2021 Requested Commercial Health Insurance Rates Have Been Submitted to OHIC for Review

CRANSTON, R.I. (July 21st, 2020) – The Office of Health Insurance Commissioner (OHIC) today released the individual, small, and large group market premium rates requested by Rhode Island’s insurers. The requests were filed as part of OHIC’s 2020 rate review and approval process (for rates effective in 2021). Tables 1 – 3, below, summarize the insurers’ requests for 2021, and provide the requested and approved rate changes for the previous two years. Two insurers, Blue Cross Blue Shield of Rhode Island (BCBSRI) and Neighborhood Health Plan of Rhode Island (NHPRI) filed plans to be sold on the individual market for persons who do not receive insurance through their employer. In addition to BCBSRI and NHPRI, UnitedHealthcare and Tufts Health Plan filed small group market plans. Five insurers (BCBSRI, UnitedHealthcare, Tufts Health Plan, Aetna, and Cigna) filed large group rates.

ST. PAUL, Minn.—Searching for MNsure on the internet can yield misleading results. If you search for MNsure, you may see ads and websites that appear to be the official MNsure website but are not. Some of these sites collect your contact information and either bombard you with phone calls or try to sell you sub-standard health insurance. Here’s how to be sure you’re working with MNsure and purchasing comprehensive health care coverage:

Those eligible for the urgent need program must:

Check the website URL: make sure you’re clicking on MNsure.org when using a search engine or simply type MNsure.org into your address bar.

July 23, 2020 - Early 2020 Effectuated Enrollment Snapshot

This report provides effectuated enrollment, premium, and advance payments of the premium tax credit (APTC) data for the Federally-facilitated and State-based Exchanges (“the Exchanges”) for February 2020 and for the 2019 plan year.

February 2020 Effectuated Enrollment Snapshot Key Findings

The data below comes from the GitHub data repositories of Johns Hopkins University, execpt for Rhode Island, Utah and Wyoming, which come from the GitHub data of the New York Times due to the JHU data being incomplete for these three states. Some data comes directly from state health department websites.

Here's the top 100 counties ranked by per capita COVID-19 cases as of Saturday, July 25th (click image for high-res version):

The Connecticut Insurance Department has posted the initial proposed health insurance rate filings for the 2021 individual and small group markets. There are 14 filings made by 10 health insurers for plans that currently cover about 214,600 people.

Important: As noted below, the 214,600 figure is Connecticut's individual & small group market combined.

Two carriers – Anthem and ConnectiCare Benefits Inc. (CBI) – have filed rates for both individual and small group plans that will be marketed through Access Health CT, the state-sponsored health insurance exchange.

The 2021 rate proposals for the individual and small group market are on average slightly lower than last year:

Unfortunately, it looks like only some of the 2021 ACA individual market premium rate filings have been uploaded to the SERFF database as of today, so I'm unable to calculate anything even close to an accurate weighted average. There are, however, several noteworthy items on the TX market:

It's been a solid year since Joe Biden rolled out his own official healthcare policy proposal. I did a fairly in-depth writeup on it last summer, but it's the understatement of the year to say that "a lot has changed since then".

The two most obvious developments on this front are 1. Biden has gone from one candidate of two dozen to being the presumptive Democratic Nominee; and 2. The COVID-19 pandemic has completely upended not only the Presidential race but the economy and the entire U.S. healthcare system. A third important (if less consequential) development is that the House has actually passed their own "ACA 2.0" bill in the form of H.R. 1425, the Affordable Care Enhancement Act, which partially overlaps Biden's healthcare plan.

Tennessee has also posted their preliminary 2021 rate filings for both the individual and small group markets. Aside from being one of the few states where a significant number of carriers are including any COVID-19 pandemic factor at all (in both markets), Tennessee has several new entrants and one significant withdrawl (I think).

On the individual market, UnitedHealthcare is newly entering, while Cigna is expanding their coverage areas as noted here. Cigna is also newly entering Tennessee's small group market, as is Bright Health Insurance.

Overall, Tennessee carriers are asking for a 10.3% increase on the indy market (the second highest so far after New York's 11.7% average), mostly driven by Blue Cross Blue Shield, which holds a whopping 83% of the market. On the small group market, the average increase is 5.5%.

COVID-19 accounts for 1.7 points of the increase on average in the indy market and 2.6 points in the small group market. This, again, is the highest statewide average COVID impact I've seen after New York state so far.

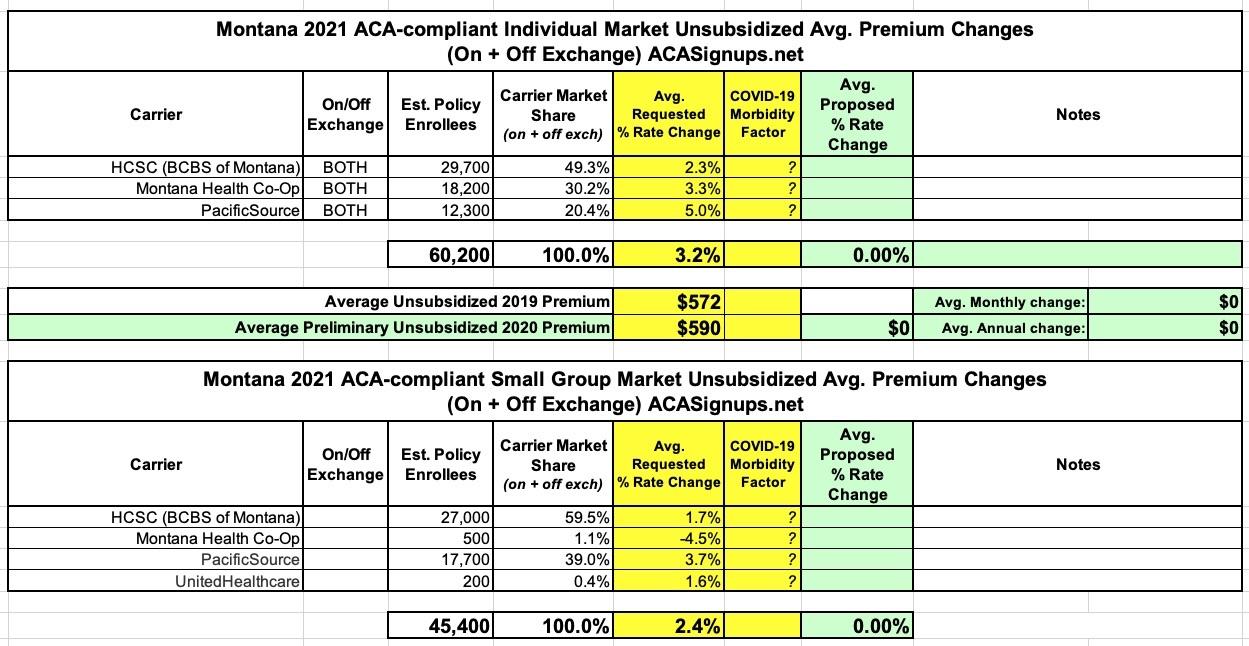

Last year, thanks to the Section 1332 Reinsurance waiver allowed for by the ACA, Montana health insurance carriers reduced their premiums for 2020 by 13.1% on average on the individual market, while raising them by 7% on the small group market (which the reinsurance program doesn't impact).