UPDATE: TexasFoldEm: GOP Sen. Tillis dusts off last year's sham "Protect Act", falsely claims THIS TIME it actually protects people

Thu, 04/11/2019 - 9:42am

The #TexasFoldEm case uses the World's Flimsiest Excuse to try and eliminate the Affordable Care Act's critical health insurance coverage protections for the 130 million Americans who have pre-existing conditions.

In response, Republican Senators Tillis, Alexander, Grassley, Ernst, Murkowski, Cassidy, Wicker, Graham, Heller and Barrasso have introduced a new bill which they claim would ensure pre-existing coverage protections. Unfortunately, it...doesn't.

I've been out and about all day and will also be unable to update the blog all day Saturday, so I'll keep this one short. Besides, several others, including Jeffrey Young of the Huffington Post have already written up good overviews of this garbage:

Right there in the text, it says health insurance companies would not be allowed to deny an individual coverage or charge extra because of “health status, medical condition (including both physical and mental illnesses), claims experience, receipt of health care, medical history, genetic information, evidence of insurability (including conditions arising out of acts of domestic violence), disability, [or] any other health status-related factor determined appropriate by the Secretary [of Health and Human Services].”

But it’s what the bill doesn’t say that makes the above mostly meaningless.

Yes, insurance companies wouldn’t be allowed to refuse to offer coverage to someone who, for example, has a history of cancer or is pregnant. But they could sell someone a policy that doesn’t cover cancer treatments or the birth of a child.

Sure, premiums wouldn’t be allowed to vary based on health status or pre-existing conditions. But prices could dramatically vary based on age, gender, occupation and other factors, including hobbies, in ways that are functionally the same as basing them on medical histories. Insurance companies have a lot of experience figuring out that stuff.

Or, as I put it at the time...

So they’d have to cover people WITH cancer or diabetes, they just wouldn’t have to cover that person’s...cancer or diabetes. That’s...not helpful. https://t.co/rIrvCgcMnF

— Charles Gaba (@charles_gaba) August 24, 2018

Well, with the #TexasFoldEm oral arguments now officially scheduled for the week of July 8th, it looks like North Carolina Senator Thom Tillis has decided to try and save his butt in 2020 by reintroducing largely the same bill, with a twist:

...Like last year's version, the Tillis bill doesn't have the votes to move forward in the Senate. Democrats have dismissed GOP health care efforts, which they view as a way to undermine Obamacare, and it's an open question whether all Republicans in the chamber to support it. Fifteen Senate Republicans co-sponsored a similar Tillis measure in the last Congress. House Democrats, now in control of the chamber, have focused their energy on defending Obamacare or more expansive health care overhauls, making it exceedingly unlikely they'd ever consider the bill.

Tillis first introduced the legislation shortly after the Justice Department announced it would not defend Obamacare's pre-existing protections in the Texas case. The senators marketed that bill as ensuring that those with imperfect health histories would be able to get insurance. It became a talking point for some Republicans on the midterm campaign trail.

However, experts quickly pointed out that the bill would allow insurers to exclude coverage of the pre-existing conditions and to adjust premiums based on gender, which could increase rates for women, especially those of child-bearing age. Obamacare, on the other hand, requires insurers to provide comprehensive policies and bars them from using gender as a factor in rates.

This year's legislation would bar insurers from excluding such coverage, according to The Wall Street Journal, which first reported the new Tillis bill.

Hmmm...well, let's take a look at the new version of the bill, shall we? Oh, wait...we can't. The actual legislative text hasn't been posted online yet.

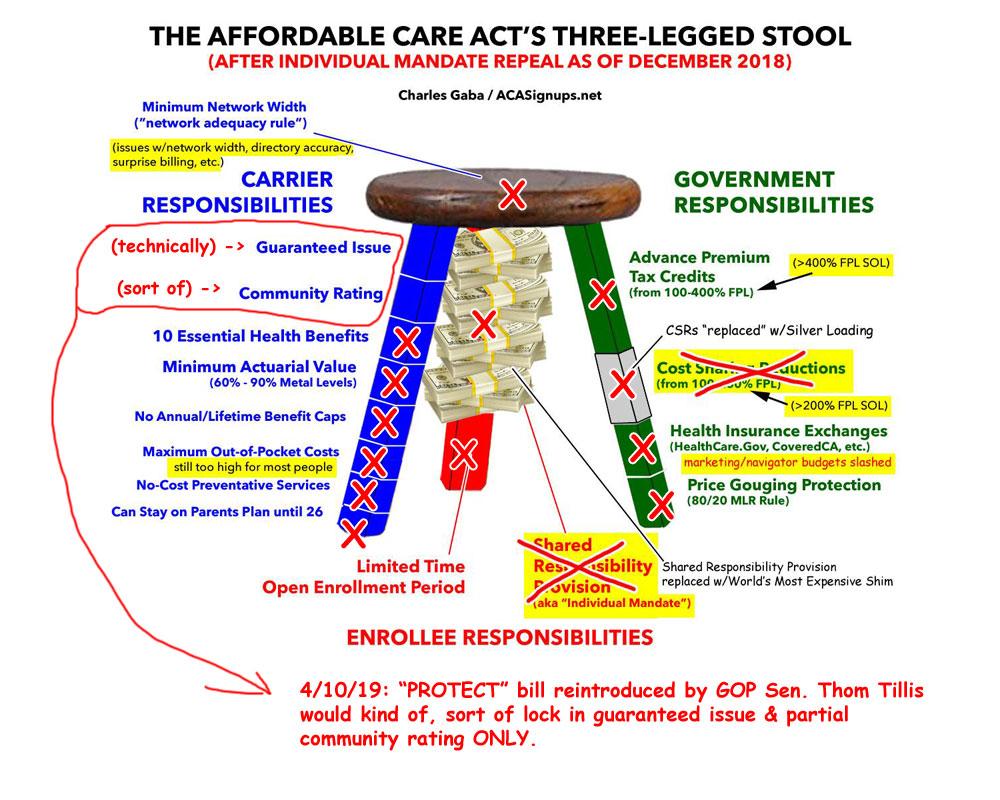

The revised version supposedly checks off the Community Rating and Essential Health Benefits parts of the Three-Legged Stool's Blue Leg, but until I see the text let's just say I'm more than a little suspicious. Even if that's the case, it would still be missing the rest of the blue leg (miniumum actuarial value, prohibition on annual/lifetime claims caps, limit on out-of-pocket expenses and so on).

Color me more than a little skeptical.

UPDATE: Welp. So much for that:

The new Republican bill would prohibit insurers from denying coverage to people with pre-existing conditions, charging them higher premiums, or excluding services related to the condition. A previous version would have allowed pre-existing condition exclusions.

— Larry Levitt (@larry_levitt) April 11, 2019

Unlike the ACA, the new Republican pre-existing condition bill would not disallow lifetime or annual limits, cap patient out-of-pocket costs, require coverage of essential benefits, prohibit gender rating, or provide subsidies to make premiums more affordable.

— Larry Levitt (@larry_levitt) April 11, 2019

In other words...not much has changed. Also, this cute trick:

The ACA specifies circumstances when premiums CAN vary (location, age, tobacco) so other rating (e.g. based on gender) is inherently prohibited

The new GOP bill takes the opposite approach: It specifies circumstances when premiums CAN'T vary, giving insurers much more flexibility https://t.co/G0IZllSWS9— Cynthia Cox (@cynthiaccox) April 11, 2019

In other words, as Jeffrey Young noted last summer:

But prices could dramatically vary based on age, gender, occupation and other factors, including hobbies, in ways that are functionally the same as basing them on medical histories. Insurance companies have a lot of experience figuring out that stuff.

Hard Pass. Next?

Advertisement