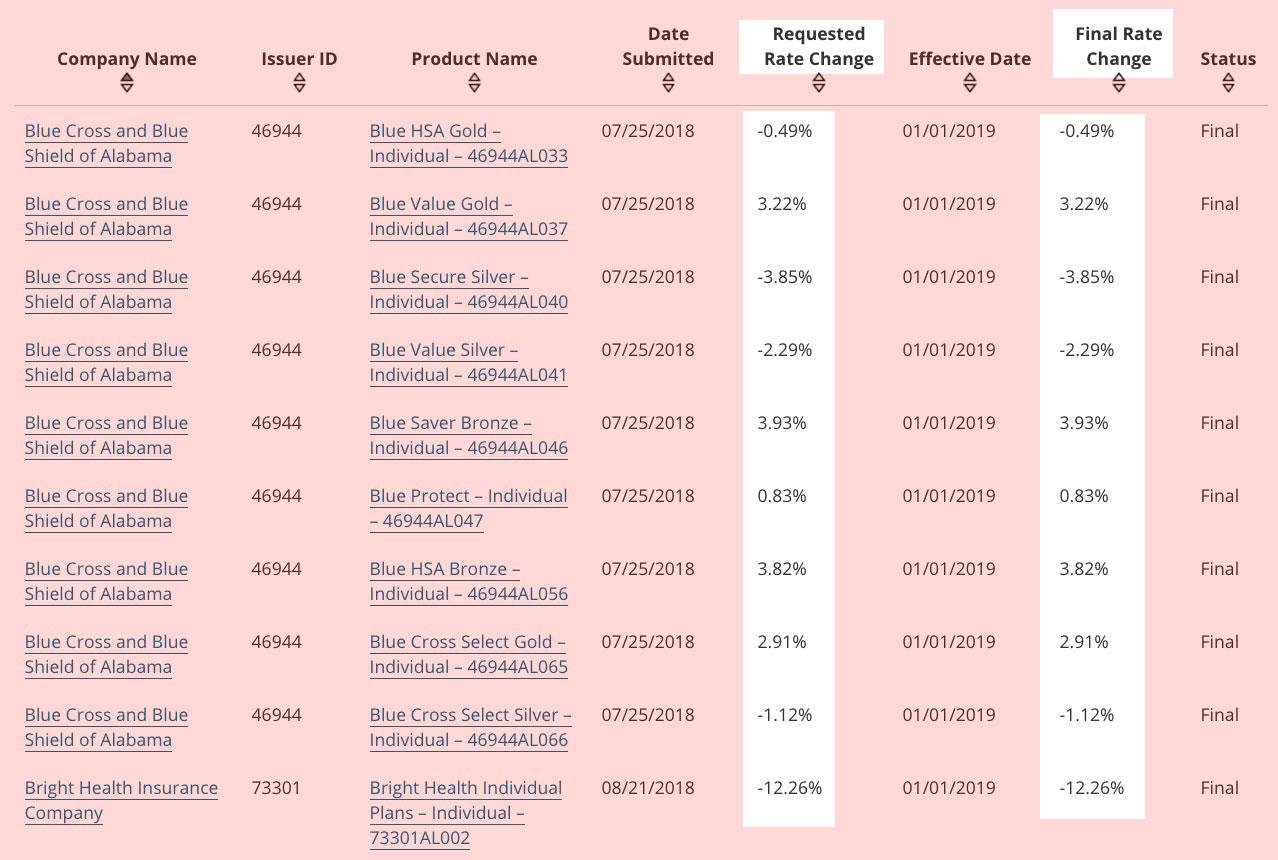

Fortunately, RateReview.HealthCare.Gov has finally updated their database to include the approved rate changes for every state, which made it easy to take care of most of these. Making things even easier (although not necessarily better from an enrollee perspective), in three states the approved rates are exactly what the requested rates were for every carrier: Alabama, Mississippi and Utah:

Last year Alabama had only a single insurance carrier, Blue Cross Blue Shield, offering individual market policies anywhere in the state. For 2018, a new carrier, Bright Health Insurance, jumped into the AL market. For 2019, both companies are lowering rates--BCBSAL is only dropping theirs slightly, but Bright clearly way overshot the mark out of the gate and is lowering their prices by 15.5% overall next year.

Unfortunately, neither of the filings clarifies just how many enrollees either has, so I don't know what the relative market share is; I'm going to assume that BCBS held onto about 90% of the total given their monopoly hold last year and the fact that Bright is a new/unknown player in the market (not to mention the fact that Bright seems to have overpriced their first year). Obviously I'll have to change this if I receive hard numbers to the contrary.

Earlier today I wrote an extensive post about California's individual market, specifically breaking out the number of off-exchange policies, including a rare look at some hard grandfathered plan enrollment numbers.

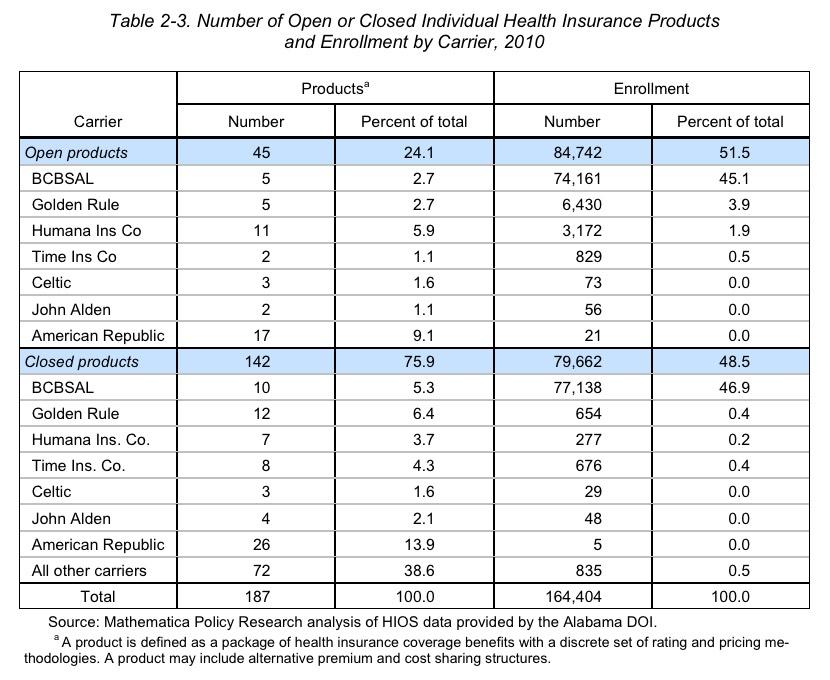

I've also managed to dig up a fascinating document from 2010 buried on the Alabama Insurance Department's website, which provides quite a bit of demographic insight into Alabama'soverall health insurance market. While all of this info is now 8 years out of date (and even precedes the first ACA open enrollment period), it does provide a few clues into estimating what's going on in Alabama today.

This first table shows exactly what Alabama's individual market looked like: 164,404 people were enrolled in pre-ACA "major medical" policies in 2010:

Alabama, which has refused to expand Medicaid for low-income adults under the Affordable Care Act (ACA), is now proposing to make work a condition of Medicaid eligibility for very low-income parents, stating that it wants to encourage work. Its proposal, however, actually would penalize work: because Alabama hasn’t expanded its program, those who comply with the new requirements by working more hours or finding a job will raise their income above the state’s stringent Medicaid income limits, thereby losing their Medicaid coverage and likely becoming uninsured.

Now that it appears that the full list of states and counties eligible for hurricane (or windstorm, in the case of Maine) Special Enrollment Periods (SEP) has settled down, Huffington Post reporter Jonathan Cohn asked an interesting question:

How if at all do you allow for the extensions in FL, TX, etc.? Or, to put another way, how many post-Dec 15 signups through https://t.co/bhGNSognZK do you expect?

The closest parallel to this particular situation I can think of was the #ACATaxTime SEP back in spring 2015. In that case, it was the first year that the ACA's (defunct as of this morning) Individual Mandate was being enforced, and a lot of people either never got the message about being required to #GetCovered or at least pretended that they didn't.

With only 5 days to go before the launch of the 2018 Open Enrollment Period, time is rapidly running out for me to wrap up my 2018 Rate Hike Project. I started this, as I have for 3 years now, back in late early May with the very first requested rate changes out of Virginia, and have been tracking all 50 states as the summer and fall have passed, following every twist and turn of the insane repeal/replace circus in Congress, Trump's bloviating and blathering about "blowing things up" and "letting Obamacare explode", the last-ditch "Graham-Cassidy" sideshow and everything else, right up to and through Trump lowering the boom on cutting off CSR reimbursement payments.

Alabama, Alaska and Wyoming only have a single insurance carrier participating in each of their individual markets. While this is a bad thing from a competitiveness POV, it cetainly makes things easier for me from a tracking-average-rate-hikes POV.

ALSO IMPORTANT: The HHS Dept. is also starting to upload the rate filings to the official RateReview.Healthcare.Gov database, which should make things easier for me going forward (assuming that the data is uploaded properly and isn't messed with, which is a distinct possibility when it comes to the Trump Administration)

Officially, Alabama has the infamous "Freedom Life" phantom plan which is asking for a whopping 71.6% rate hike...to allegedly cover exactly one (1) person statewide. Un-huh.

Aside from that, however, it's Blue Cross Blue Shield across all three states...and they're asking for the following:

As I noted when I crunched the numbers for Texas, it's actually easier to figure out how many people would lose coverage if the ACA is repealed in non-expansion states because you can't rip away healthcare coverage from someone who you never provided it to in the first place.