Just now, the MD Health Connection posted an update through this week:

Incoming exec director Michele Eberle of @MarylandConnect urges Marylanders to enroll in health coverage with 10 days left. New enrollments up 14% this year. Mobile app visitors up 140% Overall enrollment up 4% Keep it going! pic.twitter.com/75g2qu5PbC

I'm assuming these stats are as of December 4th. Last year MD's official QHP selection tally as of December 3rd was around 129,000; if they're 4% ahead of that as of the same date, that means they should have a little over 134,000 to date this year.

Total Enrollments (active renewal, passive renewal, new): 130,556 (up 3% vs. last year)

Active Enrollments (renewals + new): 29,478 (up 98% over last year)

New Enrollments: 10,900 (up 10% over last year)

Applications: 275,790 (up 13% over last year)

Mobile App Visitors: 74,744 (up 110% over last year)

OK, the MD exchange breaks out their numbers slightly differently than I do, but they've provided the numbers necessary to reformat. Like a few other states, they're "front-loading" their auto-renewals, giving the following:

18,578 Active Renewals

101,078 Auto-Renewals

10,900 NEW Enrollees

130,556 TOTAL Enrollments

For clarification: When the MD exchange says that 130,556 is "3% higher than last year", they're talking about at this point in time. Subtract 3% and you get roughly 126.7K as of 11/17/16. Maryland's total enrollment by the end of the 2017 Open Enrollment Period was 157,832.

...Statewide, in fact, growth is up 100 percent since last year, according to Betsy Plunkett, a deputy director for the Maryland Health Benefit Exchange. First-time enrollment is up 15 percent, with changes to existing plans up 270 percent. Overall, 10,420 people enrolled in the first week compared to 5,212 in 2016, she said.

"We realize it's a shorter period so we have to get people in the door quicker," said Andrew Ratner, chief marketing officer for Maryland Health Benefit Exchange, which runs the marketplace.

Sign-ups have been brisk so far, with more than 5,000 people picking plans in the first two days, nearly twice as many as last year. The Maryland Health Connection website, which usually closes at 11 p.m., had to stay open an hour later on Wednesday because 300 people were still online. Maryland currently has about 120,000 Obamacare enrollees.

Believe it or not, the original core focus of ACASignups.net was...wait for it...to track how many people are Signing Up for the ACA. Hard to believe, I realize.

Enrollments in health insurance through the state’s health exchange was robust on the first day of open enrollment Wednesday, with more people signing up for insurance than last year, officials said Thursday.

Advocates and others had expressed concern that consumers would be confused by political wrangling and policy changes to the Affordable Care Act from the administration of Pres. Donald Trump that led to last-minute rate increases and a severe decrease in marketing dollars for the program.

But exchange officials reported that enrollments under the law, known as Obamacare, were up 70 percent to more than 1,800 compared with 1,055 on the first day a year ago. About 150,000 people signed up for private insurance on the exchange in the state last year and more enrolled directly through insurers.

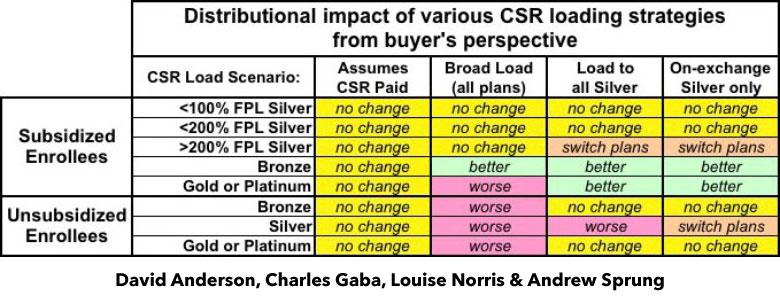

Up until a week ago, the possibility of Donald Trump pulling the plug on Cost Sharing Reduction reimbursement payments was a looming threat every day. While it hadn't actually happened yet, most of the state insurance commissioners and/or insurance carriers themselves saw the potential writing on the wall and priced their 2018 premiums accordingly (or at the very least prepared two different sets of rate filings to cover either contingency).

A few spread the extra CSR load across all policies, both on and off the exchange. This seems like the "fairest" way of handling things on the surface, but is actually the worst way to do so, because it hurts all unsubsidized enrollees no matter what they choose for 2018 and can even make things slightly worse for some subsidized enrollees in Gold or Platinum plans.

MarylandHealthConnection.gov has already been loaded with plans and prices for 2018, one month before open enrollment begins. The upcoming open enrollment period will run November 1 - December 15. Health coverage will start on January 1, 2018.

How do I get an estimate for 2018 health insurance plans?

You can compare plans and prices through a desktop computer browser or by downloading our mobile app, Enroll MHC, on your iPhone or Android.

Click on “Get Started”- this will take you to the application portal. Next, click “Get an Estimate” on the application site. Finally, enter basic information like your county, age and income to see what coverage and financial help you may qualify for. If you choose to get an estimate, the site will take you through a scenario of what plans and pricing you could receive for 2018. You won’t actually be applying for coverage.

When I last checked in on Maryland's individual market rate hikes for next year, the picture was pretty grim: Overall requested increases of around 46%...and that assumed that CSR reimbursements are made in 2018. If you assume CSRs aren't paid, it looked even worse: A whopping 57% average increase statewide for unsubsidized enrollees. Ouch.

As noted the other day, now that I've compiled the initial 2018 rate filing requests for 46 states + DC (the remaining 4 states aren't public yet), it's time to go back to the earlier states I analyzed and see whether there's been any updates/corrections to my original estimates. I started running the numbers back in early May, and a lot has changed since then, with carriers dropping out of the exchanges, expanding to fill the gaps or simply refiling with revised pricing requests.