Idaho is one of only 2 state-based exchanges which stuck with the "official" December 15th deadline for the 2018 Open Enrollment Period (the other was Vermont). Unfortunately, they haven't released an official, detailed demographic breakout report yet, but they did discuss some relevant stats in their December board meeting...which, as it happens, took place on December 15th, which means it's still missing a bit of final data. For now this is the best I can do:

d) Enrollment Update

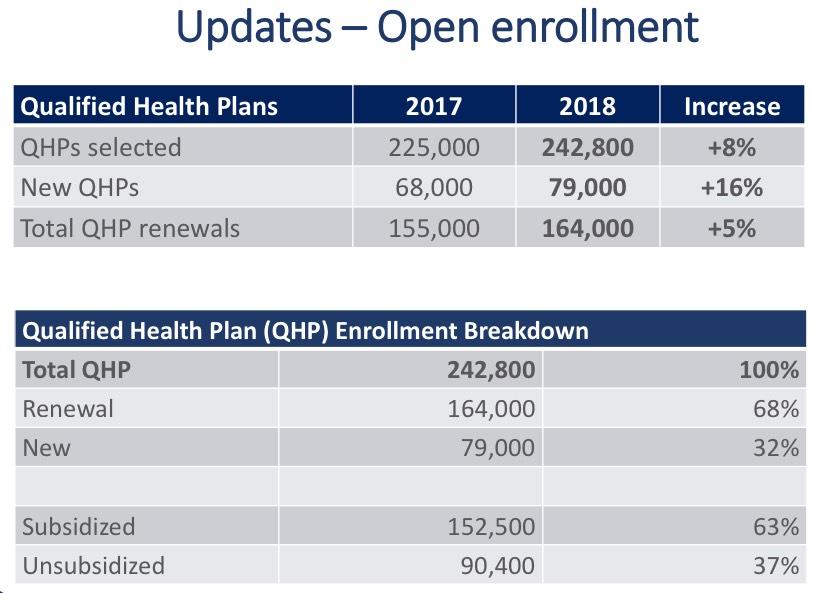

Mr. Kelly said YHI’s goal in enrollments is to be flat year-over-year, and it is within reach. When we look at average enrollments for 2017 of around 90,000 Idahoan’s, we appear to be ahead of that for 2018. As of this morning, we have almost 96,000 enrollments. This week alone, we have gained over 6,000 enrollments, way ahead of our growth for the same time last year. We also had well over 2,100 calls into the support center yesterday.

At this point, the only significant top-line 2018 Open Enrollment numbers missing are the final 10 days out of California (which could add perhaps 40,000 to the total) and a solid month of enrollment from the District of Columbia (23 days, actually, but they extended their deadline by 5 extra days, which may or may not be included in the final, official report from CMS). DC's tally through 1/08 was 21,352 QHP selections. Their all-time high was around 22,700 set in 2016, so I can't imagine that they added more than perhaps 2,000 more since 1/08. In other words, about 99.5% of the 2018 OEP QHP selections have likely been accounted for.

That means it's time to move on to...breaking down the demographic data! Woo-hoo! Parrrr-tyyyy!!

The big, official CMS report from the Assistant Secretary for Planning and Evaluation (ASPE) presumably won't be released for a couple of weeks, but some of the state-based exchanges are faster about posting their demographics. First up: Connecticut!

This Just In, courtesy of Dan Goldberg of Politico New York...

.@charles_gabaNY releases final numbers --253,102 in QHP with 41% receiving NO financial assistance. (That's amazing!) 738,851 in Essential Plan 374,577 in Child Health Plus

Nothing new or noteworthy here, but I've posted the "last call" press releases for California and DC, so I figured with just 8 hours left to go I should do so for New York as well:

ALBANY, N.Y. (January 24, 2018) – NY State of Health, the state’s official health plan Marketplace today announced that New Yorkers who have not yet signed up for coverage in a Qualified Health Plan (QHP) should enroll now so they are covered for 2018. Open Enrollment ends January 31st. Consumers across the state have a choice of multiple health plan options and for many, coverage is more affordable than last year.

Enrollment through NY State of Health continues to climb to record levels with more than 4.2 million enrolled across all programs. As of January 16, 2018, 243,600 consumers have enrolled in a Qualified Health Plan (QHP) and 726,300 have signed up for the Essential Plan, exceeding numbers at the end of open enrollment in 2017.

Final Day of Open Enrollment! Covered California Will Help Consumers Who Get Caught Up in Surge of Last-Minute Shoppers

Covered California’s open-enrollment period ends at midnight tonight.

Due to an expected increase in demand today, consumers who start an application before midnight will be able to work with a certified enroller to complete the process on Thursday or Friday.

Covered California Service Center representatives are available to help through midnight on the 31st and through 8 p.m. on Feb. 1 and 2.

SACRAMENTO, Calif. — On the final day of open enrollment, with tens of thousands of people expected to sign up for health coverage, Covered California announced it would help consumers “cross the finish line” if they get caught up in the surge of last-minute shoppers.

Huh. Deadline extensions were fairly common in the first couple of years of Open Enrollment, but have mostly been phased out more recently. This is a bit unexpected from the DC Health Link:

.@MayorBowser has extended the deadline for individuals & families to enroll in quality affordable health insurance to Monday, February 5th at 11:59 pm. Take advantage of today's extended hours at enrollment centers across the city. Don't delay #GetCoveredDCpic.twitter.com/8R7zq0EzA1

If you've been following this site for awhile, you know that for the 2018 Open Enrollment Period, I sort of partnered up with two grassroots healthcare advocacy groups: ACA Consumer Advocacy and the Indivisible ACA Signup Project. We created and disseminated a whole mess of blue-themed Open Enrollment infographics, in both English and Spanish, for all 50 states and the District of Columbia via our websites, social media and even in print via downloadable PDF versions distributed across various public locations.

Anyway, with Open Enrollment officially wrapping up in the final 3 states (well, 2 states + DC) on Wednesday, Jan. 31st, they shared a few metrics, which I'm proud to repost here as well:

Thread: So, about those blue images. We partnered with @2018ACASignup to try to help offset #ACASabotage around enrollment. Kinda impressed with how the whole thing worked. Here are some numbers:

A huge shout-out to Ken Kelly for calling my attention to this press release which was apparently sent out way back on December 19th???

Vermont wraps up 2018 open enrollment for Vermont Health Connect

News Release — Department of Vermont Health Access Dec. 19, 2017

Vermonters who Didn’t Complete Plan Selection Urged to Call this Week

WATERBURY, VT – State officials reported that nearly 23,000 Vermonters had confirmed a 2018 health plan and qualified for financial help to make the plan more affordable. Total enrollment in qualified health plans, which typically includes 46,000 small business employees and 11,000 individuals who don’t qualify for financial help, is expected to surpass 80,000. While enrollment will be similar to past years, this year’s earlier deadline means fewer members will experience gaps in coverage. In past years, nearly 2,000 members missed out on January coverage.