As I noted Monday morning, I believe that August 1st was the deadline for every state to submit their 2017 rate filings, meaning that the 14 states missing from my Requested Rate Hike Project are finally available to be plugged into the spreadsheet. I'll also be going back through the other states I've been tracking since as early as April to see which ones require updates due to carriers dropping out, joining in or resubmitting their rate requests.

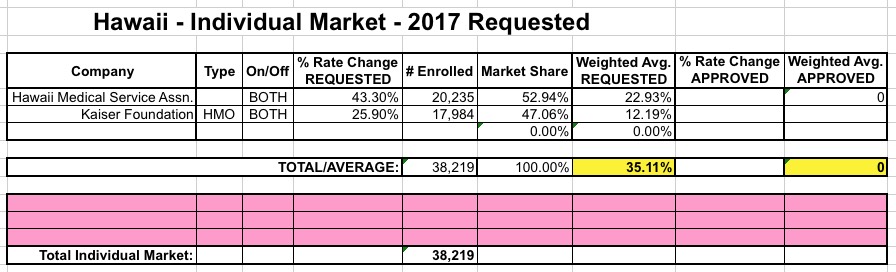

There are only two insurance carriers participating in Hawaii's individual market next year: The Hawaii Medical Service Association (HMSA) and the Kaiser Foundation Health Plan.

As I noted Monday, I believe August 1st was the deadline for every state to submit their 2017 rate filings, meaning that the 14 states missing from my Requested Rate Hike Project are finally available to be plugged into the spreadsheet. I'll also be going back through the other states I've been tracking since as early as April to see which ones require updates due to carriers dropping out, joining in or resubmitting their rate requests.

In 2014, New Jersey's total individual market was estimated at around 261,000 people, including off-exchange, grandfathered and transitional enrollees. Assuming 25% growth, this should be around 325,000 today.

As I noted Monday, I believe August 1st was the deadline for every state to submit their 2017 rate filings, meaning that the 14 states missing from my Requested Rate Hike Project are finally available to be plugged into the spreadsheet. I'll also be going back through the other states I've been tracking since as early as April to see which ones require updates due to carriers dropping out, joining in or resubmitting their rate requests.

The most recent ACA/healthcare news out of Illinois was the ugly announcement that Land of Lincoln Health is the latest ACA-created Co-Op to go belly-up, leaving 49,000 people (39,000 on individual plans and 10,000 in the small group market) having to scramble to find new coverage in the middle of the year. This was on top of recent news that UnitedHealthcare is pulling out of dozens of states including Illinois (Humana is also dropping out of a bunch of states, but I don't think Illinois is among them).

Well, nature (and the market) abhors a vacuum, so guess what?

One of the nation's largest health insurance companies plans to enter the Obamacare marketplace in the Chicago area for the first time, bringing new competition as other insurers exit or go out of business.

Every year, Republicans insist that the ACA is guaranteed to cause a rate hike "death spiral" as increasing premiums cause healthier people to drop out of the individual exchange market, causing higher medical expenses, causing even higher premiums, causing more healthy people to drop out and so forth...and every year, for three years in a row so far, this has failed to be the case nationally. While premiums have obviously continued to increase for many people, the individual insurance market has grown each year, from around 11 million in 2013 to 15.6 million in 2014, around 17 million last year and up to 19-20 million or so today.

IMPORTANT: This is really just a placeholder for Georgia's 2017 average rate hike requests, because it's extremely spotty and partial so far. I'll update it once I'm able to actually track down the bulk of Georgia's individual market enrollment and rate hike request numbers.

UPDATE 7/25/16: I've managed to acquire the additional filings; see update below

California’s health insurance exchange estimates that its Obamacare premiums may rise 8 percent on average next year, which would end two consecutive years of more modest 4 percent increases.

The projected rate increase in California, included in the exchange’s proposed annual budget, comes amid growing nationwide concern about insurers seeking double-digit premium hikes in the health law’s insurance marketplaces.

...Insurers in California have submitted initial rates for 2017, but the final figures won’t be known until July after state officials conduct private negotiations.

LAS VEGAS (AP) — Health insurance costs for about 240,000 Nevadans who buy individual or small-group plans are expected to rise next year, and state officials want consumers to offer feedback before the proposed rates are locked in in coming weeks.

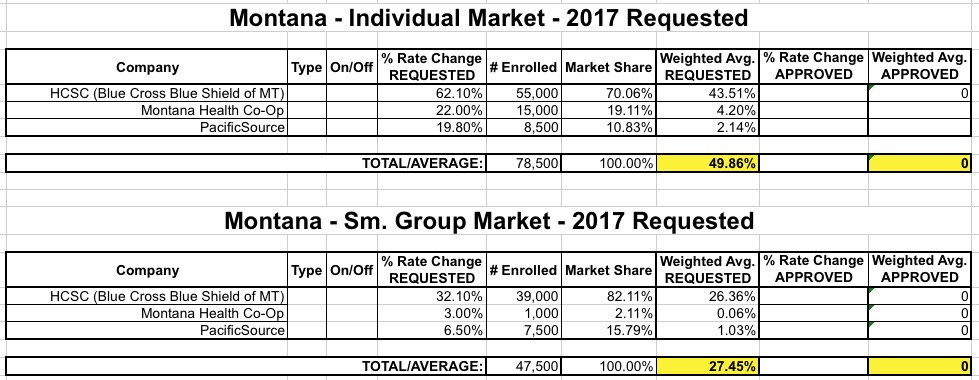

Montana's entire individual market was around 70,000 people back in 2014, and has likely grown to around 87,000 today, so it looks like pretty much everyone is accounted for above (the remaining 9,000 or so are presumably enrolled in grandfathered policies; Montana is among the few red states which didn't allow transitional plans).

As for the actual requested rate hikes...ouch. BCBS is seeking a whopping 62% average increase, and since they own 70% of the individual market, that means a statewide weighted average of right around 50% even. Things aren't as ugly on the small group market, but that 27.5% average is still pretty ugly.

OK, regular readers know that I almost never write directly about Medicare-related issues (unless it's in relation to trying to figure out the total uninsured rate and so forth), and I've only even mentioned Medigap before 3 times in the history of this website. I honestly don't know much about the program except that it's basically supplemental insurance which covers treatment/services not already covered by Medicare.

However, this seems like a significant development for my home state:

Seniors can expect to pay an additional $48 to $177 per month on BCBS Medigap plans.

Nearly 200,000 seniors can expect to pay more for their Medigap supplemental health insurance plans next year -- for some older individuals, more than twice their current amount -- when Blue Cross Blue Shield of Michigan goes forward with a long-awaited rate increase that does away with what the insurer says are below-market rates.

Blue Cross today proposed the new Medigap rates that would take effect on Jan. 1, following a five-year rate freeze for its Legacy Medigap plan.