So aside from the potential King v. Burwell fallout, what else did CMS reveal today?

Tue, 06/02/2015 - 3:26pm

NOTE: LIVE UPDATING, CHECK BACK OFTEN!!

OK, now that I've posted about CMS's actual "effectuated enrollment snapshot" and posted the most important/relevant piece of data from their report (confirmation that 6.4 million people will lose their tax credits if the King v. Burwell plaintiffs win later this month), now I can take a look at the other important data included in the report.

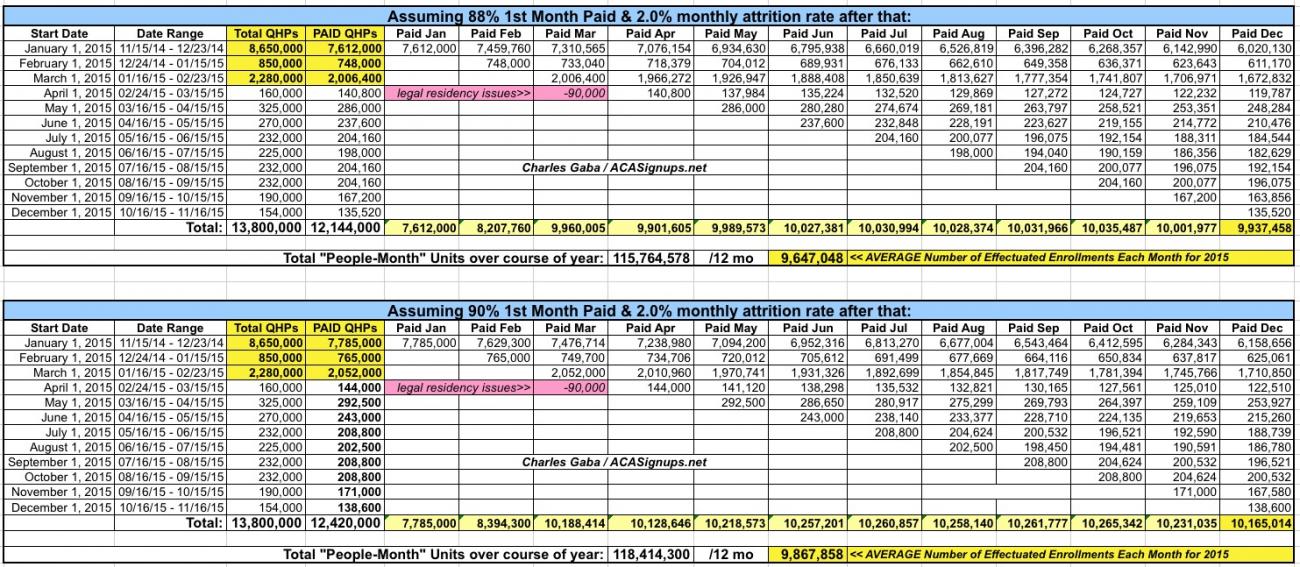

It's important to remember that this report only runs through March 31st, 2015. Some of the enrollment numbers (and thus, number of effectuated enrollments, percent receiving tax credits and so on) will have changed slightly since then as additional people enroll and existing enrollees drop their plans (I expect the effectuated enrollments to be around 2% higher throughout the summer and fall before dropping off again...assuming no King v. Burwell fallout, that is). Overall, however, this should be a pretty accurate assessment of where things stand as of today.

With all that in mind, here we go:

March 31, 2015 Effectuated Enrollment Snapshot

About 11.7 million Americans selected plans through the Health Insurance Marketplaces as of February 22, the end of the “in-line” special enrollment period for 2015 Open Enrollment for individual market coverage. On March 31, 2015, about 10.2 million consumers had “effectuated” coverage which means those individuals paid for Marketplace coverage and still have an active policy in the applicable month.1 These numbers are consistent with HHS’s effectuated target for the end of 2015. About 6.3 million consumers were enrolled in health coverage through the Marketplaces and had paid their premiums on December 31, 2014.

How does this compare with my own estimates?

Well, I estimated effectuated enrollments as of the end of March being somewhere between 9.9 - 10.1 million (call it 10.0M even). The actual number was 10,187,197 million, so I undershot by about 1.9%.

{kind=link}

On the other hand, I had December 2014 effectuated enrollments pegged at around 6.6 million, when in fact it had dropped to 6.3 million. However, 290,000 of that difference may have been people who either a) did automatically renew their policies but immediately cancelled or b) were dropped involuntarily by HHS due to legal residency issues. Either way, I overshot by about 4.8%.

{kind=link}

Of the approximately 10.2 million consumers with effectuated Marketplace enrollments nationwide at the end of March 2015, 85 percent, or nearly 8.7 million consumers, were receiving an advanced premium tax credit to make their premiums more affordable throughout the year. The average advanced premium tax credit for those enrollees who qualified for the financial assistance was $272 per month.2

The percentage is slightly lower than the 87% originally expected to receive APTCs, presumably because the vast majority of those who didn't pay their premiums at all would have received the credits. However, the actual dollar amount involved is $9 higher than the $263 estimated earlier this year. None of that came from me, however, so I take neither credit nor blame for the differences.

There were 7.5 million consumers with effectuated enrollments for March of 2015 through the 37 Federally-Facilitated Marketplaces (including State Partnership Marketplaces) or supported State-based Marketplaces (collectively known as HealthCare.gov states) and 2.7 million through the remaining State-based Marketplaces.3 Effectuated enrollment for the 34 states that are part of the Federally-facilitated Marketplaces on March 31, 2015 was 7.3 million and for State-based Marketplaces, including New Mexico, Nevada, and Oregon who are State-based Marketplaces using the HealthCare.gov platform, effectuated enrollment was 2.9 million.

It's important to remember not to include New Mexico, Nevada or Oregon when talking about King v. Burwell fallout. They are included in the HC.gov numbers but aren't expected to be victims of the King case if the plaintiffs win.

“The Health Insurance Marketplaces are working,” said HHS Secretary Sylvia Burwell. “Thanks to the Affordable Care Act, millions of Americans now rely on the health and financial security that comes from affordable coverage through the Marketplaces. We’ve seen a historic reduction in the uninsured and consumers are finding the coverage they need at a price they can afford.”

This enrollment snapshot covers effectuated enrollment on March 31, 2015. In 2015, CMS plans to release Marketplace state-by-state effectuated enrollment snapshots on a quarterly basis detailing how many consumers have an effectuated enrollment, how many are receiving advanced premium tax credits and/or a cost-sharing reduction and enrollment by qualified health plan metal level. Today’s snapshot provides an update on the number of individuals with citizenship, immigration status, or household income data matching issues; this information will be released periodically as has been done in the past.

I can live with this. I'd obviously prefer it if they issued these reports weekly or at least monthly, even during the off-season, but quarterly is still better than not releasing the data at all. On the other hand, it'd be nice if they could do so with less lag time after the end of the quarter (It took 2 full months to compile this? Really? I'm not being snarky here...it very well may have, I'm just curious).

This also suggests that they'll release another "mother lode" report sometime around the end of August, although again, an adverse King v. Burwell decision would likely change that game plan dramatically.

The Marketplace effectuated enrollment snapshot provides point-in-time estimates. CMS expects enrollment numbers will change over time when consumers find other coverage or experience changes in life circumstances such as employment status or marriage, which may cause consumers to change, newly enroll in, or cancel their plans. Supporting these types of changes is an important function of the Health Insurance Marketplace.

Yup, as I noted above, about 7,500 people are still enrolling in QHPs each day even during the off season...but a similar number are dropping their policies (or switching from one to another) for similar reasons, which will move the various numbers up and down here and there in each state.

Today’s snapshot also provides a more detailed look at effectuated enrollment in December 2014, including state-by-state breakdowns of how many consumers received financial assistance through advanced premium tax credits and/or cost-sharing reductions as well as the number of consumers who were enrolled in catastrophic, bronze, silver, gold or platinum health plans as of December 31, 2014. This snapshot also includes an update on information for 2014 on citizenship, immigration status or household income data matching issues.

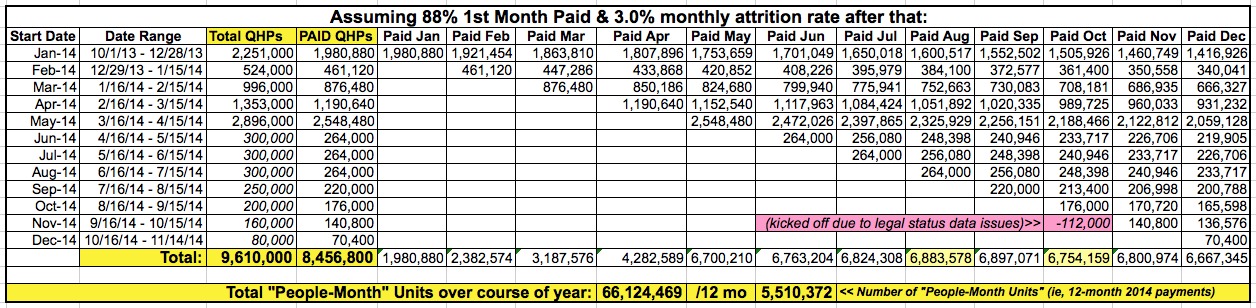

Very nice for "deep dive data geeks". I already noted the 6.3 million vs. 6.6 million difference between the actual EOY number and my own estimate above.

The following tables are included in the March 2015 Marketplace Effectuated Enrollment Snapshot:

Table 1: March, 2015 Total Effectuated Enrollment and Financial Assistance by State

Table 2: March, 2015 Average Advanced Premium Tax Credit by State

Table 3: March, 2015 Total Effectuated Enrollment Data by Metal Level by State

Table 4: December, 2014 Total Effectuated Enrollment and Financial Assistance by State

Table 5: December, 2014 Average Advanced Premium Tax Credit by State

Table 6: December, 2014 Total Effectuated Enrollment Data by Metal Level by State

Actually reposting all 6 tables here would eat up a ton of space, but here's the originals.

March 2015: Total Enrollment and Financial Assistance

Of the approximately 10.2 million consumers who had effectuated Marketplace enrollments at the end of March 2015, 85 percent or about 8.7 million consumers were receiving an advanced premium tax credit to make their premiums more affordable.4 In addition, 57 percent or about 5.9 million consumers were receiving cost-sharing reductions to lower the amount they pay out-of-pocket for deductibles, coinsurance, and copayments. This financial assistance generally is available if a consumer’s household income is between 100 percent and 250 percent of the federal poverty level, the consumer is otherwise eligible for advance payments of the tax credit, and the individual chooses a health plan from the silver plan category.

I admit that of all the different facets of the ACA, enrollments and so on, I haven't paid a whole lot of attention to the CSR (Cost Sharing Reduction) issue, but that's a big deal as well. Andrew Sprung at Xpostfactoid is the guy to read about all CSR issues. Suffice it to say, if the King case results in tax credits being killed for 6.4 million people, about 4.5 million of them would also lose the Cost Sharing Reduction assistance. Of course, they'd almost all end up losing their policies anyway, so that's kind of a moot point.

The ten states with the highest rate of consumers who received financial assistance through advanced premium tax credits were: Mississippi (94.5%), Florida (93.5%), North Carolina (93.2%), Wyoming (92.9%), Louisiana (92.0%), Arkansas (91.1%), Georgia (91.1%), Alabama (90.7%), Wisconsin (90.7%), Alaska (90.5%) and South Carolina (90.2%).

Gee, imagine that! All 10 of them just happen to be Republican-controlled states (OK, Alaska's Governor is an Independent), and all 10 of them just happen to be run through the federal ACA exchange.

The states with the lowest rate of consumers who received advanced premium tax credits include: District of Columbia (10.0%), Minnesota (49.5%), Colorado (55.3%), Hawaii (59.3%), Vermont (64.3%), New Hampshire (65.8%), Massachusetts (66.7%), Utah (67.3%), Maryland (68.2%) and Kentucky (69.3%).

Gee, imagine that! 8 of the 10 just happen to be states which have their own ACA exchange established! (Utah technically has "half" an exchange, in the form of their SHOP exchange, but that doesn't mean much when it comes to the individual market).

Nine of the ten states with the highest rate of consumers receiving financial assistance (all but Arkansas) have not taken the Medicaid expansion option under the Affordable Care Act. As such, those residents with income from 100 to 133 percent of the federal poverty level who are otherwise eligible qualify for coverage through the Marketplace with tax credits.

Gee, imagine that! Oh...wait, CMS already did the snark for me here.

There's still a LOT of other info to dig through in this report; I'll have to save the rest for yet another post this evening or tomorrow.

Advertisement