UPDATE 10/27/16: See below for FINAL update (for real!)

UPDATE 10/19/16: As you can see, I've locked in the approved weighted average rate hikes for 40 states plus DC, leaving 10 states to go. I do plan on filling in the remaining approved rate hikes as the data for those 10 states comes in, but at this point it's quite clear that 25% is the magic number. The weighted average has been hovering between the 23-26% range since the first few approvals started being publicized in mid-August, and has stabilized in the 24-25% range for the past month. Over 77% of the total U.S. population is represented by these 40 states (+DC); unless there's some dramatic final rate changes in the remaining 10 states, that national 25% average isn't likely to budge by more than a rounding error.

As proof of this, I assumed that the requested rate hikes are approved exactly as is for all 10 states.

Result? The national, weighted average rate hikes went from 25.25%...to 25.36%.

OK, make that four states in which at least one major carrier has submitted an updated rate filing request since I originally estimated the statewide average.

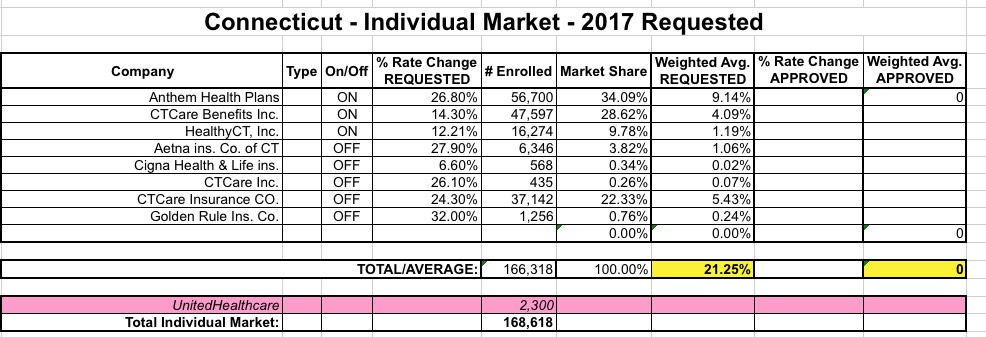

Shortly after that, however, HealthyCT became the latest ACA-created Co-Op to fail, meaning their 16,000 or so current enrollees will have to shop around for new coverage next year. I revised the numbers accordingly and the average request bumped up a bit to 22.2%...

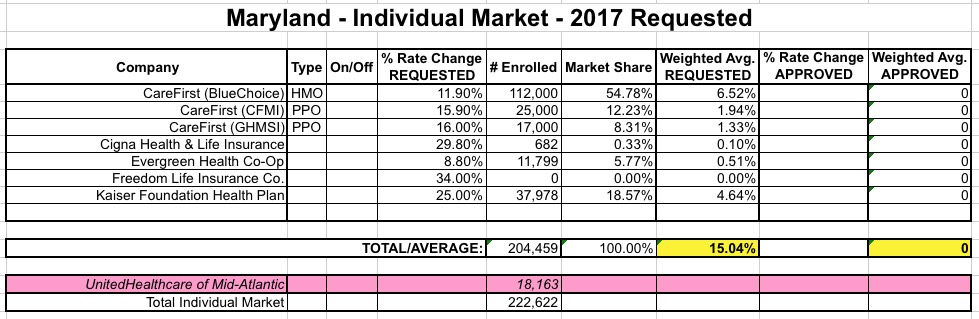

BALTIMORE – Commissioner Al Redmer, Jr. will be conducting a second public hearing on Monday, August 15th from 11 am – 1 pm at the Maryland Insurance Administration located at 200 St. Paul Place, 24th floor Hearing Room, Baltimore, MD 21202 to receive public input on a revised filing made by CareFirst. On July 26, CareFirst refiled its 2017 proposed rates for the individual market and requested a 27.8% rate increase for HMO plans and a 36.6% rate increase for PPO plans. CareFirst previously requested a 12.0% and 15.3% rate increase, respectively.

I noted back in February that Vermont Health Connect, VT's ACA exchange, has remained essentially silent since last fall, issuing only 2 press releases since Open Enrollment started last November (one of which was about a new plan comparison tool, the other of which was about some sort of Medicaid-related dealine). In other words, they haven't publicized their 2016 enrollment numbers whatsoever...the only reason I have data for VT at all is thanks to the official ASPE reports from the HHS Dept. This is a stunning 180º turnaround from 2015, when they were issuing detailed reports on a regular basis.

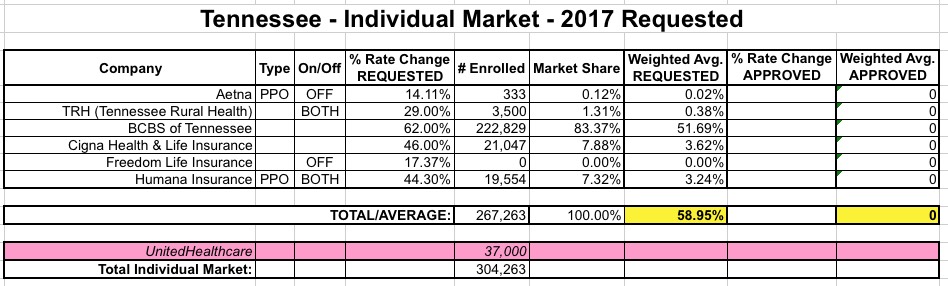

Cigna and Humana would have to revise their requests up to 50% apiece in order for the statewide average to end up hitting the 60% threshold, but that's not exactly a vote of confidence when it's already in the 56% range to begin with.

In its latest filing, Cigna is proposing an average 46 percent increase — double its first 23 percent increase request.

Humana, which requested a 29 percent average increase in June, is requesting an average 44.3 percent increase, according to a filing with the state regulators.

Here's what that looks like on the weighted average table:

Rhode Island, in addition to being one of the smallest states, is also one of the first states I crunched the rate hike numbers for back in late May. It was actually pretty easy to run a weighted average hike request since there are only 2 carriers even operating on the individual market next year: Blue Cross Blue Shield of RI and Neighborhood Health Plan (UnitedHealthcare is dropping out of the RI indy market entirely, but only has about 1,400 people enrolled to begin with).

Anyway, BCBS was asking for a 9% increase, while Neighborhood is among the very few carriers to actually request a rate decrease...of around 5%. As a result, Rhode Island has the honor of having the lowest average rate hike request of all 50 states (+DC) next year...a mere 3.6% overall, which is awesome.

In an effort to prevent more insurers from abandoning the Obamacare exchange in Tennessee, the state's insurance regulator is allowing health insurers refile 2017 rate requests by Aug. 12 after Cigna and Humana said their previously requested premium hikes were too low.

As of last week, five companies in Arizona had announced plans to pull out or pull back: Health Choice, United Healthcare, Humana, Blue Cross Blue Shield of Arizona and Health Net.

Well, there you have it: Across all 50 states (+DC), taking a bunch of caveats into account (see below), as far as I can estimate, the average premium rate increases being requested by health insurance carriers sits at right around 23% overall.

Off-exchange policies are included whenever possible, but only if they're ACA-compliant (grandfathered/transitional plans are in a different risk pool anyway). The ACA-compliant individual market totals roughly 18-19 million people nationally (11 million on-exchange, another 7-8 million off-exchange). Grandfathered/Transitional plans likely total around 2-3 million more.

Only individual market policies are included (there's a few states where the small group market has been merged with the individual market risk-pool wise, but I only include indy enrollees for purposes of weighting). The small group market was around 13.5 million people, according to Mark Farrah Associates.

Some carriers are pulling out of either specific counties or entire states next year, or are dropping certain plans while keeping others. There's no way of estimating the "average rate increase" for anyone who's losing their existing plan altogether.

Well, I've managed to put together estimates (some very rough, some pretty specific) of the weighted average requested ACA-compliant individual market rate hikes for 49 out of 50 states, along with the District of Columbia. This leaves just one state left: Minnesota. For whatever reason, I've been informed that Minnesota's requested rate filings won't be available to the public until September 1st, which is too late for my purposes...because by that point, many of the other states will have started releasing their approved rates for next year (in fact 3 of them--Oregon, New York and Mississippi--have already done so). Minnesota's approved rates will be posted on October 1st. It's always been my intent to lock down the requested rates for every state before the approved numbers are posted in order to run a comparison between what was asked for and what the final approved rate changes are.