IMPORTANT: Guess what's NOT included in Graham-Cassidy??

Tue, 09/19/2017 - 12:47am

Regular readers know that one of the issues I've spent the better part of the past year yammering on about endlessly is the importance of Congress formally appropriating Cost Sharing Reduction reimbursement payments to the insurance carriers on the individual market exchanges.

Thanks to the ongoing/pending ruling in the federal House vs. Burwell Price lawsuit, Donald Trump has the ability to pull the plug on CSR payments pretty much whenever he wants to (and he's threatened to cut them off every month since around March or April so far). CSR payments hang like a Sword of Damocles over the heads of every exchange-based insurance carrier each month, with them never knowing whether they'll get reimbursed or not.

As bad as the CSR situation is for the remainder of this year, when it comes to 2018, it's an even bigger problem. The carriers are already stuck with their current contracts through the end of December, so for 2017, all they can do is grit their teeth every month, crossing their fingers and breathing a big sigh of relief when the Trump Administration deigns to actually make the reimbursement payments that are legally owed to them. Between Trump's long history of stiffing contractors he owes money to and his repeated Twitter rants in which he's openly threatened to cut off CSR "bailouts" (they aren't bailouts, but he doesn't know the difference anyway), the carriers are no doubt gulping down Pepto-BIsmol around the 23rd of each month (that's when the CSR payments are due).

For next year, however, the carriers have declared en masse that they have no intention of being hung out to dry on this issue. Some, like Humana, Aetna, Wellmark, Optima and so on, have already either announced that they're dropping out of the individual market altogether, or at least moving to the off-exchange market only, in a number of counties and/or states, specifically citing CSR payment uncertainty as one of the primary reasons for their decision.

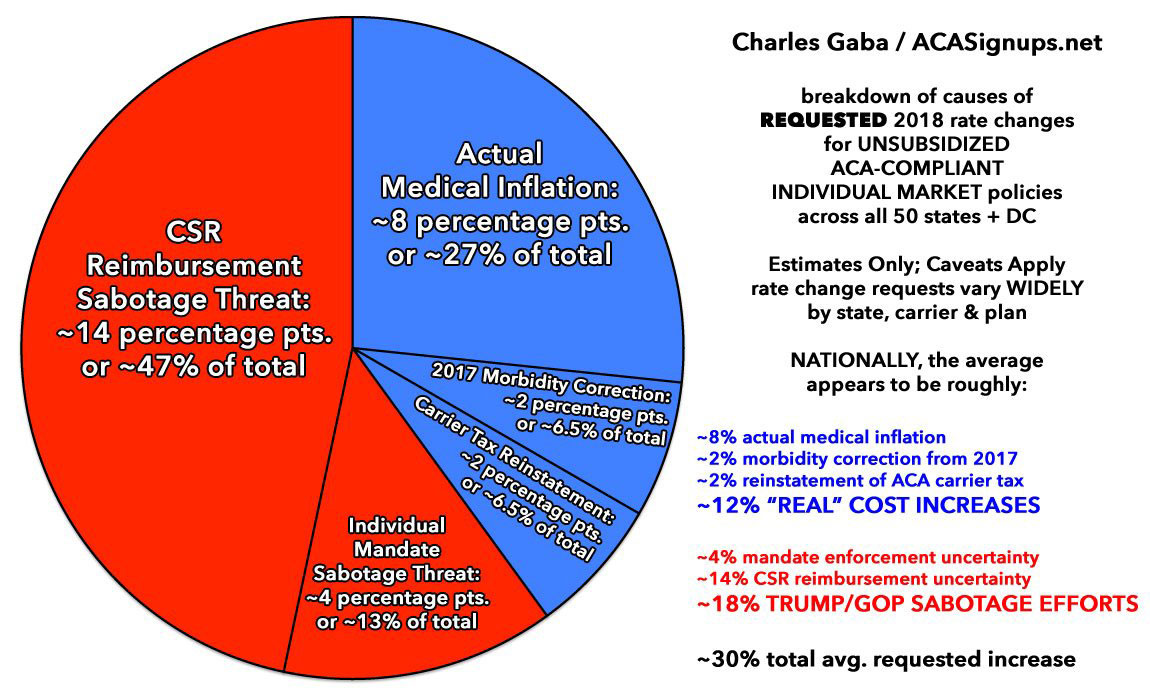

The rest of the carriers who are sticking around are going a different route: They're jacking up their rates dramatically to cover their asses in the event CSR payments aren't made next year. tacking on an average additional charge of around 14 percentage points overall specifically to cover their potential CSR losses.

Anyway, as I've noted before, one of the great ironies of the Republican repeal effort is that both the House GOP version (AHCA) and the Senate GOP version (BCRAP) included specific appropriation of CSR funds for the next two years at the very end of each bill:

House Version (AHCA), page 142 (last page):

SEC. 207. FUNDING FOR COST-SHARING PAYMENTS.

There is appropriated to the Secretary of Health and Human Services, out of any money in the Treasury not otherwise appropriated, such sums as may be necessary for payments for cost-sharing reductions authorized by the Patient Protection and Affordable Care Act (including adjustments to any prior obligations for such payments) for the period beginning on the date of enactment of this Act and ending on December 31, 2019. Notwithstanding any 10 other provision of this Act, payments and other actions for adjustments to any obligations incurred for plan years 2018 and 2019 may be made through December 31, 2020.

SEC. 208. REPEAL OF COST-SHARING SUBSIDY PROGRAM.

(a) IN GENERAL.—Section 1402 of the Patient Protection and Affordable Care Act is repealed.

(b) EFFECTIVE DATE.—The repeal made by subsection (a) shall apply to cost-sharing reductions (and payments to issuers for such reductions) for plan years beginning after December 31, 2019.

Senate Version (BCRAp), page 163:

SEC. 210. FUNDING FOR COST-SHARING PAYMENTS.

There is appropriated to the Secretary of Health and Human Services, out of any money in the Treasury not otherwise appropriated, such sums as may be necessary for payments for cost-sharing reductions authorized by the Patient Protection and Affordable Care Act (including adjustments to any prior obligations for such payments) for the period beginning on the date of enactment of this Act and ending on December 31, 2019. Notwithstanding any other provision of this Act, payments and other actions for adjustments to any obligations incurred for plan years 2018 and 2019 may be made through December 31, 2020.

SEC. 211. REPEAL OF COST-SHARING SUBSIDY PROGRAM.

(a) IN GENERAL.—Section 1402 of the Patient Protection and Affordable Care Act is repealed.

(b) EFFECTIVE DATE.—The repeal made by subsection (a) shall apply to cost-sharing reductions (and payments to issuers for such reductions) for plan years beginning after December 31, 2019.

Of course, in both cases, the CSR payments only last two years...before the entire CSR program is wiped out altogether.

The reason for this is simple: The GOP is trying to avoid taking the blame for massive rate hikes until after the 2018 midterms are over. That's why so much of both the AHCA, BCRAP and Graham-Cassidy doesn't actually start until the end of 2019.

Even as I've been sounding the alarm about the danger posed by Graham-Cassidy over the past week, however, I didn't really give much thought to how G-C deals with CSRs. If I thought about it at all, I assumed that they had simply done the same thing a third time: Copy & paste the text above again and be done with it: Appropriate it for two years, then kill it off.

However...it turns out that's not the case at all. Here's the formal legislative text of the most recent version of the Graham-Cassidy bill. Scroll all the way to the very end and you'll only see the second part of the above, like so:

19 SEC. 205. REPEAL OF COST-SHARING SUBSIDY PROGRAM.

(a) IN GENERAL.—Section 1402 of the Patient Protection and Affordable Care Act is repealed.

(b) EFFECTIVE DATE.—The repeal made by subsection (a) shall apply to cost-sharing reductions (and payments to issuers for such reductions) for plan years beginning after December 31, 2019.

Yes, Graham-Cassidy uses the exact same language to terminate the CSR program effective 12/31/19...but unlike AHCA and BCRAP, it does not actually appropriate CSR reimbursement payments before then.

This means that unless the Senate HELP committee is able to pull a rabbit out of their hat and appropriate CSRs separately or the GOP slips the earlier half of the text back into Graham-Cassidy before voting on it, CSR payments will NOT be guaranteed for 2018.

So, was it an oversight or a deliberate decision not to inlcude the 2-year appropration language? I can't imagine that it was an oversight, since a) it's the very last page of the bill and b) they did include the second paragraph but not the first, after simply copy/pasting it for AHCA and BCRAP earlier this year. I'm certain this was a deliberate decision on Lindsey Graham and Bill Cassidy's part.

WHY would they leave that out? The only reason I can think of is that they think this will help win over reluctant Libertarian types like Rand Paul, who hates the thought of any government spending on helping people out. Sure, he's already acting like he's a "no" vote anyway, but it's possible that formally locking in CSR payments for two years would guarantee a "no" from him (then again, he voted yes on BCRAP after protesting, so perhaps not).

UPDATE: D'OH!! Thanks to David Anderson for reminding me of the obvious reason why CSR funding was left out of Graham-Cassidy: It was already ruled not kosher by the Senate Parlimentarian back in July. CSR appropriation can't be included in a reconciliation bill because they're already included in the ACA to begin with (which is ironic given that the only reason CSRs are at risk in the first place is because the House GOP claimed that they aren't properly appropriated in the ACA).

More to the point, however: What other significance does not including CSR funding have?

Well, first of all, is it possible that they'll slip CSRs in before the vote? I suppose so, but consider this:

- The final deadline for the insurance carriers to actually sign their contracts for 2018 is Sept. 27th, just 8 days from now.

- The end of the 2017 fiscal year (i.e., the deadline for the GOP to try and cram through Graham-Cassidy with only 50 Senate votes) is Sept. 30th.

- The CBO is "aiming" to provide a "preliminary assessment" of Graham-Cassidy "early next week" which I presume means Monday the 25th or Tuesday the 26th.

- I assume the other steps (parlimentary ruling, vote-a-rama, etc) would take place on Wednesday the 27th, the same day the contracts have to be signed.

- Yom Kippur is the evening of the 29th, running through Saturday the 30th. I can't imagine even McConnell would be that much of a dick to schedule the vote then.

- That leaves Thursday the 28th or Friday the 29th for the actual vote itself.

That's a day or two after the carrier contracts have been signed.

That means that even if there's a last minute change to the bill, at this point, CSR payments are virtually certain not be guaranteed next year.

If I've figured this out, I'm sure the insurance carriers have as well...which explains why, for instance, Health Alliance Plan here in Michigan just dropped out on Friday.

I wouldn't be at all surprised to see more 11th-hour drop-outs next week. Donald Trump and the Republican Party's open sabotage of the ACA will likely bear even more fruit.

Here's the irony: In this scenario, given the timing of it all, you could see:

- Carriers dropping out due to CSRs not being paid...because the CSR appropriation came after they dropped out

- Carriers jacking up their rates an extra 14 points due to CSRs not being paid...because the CSR appropriation came after their rates were locked in.

Congratulations, GOP: You managed to raise premiums 14 points and decimate the market and dole out a good $10 billion designed to avoid both of those outcomes all at once.

Bravo.

UPDATE: Welp. So much for that:

@Lawrence Breaking News: McConnell has cancelled hearings on Lamar Alexander/Patty to force Senators to vote on #GrahamCassidyBill

— Alex (@aroseblush) September 19, 2017

Yup. The final approved rate hikes might be a bit lower overall, but generally speaking, it looks like Mitch McConnell has just guaranteed an extra 14 point rate average hike next year.

Advertisement