TRENTON — As the January 31 final deadline for Open Enrollment approaches, New Jersey residents still in need of health insurance are encouraged to explore plan options for 2026 through Get Covered New Jersey, the State’s Official Health Insurance Marketplace, New Jersey Department of Banking and Insurance Acting Commissioner Susan Ochs said today, reminding residents that financial help and community-based enrollment assistance remains available.

Open Enrollment is the only time of year residents can enroll in a plan, unless they have a major life event, such as marriage, pregnancy, or a move that qualifies them for a Special Enrollment Period.

Marketplace 2026 Open Enrollment Period (OEP) Report: National Snapshot

The Centers for Medicare & Medicaid Services (CMS) reports that 23.0 million consumers have signed up for 2026 individual market health insurance coverage through the Marketplaces since the start of the 2026 Marketplace Open Enrollment Period (OEP) on November 1, 2025.

This includes 15.8 million Marketplace plan selections in the 30 states using the HealthCare.gov platform for the 2026 plan year and 7.2 million plan selections in the 20 states and the District of Columbia with state-based Exchanges (SBEs) that are using their own eligibility and enrollment platforms.[1]

Sen. Bernie Moreno, R-Ohio, made his final pitch to Senate Democrats on a plan to revive expired health care subsidies on Wednesday, according to a copy of the legislation obtained by Semafor.

The Ohio Republican is pitching a one-year extension of the enhanced premium tax credits that expired at the end of last year with an option to use Health Savings Accounts after 2026. it would also bar “individuals not lawfully present” in the US from receiving benefits under the bill.

...The proposal also includes a minimum $5 monthly payment on subsidized plans; extends open enrollment until March 31; imposes penalties on fraud; requires audits of states’ compliance with the Hyde amendment barring taxpayer funding on abortions; includes cost-sharing reduction payments; and caps the subsidies at 700% of the federal poverty level.

Coming out of open enrollment, Health Connector enrollment for 2026 is slightly higher than it was at the end of 2025.

Health Connector individual market enrollment for 2026 is 391,744, a 1.6 percent increase compared to total unique enrollees in November and December 2025

...I'm bringing all of this back up again today because I strongly suspect that the situation is about to reverse itself, with the Trump Administration already preparing to brag about impressive-sounding ACA enrollment numbers for 2026 in spite of the enhanced tax credits expiring less than 60 hours from now...even though the actual negative impact of the expiring tax credits (along with several other administrative policy changes made by CMS this year) likely won't be known for several months after Open Enrollment officially ends in January.

Open enrollment through Washington Healthplanfinder ends, with federal actions and lapsed tax credits creating uncertainty and higher costs

Open enrollment concluded Jan. 15 with a record number of Washingtonians receiving Cascade Care Savings

OLYMPIA, Wash. – More than 290,000 Washingtonians selected a plan for 2026 health and dental insurance through Washington Healthplanfinder during open enrollment. Washington Health Benefit Exchange runs Washington Healthplanfinder, the state’s online marketplace for Affordable Care Act (ACA) health insurance.

Expiring enhanced premium tax credits (ePTCs) increased many people’s monthly costs. Around 40,000 fewer Washingtonians are receiving premium tax credits in 2026 than 2025. Some customers saw significant increases in their health insurance premiums, resulting in more than 61,000 customers changing their plans.

Two things are true as of today: 2026 ACA Open Enrollment has ended...and 2026 ACA Open Enrollment is still going on (in some states).

The official Open Enrollment Period is over in 43 states...but residents of the other 7 (plus DC) still have time to enroll for coverage starting either February 1st or March 1st!

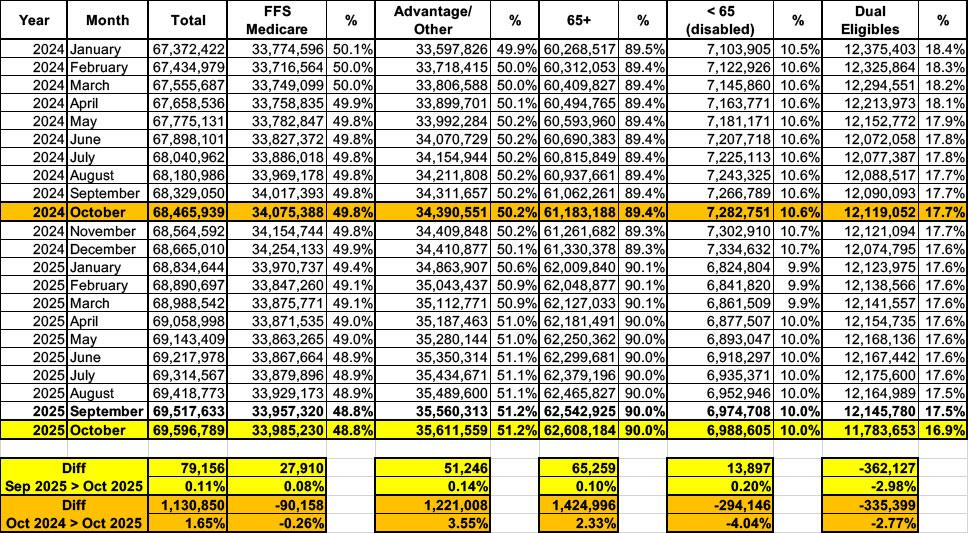

Whether the data posted since January 20, 2025 is accurate or not, I can't say for certain, but at least they're updating it...and so far, at least, I don't see anything in their monthly reports which is setting off any obvious red flags.

In any event, according to the latest report, as of October 2025:

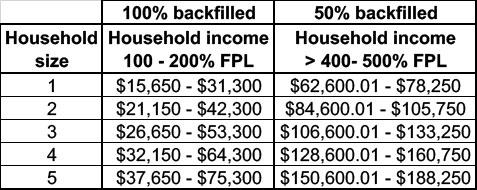

The bottom line is that Connecticut enrollees who earn between 100 - 200% of the Federal Poverty Level (FPL) will have 100% of the lost federal tax credits backfilled, while enrollees who earn between 400 - 500% FPL will have half (50%) of their lost subsidies covered:

The state subsidies are currently in place for one year.

Here is a chart to show the annual income by household size for eligible groups:

{kind=link}

{kind=link}