Including Georgia, I've now compiled initial 2018 unsubsidized individual market rate hike requests for 17 states...and Georgia's carriers are asking for by far the highest overall average increase, even assuming no Trump/GOP sabotage tax.

There appear to be four carriers which have filed to sell individual market plans in Georgia next year: Alliant, Ambetter (aka Celtic, aka Centene...for God's sake, pick one name, guys, willya??), Anthem Blue Cross Blue Shield and Kaiser Health Plan.

New data have been released contradicting Republican propaganda about the “failing” Affordable Care Act. What may be more embarrassing to the hardliners pushing repeal is that it comes from the government, specifically the Department of Health and Human Services.

Under Secretary Tom Price, the department has been a fount of anti-ACA rhetoric. But in an annual report about the ACA’s risk-management provisions issued Friday, Health and Human Services established that the key programs are “working as intended,” protecting insurers from unexpectedly large risks and moderating premiums for consumers.

Not only that, the data “would seem to refute the commonly held belief that the marketplace population is becoming sicker,” observes health economist Timothy Jost, writing in Health Affairs. In fact, according to the figures from 2016 in the latest report, the customer base is getting healthier and the risk pools have been stabilizing.

His proposal, which he’s circulating to his colleagues on typed handouts, wouldn’t explicitly create and fund the special insurance markets, as the House bill did. Instead, insurance experts said, it would create a sort of de facto high risk pool, by encouraging customers with health problems to buy insurance in one market and those without illnesses to buy it in another.

...There is no public legislative language yet, but here’s how Mr. Cruz’s plan appears to work, based on his handout and statements: Any company that wanted to sell health insurance would be required to offer one plan that adhered to all the Obamacare rules, including its requirement that every customer be charged the same price. People would be eligible for government subsidies to help buy such plans, up to a certain level of income. But the companies would also be free to offer any other type of insurance they wanted, freed from Obamacare’s rules.

At the top of the website I have a button linking to an article I wrote for Cracked.com back in May in which I explored about a half-dozen reasons why making major changes to healthcare policy in the U.S. is such a royal pain in the ass. I'm a Single Payer advocate at heart, so it was mostly written from that perspective, but really, most of the points I made would apply to any major policy change.

One thing you may notice in reading the piece is that at no point do I address the cost/payment side of moving the entire U.S. over to a universal, federally-funded Single Payer system; I stick mostly to the logistical side of things (What to do with 2-3 million industry workers? What about the Hyde Amendment? Etc, etc). These are all reasons why I'm convinced that achieving such a system would have to be done in stages. That doesn't mean tiny stages, mind you; "incremental" simply means "more than one step", so it could be, say, 4-5 stages phased in over 20 years or whatever...just not all in one shot.

As longtime readers know, I've often separated the problems with the ACA into several categories:

Some were inherent in the original bill as signed into law.

Yes, many of these only exist because of futile attempts to win over support from Republicans (or a handful of blue dog Dems), but the Democrats are still responsible for them. This includes things like the APTC tax credits being too skimpy, the "family glitch", the "skinny ESI glitch" and so forth. In these cases, the GOP can certainly be criticized for refusing to help resolve those issues, but that's a matter of "passive" obstruction as opposed to overtly doing so.

Several regular commenters here at ACA Signups have been wondering why the Congressional Budget Office keeps using March 2016 as the "baseline" for projecting the net impact on healthcare coverage numbers under the GOP's Trumpcare bills (the House's AHCA and the Senate's BCRAP), as opposed to the more recent January 2017 baseline. After all, according to the March 2016 baseline, the CBO was projecting that under the ACA, the total individual market would have 25 million people as of 2026 (18 million on the exchanges plus another 7 million off-exchange), whereas under the January 2017 baseline, their projections are for the individual market to only be 20 million as of 2027 (13 million on the exchanges plus 7 million off-exchange). Taken at face value, this would seem to suggest a 5 million enrollee discrepancy. This drumbeat has been taken up more recently by GOP Senators, particularly Wisconsin Senator Ron Johnson.

*UPDATE: FOR GOD'S SAKE PEOPLE, THE HEADLINE IS SNARK. THAT'S KIND OF THE POINT. SHEESH.

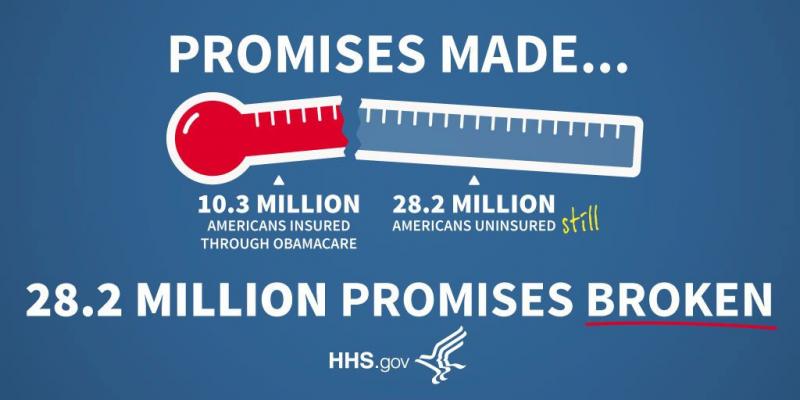

So, the taxpayer-funded Trump/GOP propaganda campaign continues, with HHS Secretary Tom "Inside Trader" Price posting the following tweet:

Only 10.3 million Americans are on the #Obamacare exchanges while 28.2 million have no insurance at all. We need relief now. pic.twitter.com/s4RRoRGJlF

Their initial requests ended up boiling down to a weighted average of around 17.2% on the individual market and 8.2% for the small group market. At the time, however, I was still figuring out how to sort out the Trump Tax Factor: That is, the portion of the requested rate hikes which can be blamed specifically on 2 major factors: The GOP's refusal to pass a 64-word bill formally appropriating CSR reimbursement payments unless it's tied to the rest of their #BCRAP bill (and Trump's constant, public threats to cut off CSR payments altogether unless the #BCRAP bill passes); and Trump/Tom Price's ongoing threats/overt suggestions that they're not going to bother enforcing the individual mandate penalty at all.

This year, to the best of my estimates, Tennessee's total individual market consists of roughly 300,000 people, around 2/3 of whom are enrolled via the federal ACA exchange. Humana is dropping out of the state next year, meaning roughly 79,000 enrollees will have to shop around.

To my knowledge, there are actually 6 individual market carriers in Tennessee this year: Aetna, TRH (Tennessee Rural Health), Blue Cross Blue Shield, Cigna, Humana and "Freedom Life" (which, again, is basically a phantom carrier with no enrollees). Aetna and Humana are out, so that leaves TRH, BCBSTN and Cigna. TRH doesn't appear to have submitted an official 2018 rate filing as of yet, but they only had 3,500 enrollees this time last year anyway, so likely won't have much impact on the overall weighted average rate hikes.

So, the other day the CBO issued their score of impact of the GOP Senate's #BCRAP bill on both healthcare enrollment as well as the U.S. Federal Budget. While most people have been focusing on the impact on how many additional people are projected to be uninsured as of 2026 if the bill becomes law, there's also been a lot of understandable backlash over the massive cuts to non-ACA Medicaid spending: A reduction in projected spending of 26% as of 2026 and 35% by 2036:

The Senate Republican healthcare plan's proposed cuts to Medicaid, one of the most contentious parts of the bill, get progressively steeper over time, according to a Congressional Budget Office analysis released Thursday.

The nonpartisan CBO on Monday released its first analysis for the Senate bill, the Better Care Reconciliation Act, and estimated that provisions in the BCRA would result in $772 billion in cuts to Medicaid by 2026.

That amounts to 26% less funding for the program than than under the current law, the Affordable Care Act.