A REALLY DEEP DIVE into the updated "Medicare for America" bill.

Wed, 05/01/2019 - 2:00pm

NOTE: Back in January, I wrote up an extensive explainer about the "Medicare for America" (Med4Am) universal healthcare coverage bill introduced in December by Democratic Representatives (and Progressive Caucus members, I might add) Rosa DeLauro and Jan Schakowsky.

Regular readers know that I've been a fan of the basic #Med4Am framework for over a year, dating back to the "Medicare Extra for All" proposal introduced by the Center for American Progress (CAP) back in April 2018.

Yesterday, DeLauro & Schakowsky have introduced a modified, improved version of Medicare for America, with some important changes. I'm therefore posting an updated version of my January explainer of the bill, with notes about what's changed since the December version.

There's a half-dozen or more different healthcare policy overhaul bills which are being batted around by Congressional Democrats these days, ranging from the fairly modest ("lower the Medicare buy-in to age 50!") up through the full-blown, "pure" Single Payer bill being pushed by Sen. Bernie Sanders, Rep. Pramila Jayapal & other "Medicare for All" activists.

Over a year ago, CAP's plan was rather awkwardly titled "Medicare Extra for All" (MEFA), and it's based in large part on three previous proposals:

- Congressman Pete Stark's "AmeriCare" Health Care Act,

- Institute for Social & Policy Studies Jacob Hacker's "Medicare Part E", and

- Jon Walker of ShadowProof's "Medical Insurance & Care for All" (MICA)

Anyone who read my analysis of CAP's "MEFA" plan knows that I was pretty excited about it. In short, I concluded that a proposal along these lines would:

- ...piss off the fewest people as possible, while...

- being scaled up gradually enough to cause minimal disruption, but...

- quickly enough to achieve universal coverage within a reasonable timeframe.

CAP's MEFA proposal was eventually modified into full legislative text by Reps DeLauro and Schakowsky last December, and on Wednesday, May 1st a modified version was re-introduced by both of them with some important changes:

Congresswoman Rosa DeLauro (CT-03) and Congresswoman Jan Schakowsky (IL-09) today reintroduced the Medicare for America Act—a bill that would ensure universal, affordable, high-quality healthcare coverage. Medicare for America builds on the success of Medicare and Medicaid by expanding these programs’ covered benefits and services to include prescription drugs, dental, vision, and hearing services, as well as long-term supports and services for seniors and Americans living with disabilities. Medicare for America also achieves universal coverage while preserving quality employer-sponsored insurance. Americans who are uninsured or do not have employer-sponsored insurance—including those currently on the individual market—would be auto-enrolled into Medicare for America.

This is precisely the point I was making in my MEFA analysis from last year. One of the trickiest parts about trying to overhaul the entire U.S. healthcare system is twofold:

- On the one hand, there's nearly 30 million Americans still uninsured, and another 20 million or so are covered via a hodge-podge of healthcare plans ranging from pretty good (subsidized individual market enrollees) to crap ("short-term plans" and so forth). Pretty much all of these folks would be far better served by being added to a more comprehensive Medicare/Medicaid-style public program with lower out of pocket costs than whatever they're on (or not on) today.

- On the other hand, nearly half the population (around ~160 million or so) are covered through their employers...and while plenty of those with employer coverage hate it, polls consistently show that a large majority of them are fairly satisfied with it (at least to the point that they aren't happy about the prospect of it being torn away and replaced with an all-new, unknown/unproven system, anyway).

The thing about health insurance risk pools is that you need low-cost healthy people enrolled in order to help cover the expenses for high-cost sick people. In order to do this, you have to make participation mandatory to some degree to prevent healthy people from skipping out when they're healthy but gaming the system when they become sick.

At the same time, people who are satisfied with their current system tend to hate being forced into participating in a Big Government Program (remember the massive backlash over President Obama's "If You Like It You Can Keep It" statement? The ACA only "forced" around 5-6 million people to switch policies, yet the outrage was so fierce and loud that he had to tell his HHS Dept. to issue a 1-year extension of noncompliant plans...which was later bumped out to three years, then four, then five...)

The "Medicare for America" bill, along with the three previous proposals it's modeled after, neatly walks this tightrope by making a vastly improved/enhanced "Medicare" program mandatory for the half the country least likely to object but optional for the half of the country most likely to object.

Besides DeLauro and Schakowsky, the bill has 16 other cosponsors in the House: Joe Kennedy III (MA-04), William Lacy Clay (MO-1), Eleanor Holmes Norton (DC-AL), Raúl Grijalva (AZ-03), Salud Carbajal (CA-24), Lori Trahan (MA-03), Tim Ryan (OH-13), Sheila Jackson Lee (TX-18), Bennie Thompson (MS-02), Lucille Roybal-Allard (CA-40), Betty McCollum (MN-04), Gwen Moore (WI-04), Bobby Rush (IL-01) and Brian Higgins (NY-26)

“Our country has long aspired to create a universal healthcare system that gives people quality coverage without the fear of skyrocketing costs and the hassle of unnecessary complexity. Medicare for America puts us squarely on that path,” said Congresswoman DeLauro. “With an extensive benefits package, caps on premiums and out-of-pocket costs, no deductibles, incentives to expand our healthcare workforce, and the power to bring down high drug costs, Medicare for America will ensure every American has access to high-quality, affordable coverage they can rely on.”

The "no deductibles" part is the first important change since December. Originally they were going to cap deductibles at $350/individual or $500/household, but they thought better of this and decided to simplify the cost sharing provision. I applaud this...while I'm not opposed to reasonable premiums and co-pays, I hate deductibles and based on my interactions, they confuse the hell out of people even when they aren't sky-high. Good riddance to deductibles, I say!

“We need bold ideas to transform our health care system and reach the goal of universal coverage in the United States. Medicare for America is one of those ideas, and I am proud to join my friend Representative DeLauro to introduce a bill that is one solid plan to achieve that goal,” said Congresswoman Schakowsky. “I am working with my colleagues to improve health equity and access this Congress, and Medicare for America is a proposal that gets us there. As a member of the Medicare for All Caucus, I believe that every person in America deserves high quality, affordable, and comprehensive health care. Medicare for America achieves that goal by including coverage for all reproductive health care, allowing for transparency and negotiation on prescription drug costs, improving long-term services and supports for seniors and Americans living with disabilities, and strengthening our health care workforce. Most importantly, Medicare for America provides universal coverage, covering each and every American.”

AGAIN: Not only are both DeLauro and Schakowsky members of the House Progressive Caucus, Schakowsky is also a cosponsor of the House Medicare for All bill. This does not have to be an ugly, acrimonious debate...they're just two different paths towards the same end goal.

Under Medicare for America, individuals and families will have no out-of-pocket costs for preventive and chronic disease services—including pediatric, maternity, and emergency services—long-term services and supports, and prescription drugs—generic or brand name as necessary. Medicare for America also lifts the current prohibition on Medicare’s ability to negotiate prescription drug prices—a ban that has kept drug prices artificially high and increased healthcare costs for millions of Americans.

This is an important point: While Med4Am does have (reasonable...see below) co-pays and coinsurance for some services, there's none of that for a bunch of other stuff.

The inclusion of long-term supports & services (LTSS) is a very big deal...this was part of the bill from the CAP/MEFA plan over a year ago, and it has since been adopted by both the House and Senate versions of "Medicare for All". The LTSS component is getting a ton of praise from various disability community representatives:

...Currently, there is incredibly limited access to long-term supports and supports in Medicare and private insurance, leaving Medicaid as the primary payer for these services and supports. With an emphasis on home and community-based settings, Medicare for America establishes and guarantees access to long-term support and services.

“We are grateful to Representatives DeLauro and Schakowsky for including long term services and supports (LTSS) as part of the Medicare for America bill,” said Nicole Jorwic, Senior Director of Public Policy of The Arc of the United States. “This will address the current institutional bias in the Medicaid program and increase access to the supports and services that allow people with disabilities to access the community, including people on waiting lists for these services all over the country. The inclusion of LTSS is an important recognition of the value of the lives of people with disabilities and the right that all people should have to a life in the community.”

“The Medicare for America bill takes a big and bold approach to providing the basic right to affordable healthcare for all Americans, including the essential care and services seniors and people with disabilities need to live with dignity at home,” said Terrell Williams, a New Haven, Conn. home care worker and member of SEIU District 1199 New England. "The proposed bill recognizes that we must have a stable healthcare workforce and will look at our wages and other policies to keep dedicated workers. I have no doubt that this bill is a big step forward for working people and that the best way to raise our wages and advocate for better job and quality of care standards is by giving all workers the opportunity to join together in unions.”

“The Consortium for Citizens with Disabilities is thankful to Representatives DeLauro and Schakowsky for including long term supports and services in the Medicare for America bill introduced today,” said Lisa Ekman, Chair of the Consortium for Citizens with Disabilities. “These services are imperative for people with disabilities and older adults to live healthy lives in their communities.”

“Health care is a human right, and one that is of vital importance to allow the millions of Americans with complex medical needs and disabilities, including children, to survive and thrive,” said Elena Hung President and Co-founder of Little Lobbyists. “We are so grateful that, in drafting Medicare for America, Representatives DeLauro and Schakowsky worked closely with the disability community to ensure a health care system that includes and supports people with disabilities. In particular, Medicare for America's robust community-based long term supports and services, and coverage for all children currently on waiting lists for Medicaid/Medicaid waiver programs, would provide necessary care - and peace of mind - to millions of Americans. These benefits are necessary in any truly universal health care proposal, and we will continue to work to ensure that any health care reform reflects the needs and input of the disability community.”

This next section is newly-added and very smart:

Given the intended expansion of healthcare coverage to tens of millions more people, Medicare for America also accounts for the need to ensure there are enough healthcare providers by creating a new student loan forgiveness program for healthcare workers like direct care workers, mental health counselors, licensed marriage and family therapists, physician assistants, pharmacists, dentists, dental hygienists, doctors, and nurses. The program will forgive 10 percent of student loan debt for each year the provider or institution the provider works for accepts the Medicare for America plan.

This kills two birds with one stone: Not only does it address one of the biggest concerns about moving to a universaly healthcare system (long lines/short supply of providers), it also addresses one of the major reasons many healthcare providers (especially some doctors) push for high pay rates: In many cases they're simply trying to get out from under massive student loan debt. Under this proposal, if they agree to accept Med4Am payment rates for 10 years, their entire student loan debt burden will be completely eliminated. Clever.

If enacted, Medicare for America would fix the current two-tiered healthcare system by banning private contracting. The wealthy and well-connected currently use private contracting to pay for care from providers who do not accept health insurance and demand to be paid completely out of pocket. Meanwhile, the vast majority of Americans—who rely on their health insurance to defray the high cost of care—cannot afford to receive care from these providers.

I believe this is a new provision. I think this is the same thing known as "concierge medicine". I honestly don't know enough about how big of an impact this currently has on healthcare costs and the like. Here's the actual wording of this section:

‘‘(f) NO PRIVATE CONTRACTING.—A health care provider or health care institution are prohibited from entering into a private contract with an individual enrolled under Medicare for America for any item or service coverable under Medicare for America.

If I'm reading this correctly, it sounds like doctors or hospitals could enter into a private, direct care agreement...but only with those not enrolled in Med4America, which means those who keep their employer-sponsored coverage. I'll have to think about this one a bit.

How much would it cost the enrollees? This is where the two changes I already knew about can be found:

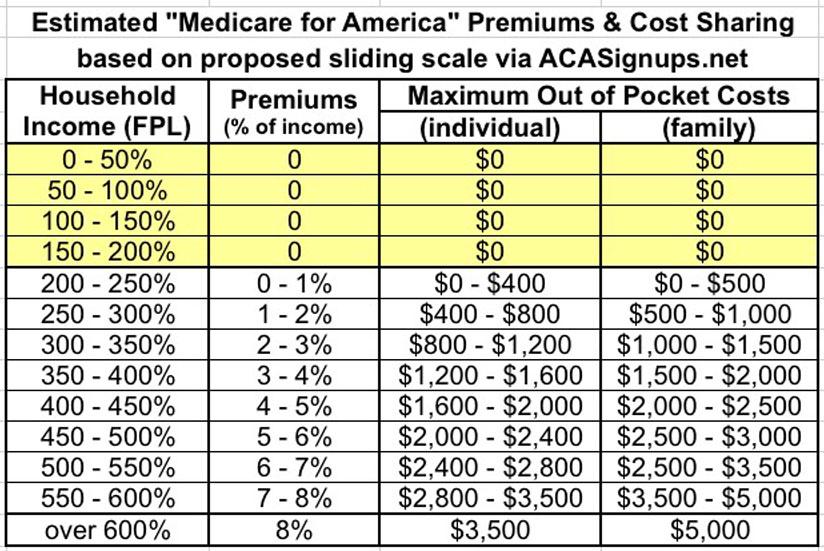

Medicare for America offers a simple, transparent cost structure. Individuals and families will have no deductibles. Individuals will have a $3,500 maximum out-of-pocket spending, and households will have a $5,000 maximum out-of-pocket spending. Medicare for America also ensures coverage is affordable for all by capping individual and household premiums at 8 percent of their monthly income. Individuals or families making less than 200 percent of the Federal Poverty Level will not pay a premium or have a maximum out-of-pocket spending threshold. And individuals or families with incomes between 200 percent and 600 percent of the Federal Poverty Level will receive subsidies to lower their premium contribution and will have their maximum out-of-pocket spending established on a sliding scale.

Again, the removal of deductibles altogether is great. The other change here is that they've lowered the upper limit on premiums from 9.69% of income down to 8.0%. There's no actual rate chart in the legislative text (which I'm a little surprised at), but the 200-600% range means that it will likely look something like the following:

Again: Anyone earning less than 200% of the Federal Poverty Line (around $25,000/year if you're single, around $50,000/year for a family of four) would pay nothing. Zilch. Zero. That's fully 28% of the total population. For them, there would be essentially no difference between this and a Bernie Sanders/Pramila Jayapal-style Medicare for All-like system. If they earn more than 200% FPL, they'd pay anywhere from 0 - 8% of their income.

For instance, right now a single 40-year adult earning $30,000/year (247% FPL) has to pay about 8.25% of their income ($2,475/year) for a Silver plan; it would likely have roughly a $6,000 deductible and a $7,900 maximum out of pocket total.

Under Med4Am, they'd likely pay around 1% of their income ($300/year) for a plan covering nearly all of their medical expenses; their co-pays/coinsurance would max out at around $400.

The maximum amount they'd have to pay total under the worst-case scenario would drop from $10,375 to just $700. And keep in mind that the current scenario assumes that every doctor, hospital and prescription drug they visit/take is in network; under Med4Am, they'd never have to worry about whether the doctor, hospital, anesthesiologist or whatever was "in network" since pretty much all of them would be.

For the same single adult, if they earned $60,000 (494% FPL), right now they'd have to pay full price...which would likely be around $7,300/year for the same plan. That's 12.2% of their income...whereas under Med4Am (assuming the table above is accurate), they'd only have to pay around 6% of their income ($3,600/year) with a $2,400 MOOP. That's a $6,000 total worst-case scenario vs. $15,200 today.

Here's the summary version of the bill:

Who is Covered?

Medicare for America achieves universal coverage by enrolling the uninsured, those who purchase their health insurance on the individual market, and those currently on Medicare, Medicaid, and CHIP. Large employers can continue to provide employer-sponsored care, if it is gold-level coverage. Or, they can direct that contribution toward their employee’s Medicare for America premiums. Or, employees will have the option to choose Medicare for America over employer sponsored coverage.

AGAIN: For the ~47% of the country with employer-based coverage, if it's great, you can keep it (assuming your employer chooses to...and that's something every employee is already at the mercy of each year as it is anyway). If it sucks, you can switch over to Med4Am.

For the ~37% of the country currently on (today's) Medicare or Medicaid, along with the other ~16% or so on the individual market, non-ACA compliant plans or completely uninsured, it's a significant upgrade for them no matter what.

What Does It Cover?

Medicare for America improves on Medicare’s and Medicaid’s benefits: covering prescription drugs, dental, vision, and hearing services. And unlike Medicaid, your zip code does not determine your benefits. Medicare for America also comprehensively covers long-term services and supports for Americans living with disabilities and seniors, which Medicare and private insurance do not.

You really couldn't ask for much more in terms of what services it covers.

What Does It Cost Me?

Premiums, to be established by the Secretary, will be no more than 8% of individuals’ or households’ monthly income. Current Medicare beneficiaries will pay either Medicare’s premium (how it is presently calculated) or Medicare for America’s, whichever is cheaper. And, individuals and families between 200 and 600 percent of the Federal Poverty Level will receive subsidies. Those below 200 percent will have no premiums or cost-sharing. There will be no deductibles under Medicare for America. Maximum out of pocket costs for an individual (including seniors and current Medicare beneficiaries) will be $3,500; $5,000 for families (based on a sliding scale for individuals and families between 200 and 600 percent of the Federal Poverty Level).

The payment choice for current Medicare enrollees is critical to ensuring they don't freak out: Those already enrolled at the point the Med4Am expansion is rolled out can keep their existing payment level/structure. I suspect for many of them Med4Am will be a hell of a bargain.

What About Employer-Sponsored Insurance (ESI)?

Large employers can continue to provide insurance, if it is gold-level coverage with benefits comparable to Medicare for America. Or, they can enroll their employees in Medicare for America and contribute 8% of annual payroll to the Medicare Trust Fund. Employees can choose to enroll in Medicare for America, even if their employer offers qualifying coverage. And in either case, if an employer contributes to Medicare for America in lieu of ESI or an employee chooses it over ESI, the employee’s premiums will be based on income. And, they will be eligible for subsidies. The same cost-sharing rules apply for these individuals and households.

THIS is the key to the whole program: Employer-sponsored coverage will continue, but only if it's a comprehensive plan. If it's crap, they have to either upgrade to a comprehensive plan or they can shift their employees over to Med4Am and pay a flat 8% payroll tax. Frankly, I'm guessing most employers would prefer to just pay a fee instead of dealing with all the headaches of health insurance anyway (not just the cost, but the administrative overhead/decision-making process, etc etc). And if the employees prefer, they can switch over to MFA regardless of what their employer chooses to do.

What Health Care Providers Can I See?

Health Care Providers who participate in current Medicare and Medicaid remain a participating provider under Medicare for America. The Secretary would establish a process for adding more providers not yet participating in either program. Medicare for America would fix the current two-tiered healthcare system by banning private contracting. The wealthy and well-connected currently use private contracting to pay for care from providers who do not accept health insurance and demand to be paid completely out of pocket. Meanwhile, the vast majority of Americans—who rely on their health insurance to defray the high cost of care—cannot afford to receive care from these providers

Practically all doctors accept Medicare, so this mostly eliminates the "out of network" issue in one shot.

How Are Health Care Providers and Services Reimbursed?

Medicare for America’s rates for health care providers and services would be based on current Medicare and Medicaid rates, while proactively increasing rates for primary care and other mental and behavioral health and cognitive services. The Secretary has the authority to raise rates as needed to ensure there are no barriers to care. In our current system, far too many individuals cannot get the care they need because reimbursement rates are too low.

This is gonna cause some doctors/hospitals to be furious...while others will be thrilled. Medicare currently only pays about 60% as much as private insurance, so it's gonna be a pay cut for many providers...but Medicaid only pays doctors around 45% as much on average, so it'd be a huge pay increase for them. Medicaid reimbursement rates, in particular, vary widely from state to state, so the doctor/hospital/clinic lobbies in some states will be more upset/happy than others. It's important to note that it doesn't say payments would be equal to current Medicare rates, just that they'd be based on them.

What About Skyrocketing Prescription Drug Prices?

Medicare for America would end the Big Pharma giveaway banning Medicare from negotiating drug prices. Under Medicare for America, the Secretary will negotiate prescription drug prices. Additionally, Medicare for America bans the use of prior authorization and step therapy in any type of health insurance: public or private.

The ability to allow Medicare to negotiate drug prices has been one of the holy grails of healthcare reform for decades.

What About Medicare Advantage?

Individuals will have the option to enroll in a Medicare Advantage for America plan, but these plans will need to charge a separate premium if they cover additional benefits. Medicare Advantage plans would also pay Medicare for America rates for benefits and services. The bill also includes the Medicare Advantage Bill of Rights, which would prohibit plans from dropping providers during the middle of the plan year unless they can show cause, and would improve notice to plan enrollees about annual changes to provider networks before they commit to joining the plan.

THIS is something else (in addition to making the program optional for half the country and charging premiums/deductibles, even though those are already part of Medicare anyway) which "pure" single payer activists will likely flip out about. There's a contingent of SP purists who are opposed to any private/profit motive-based provisions being included in a theoretical SP plan. I'm not thrilled about Medicare Advantage, but it seems to be pretty popular, so killing it off seems like asking for more headaches/opposition to the bill without much reason.

While Medicare Advantage plans would still be allowed, they'd have to be at least as comprehensive as the main Med4Am plan, and would face stronger regulations. In a sense, the new "Medicare Advantage" plans would serve the same function that is currently served by Medicare Advantage + MediGap plans, including supplemental/upgraded coverage of things like private hospital rooms, higher-end medical devices and so on.

I'm not an expert on Medicare Advantage, but I think the way it would work is as follows:

- Let's suppose that in a given area, unsubsidized Med4America premiums would officially cost $10,000/year.

- Let's suppose that a given enrollee earns exactly $100,000, so their standard Med4America premiums would cost $8,000/yr (8% of income)

- Let’s say they rack up exactly $10,000 in claims in a year. In that scenario, the government would end up spending a net of $2,000 in claims.

OK, what if the same person enrolled in a Medicare Advantage plan?

- They still pay the same $8,000 to the government, plus another, say, $2,000/yr more to BlueCross (or whoever) for enhanced services (private rooms, etc)

- The government would pay Blue Cross $9,500 to administer the enrollee (95% of what they'd otherwise spend)

- Blue Cross, in the meantime, would pay out the full $10,000 in claims to healthcare providers

- In this scenario, it costs the government net $1,500 ($8,000 - $9,500)...

- ...while Blue Cross earns a net profit of $1,500 ($9,500 + $2,000 - $10,000)

Again, this is grossly oversimplified, but I think it gives the basic idea: Medicare Advantage plans would still be allowed to exist, but would be on a very short leash.

How Is Medicare For America Paid For?

Medicare for America will be financed by sunsetting the Republican tax bill, imposing a 5% surtax on adjusted gross income (including on capital gains) above $500,000, and increasing the Medicare payroll tax and the net investment income tax. Medicare for America also increases the excise taxes on all tobacco products, beer, wine, liquor, and sugar-sweetened drinks.

Everyone wants to go to heaven but no one wants to die to get there. Expanding publicly-financed healthcare coverage to any significant degree will obviously involve raising taxes to some extent.

It's important to note that the Medicare payroll tax referred to here only applies to individuals with incomes over $200,000 or couples earning more than $250,000. Those folks would go from paying 0.9% of their income over that amount to 4.0%. The net investment tax would be increased from 3.8% to 6.9%. Again, this only applies to folks earning more than $200K/$250K.

In other words, the only tax increase which anyone earning less than $200,000/year would see (aside from repealing the GOP tax bill, which everyone hates anyway), is from an increase in the cost of tobacco, alcohol and sugary drinks...all of which are, of course, major contributors to health problems anyway.

States will also need to make maintenance of effort payments equal to the amounts they currently spend on Medicaid and CHIP. For states that did not expand Medicaid, these amounts would be inflated by the growth in gross domestic product (GDP) per person plus 0.7 percentage points. For states that did expand Medicaid, these amounts would be inflated by the growth in GDP per person plus 0.4 percentage points.

After 10 years of payments, they would then increase by the growth in GDP per person plus 0.7 percentage points for all states. This structure would ensure that no state spends more than they currently spend, while giving a temporary discount to states that expanded Medicaid.

That makes perfect sense to me; the states which sat on their asses and refused to expand Medicaid for what would amount to nearly a decade by the time Med4Am was signed into law shouldn't get off the hook.

If states refuse to make the maintenance of effort payments, they will be no longer be eligible for funding under the Mental Health Services Block Grant program, Social Services Block grant program, the Substance Abuse Prevention and Treatment Block Grant program (Federal Health Centers Program), State Targeted Response to Opioid Crisis Grants, Community Services Block grants, Section 330 grants, and the Ryan White HIV/AIDS Program grant program.

The federal government can't legally require that individual states pay into a program which no longer exists, but they can certainly cut off federal assistance to those which don't, so this seems like a pretty compelling move.

OK, let's get into the actual legislative text itself:

- There would be a two-year "ACA Public Option" period to start things off:

The Secretary of Health and Human Services (in this subtitle referred to as the ‘‘Secretary’’) shall establish a public health plan option that is offered in the individual market through the Federal and State Exchanges under title I of the Patient Protection and Affordable Care Act to eligible individuals for plan years 2021 and 2022 in accordance with this subtitle.

- During this 2-year period, there'd be "ACA-level" Silver and Gold plans made available including abortion coverage (see below). States would not be able to deny those plans.

- Premiums for the ACA Public Option plans would be at least comparable to other plans available on the exchange, except that...

- ...Subsidies would follow the same table as noted above ($0 for those under 200% FPL, 0 - 8% of income for those 200-600% FPL, 8% of income over 600% FPL)

This revised premium subsidy table does not appear to apply towards the private exchange policies as well, which would seem to give Med4America one hell of an unfair advantage even during the 2-year Public Option period. HOWEVER, in Section 134, Med4America upgrades the ACA benchmark plan from Silver to Gold, while also beefing up the ACA CSR subsidy formula as follows:

![]()

- Reimbursement rates to providers would be whatever is "necessary to maintain network adquacy", leaving it up to the HHS Secretary to set rates for dental, vision, hearing, reproductive andother services which aren't currently covered by Medicare

- The healthcare provider network would basically include any doctor/hospital which accepts Medicare today...which is the vast majority of them. It would also include the ability for additional providers to jump in.

- For prescription drugs, the existing Medicare Part D formulary would be included.

- One More Time: Yes, abortion would be covered, period. Like both the House and Senate versions of MFA, the Med4America bill would tackle the Hyde Amendment head on. It doesn't technically repeal Hyde...it just says that Hyde "shall not apply" to Med4America. I'm sure this won't cause any controversy or backlash whatsoever...

(d) CLARIFICATION.—Any provision of law restricting the use of Federal funds with respect to any reproductive health service shall not apply to funds appropriated under subsection (b) or with respect to the account under sub-section (a).

AFTER the 2-year ACA Public Option period, the full-blown Med4America plan would kick into place:

‘‘PART A—COMPREHENSIVE HEALTH COVERAGE

‘‘SEC. 2201. ESTABLISHMENT.

‘‘The Secretary shall establish a public health insurance program, to be known as ‘Medicare for America’, which shall for calendar year 2023 and each subsequent calendar year provide comprehensive health benefits in accordance with this part to individuals enrolled for coverage under this title.

It's important to note that the bill defines eligible individuals as:

‘‘(1) a resident of the United States or a territory of the United States;

‘‘(2) an individual who is lawfully present, as defined in section 152.2 of title 45 of the Code of Federal Regulations; or

‘‘(3) an individual who would be eligible for coverage under a State Medicaid plan pursuant to section 1903(v) (as such section was in effect as of the date of the enactment of this title),

In other words, the Med4Am bill should cover pretty much everyone...although it sounds like it would be up to whoever the HHS Secretary is to decide how far that goes in terms of undocumented immigrants. Even if some undocumented immigrants don't end up making the cut, however, it includes this line:

Nothing in this title shall preclude a State from using State funds to provide for an individual’s health coverage who is not eligible under this subsection.

In other words, if California wants to pay for undocumented immigrants to have healthcare coverage, they're free to do so.

Beginning in 2023, the Secretary shall provide a mechanism for the enrollment of individuals entitled to benefits under this title and, in conjunction with such enrollment, the issuance of a Medicare for America card which may be used for purposes of identification and processing of claims for benefits under this title. The card shall not use the individual’s social security number as an identifier. As a condition of participation in the program, participating providers shall facilitate enrollment as specified by the Secretary. The State entities responsible for enrolling individuals in the Medicaid program under title XIX and the Children’s Health Insurance Program under title XXI shall serve as the enrolling entity for Medicare for America within each State.

Interesting...the program itself is federal, but the actual enrollment process will be handled by each individual state's Medicaid/CHIP infrastructure.

Autoenrollments:

‘(A) ENROLLMENT AT BIRTH.—For plan years (beginning with plan year 2023), a process, established by the Secretary in consultation with the Commissioner of Social Security, for the automatic enrollment of eligible individuals born during such plan year.

‘‘(B) CURRENT MEDICARE BENEFICIARIES.— (i) CURRENT MEDICARE BENEFICIARIES.—For plan years (beginning with plan year 2023), a process established by the Secretary for the automatic enrollment of all individuals who are enrolled for benefits under part A or B of title XVIII (other than individuals who are enrolled for such benefits and receiving benefits under title XIX).

‘‘(ii) CONTINUING POPULATION.—For plan years (beginning with plan year 2023), a process established by the Secretary for the automatic enrollment of eligible individuals who attain the age of 65 during such plan year.

‘(iii) DUALS.—For plan years (beginning with plan year 2025), a process established by the Secretary for the automatic enrollment of eligible individuals who are enrolled for benefits under part A or B of title XVIII and receiving benefits under title XIX.

‘‘(C) OTHER INDIVIDUALS WITHOUT QUALIFIED HEALTH COVERAGE.—For plan years (beginning with plan year 2023), a process established by the Secretary for the automatic enrollment of eligible individuals who are not enrolled in other qualified health coverage (as defined in paragraph (4)(B)) for such plan year.

Note the starting years for each population...I'll be going over the full timeline below.

‘‘(B) SMALL EMPLOYERS.— ‘‘(i) IN GENERAL.—For plan years (beginning with plan year 2023), a process and methodology under which a small employer, as defined in section 126(d)(3) of the Medicare for America Act, may provide for the enrollment of the employees of such employer under Medicare for America. For purposes of this subparagraph, the term ‘small employer’ means any employer for any calendar year if the annual payroll of such employer for the preceding calendar year does not exceed $2,000,000 or has fewer than 100 employees.

‘‘(ii) REQUIREMENT.—Small employers shall either provide coverage as defined within the meaning of section 2791(d)(8) of the Public Health Service Act or facilitate the enrollment of their employees into Medicare for America. Small employers facilitating enrollment into Medicare for America will not be subject to a mandatory employer contribution.

Translation: Companies with fewer than 100 employees can either provide Gold-level private coverage or they have to shift their employees over to Med4America. Small business won't have to pay a dime if they do the latter, however, so my guess is that almost all of them will jump at the chance to do so.

‘‘(iii) AUTHORITY.—The Secretary may set standards for determining whether employers are undertaking any actions to affect the risk pool within Medicare for America by inducing individuals to decline coverage under a qualifying employer sponsored plan and instead to enroll in Medicare for America. An employer violating such standards shall be treated as not meeting the requirements of qualified health coverage.

In other words, employers will not be allowed to "dump" expensive/sick employees on the Med4America system while continuing to insure only their healthy employees. I can't imagine this will be much of a problem for small employers, since they'll likely just kick everyone over to Med4America, but it's a necessary precaution for large employers (see below).

‘‘(C) LARGE EMPLOYERS.—For plan years (beginning with plan year 2027), the Secretary shall provide for a process and methodology under which a large employer may provide for the enrollment of the employees of such employer under Medicare for America. For purposes of the preceding sentence, the term ‘large employer’ means an employer with at least 100 employees or whose annual payroll exceeds $2,000,000.

UPDATE: Oh, yeah...two other important requirements for employer-sponsored private insurance:

(2) any other plan or coverage that meets the criteria under subsection (b), includes vision, dental, and hearing benefits, and provides health coverage that is equivalent to an actuarial value of at least 80 percent of the coverage provided under title XXII of the Social Security Act and makes a premium contribution of at least 70 percent.

Such plan shall require a premium contribution from the employer of at least 70 percent regardless of whether cov- erage is for single, spousal, or dependent care.

In other words, if employers want to stick with private group insurance, it has to be solid, comprehensive coverage, and it has to cover the employee's entire family, not just them.

Large companies will have to wait until the 6th year before they can start shifting their employees over to Med4America. This may sound like a long time, but remember that even the ACA's employer mandate provision didn't kick in until five years after the law was signed. Large employers cover something like over 100 million people, so it makes sense to hold off until the dust has settled on all of the other moving parts first.

‘‘(D) MEMBERS OF CONGRESS AND THEIR STAFF.—Beginning for plan year 2023, Members of Congress and their staff, subject to paragraph (4), shall be enrolled in Medicare for America.

Just like under the ACA, Med4America will indeed require Congress to eat their own dog food.

Here's who wouldn't be required to enroll in Med4America:

- First 2 years: Optional for everyone

- 3rd & 4th year: Optional for those enrolled in Medicaid & CHIP

- Permanently optional:

- Those with qualifying (gold level) employer coverage

- Those enrolled in TRICARE

- Those enrolled in the Veterans Administration

- Those enrolled in the FEHB (federal employee health benefits) program

- Those enrolled in the Indian Health Service

What's covered under the full Med4America program: Pretty much everything:

- Ambulatory services

- Emergency care/urgent care

- Hospitalizatoin

- Maternity/newborn care

- Behavorial health services (mental health, substance abuse, home/ community-based)

- Prescription drugs via FDA

- Rehab/habiliative services (physical therapy, speech therapy, occupational therapy)

- Laboratory services

- Preventative/wellness & chronic disease management

- Pediatric services

- Dental care

- Hearing services/hearing aids

- Vision services

- Home & community-based long-term support services

- Chiropractic services

- Durable medical equipment (wheelchairs, walking aids, bathroom equipment, nebulizers, hospital beds, CPAPs, insulin pumps, breast pumps, lymphedemia items, medical wigs, augumentative communication devices, oxygen, orthotic/prosthetics, disposable supplies)

- Family planning (reproducive exams, counseling/education, abortion, contraceptives, voluntary sterilization, infertility treatment)

- Gender-confirming procedures/treatment

- STD/HIV screening/ testing/ treatment/ counseling

- Dietary/nutrition counseling

- Medically necessary food/vitamins

- Nursing facilities

- Acupuncture

- Digital health therapeutics

- Telehealth

- Non-emergency medical transportation

- Care coordination

- Palliative care

- Anything else covered by any State plan

Whew! That's a lot of stuff! Really, it's at least as comprehensive as the MFA bills in terms of scope of coverage.

‘(c) IMPLEMENTING POLICIES.—The Secretary shall establish payment models, quality measures, and other implementing policies that provide further access to the coverage under this title. For purposes of the previous sentence, the Secretary shall consult with stakeholders, including those covering pediatrics, disabilities, and seniors.

This may sound like a minor point, but a lot of disability advocates and advocates for children & seniors are deeply concerned about their specific needs not being accounted for. This requires the HHS Secretary to do so.

Speaking of the scope of coverage:

‘‘(d) PROHIBITION AGAINST DUPLICATING COVERAGE.— ‘‘(1) IN GENERAL.—It is unlawful for a private health insurer (other than an insurer with respect to a Medicare Advantage for America plan under part C of this title or qualified employer-based coverage) to sell health insurance coverage that duplicates the benefits provided under Medicare for America under this part.

‘‘(2) CONSTRUCTION.—Nothing in paragraph (1) shall be construed as prohibiting the sale of health insurance coverage for any additional benefits not covered by this part, insofar as the coverage satisfies the conditions of paragraphs (3) and (4). Nothing shall preclude employers meeting the requirements under section 126 of the Medicare for America Act from providing supplemental coverage under this section to their employees.

In other words, private major medical insurance coverage will be allowed for Employer Coverage (gold-level or better only) and Medicare Advantage only. Supplementary insurance to cover anything not on the list above (private hospital beds and the like) could also be sold standalone, although I'm guessing just about anyone wanting that sort of thing would just go for a Medicare Advantage plan anyway.

‘‘(f) PROHIBITION AGAINST STEP THERAPY AND PRIOR AUTHORIZATION.—Items and services covered under Medicare for America shall be covered without any need for any prior authorization determination and without any limitation applied through the use of step therapy protocols.

I don't know much about step therapy, but I know that patient advocates can't stand it.

PREMIUMS: I already covered most of this above: <200% FPL = zilch; from 200-600% it's 0 - 8% of household income, with maximum out-of-pocket costs of $0 - $3,500. However, there's some important caveats to this starting in 2023 when the fully comprehensive Med4America plans go into effect:

‘‘(1) IN GENERAL.—Subject to paragraph (2), each individual enrolled for benefits under this title for a year shall pay monthly community-rated premiums for such year in an amount determined by the Secretary in accordance with subsection (b).

Community-rated, which means identical for every enrollee. The ACA reduced variances in premiums based on medical condition, gender, etc, but still allowed variants based on age (3:1 ratio), smoking and geographic location. I think this would eliminate everything except geographic region. To be honest, I suspect the robust subsidy structure is such that this won't make much of a difference in terms of what anyone actually pays, anyway.

‘(2) GRANDFATHERED MEDICARE BENEFICIARIES.—In the case of an individual enrolled under part B of title XVIII as of the date of the enactment of this part, the premium applied under this section for such individual for benefits under this title shall be the lesser of—

‘‘(A) the premium otherwise applicable to such individual under such title XVIII if this title had not been enacted; or (B) the premium that would be applied to such individual under this title without the application of this paragraph.

In other words, the ~55 million current Medicare enrollees are gonna get the bargain of a lifetime: They'll keep paying what they're already paying today for Medicare, but with massive expansion of benefits.

This part explains how premiums are handled for employees who are either moved over to Med4America by their employer or who choose to do so individually:

‘‘(4) For an individual whose employer will be making a firm-wide contribution under this title in lieu of offering employer sponsored insurance (as specified in section 126(b)(1)(B) of the Medicare for America Act), such individual shall pay a premium in accordance with this subsection.

‘‘(5) For an individual who has opted out of their employer sponsored insurance in order to enroll in Medicare for America as specified in section 126(c) of such Act, the individual shall pay the lesser of— (A) the premium described in this subsection; or (B) the amount owed after the amount of employer contribution (as specified in section 126(b)(1)(B) of the Medicare for America Act) is subtracted from the premium established by the Secretary of Health and Human Services as described in paragraph (1), whichever is less.

In other words: Let's suppose you're single and earn $50,000/year (around 400% FPL) with employer coverage. Your employer policy premium is $500/month but you only pay $200 of it, with your employer covering the other $300. If you decide to drop that coverage and move to Med4America on your own, your employer would still have to keep paying that $300/month...they'd just pay it to the federal government instead of to their insurance carrier.

I believe this means you would therefore pay the lesser of the same $200/month or around 4% of your income...which in this case would be around $166/month ($2,000/year). Thus, you'd be getting far more comprehensive coverage for $34/month less than you're paying now. In other cases you might be better off continuing to pay what you already are now…except for much better coverage.

Payment of Benefits; Cost-Sharing; Out-of-Pocket Limits

Short version: Med4America will pay 80% of most services with zero out of pocket expenses, but 100% with no out of pocket cost for:

- ‘‘(1) USPTF recommended preventive and chronic disease services.

- ‘‘(2) Long-term services and supports.

- ‘‘(3) Generic drugs, and prescription drugs if medically necessary.

- ‘‘(4) All services for individuals who are medically frail or otherwise have special medical needs, (including children with serious emotional disturbance and adults with serious mental illness), individuals with chronic substance use disorders, or individuals with serious and complex medical conditions (such as epilepsy and HIV), individuals with a physical, intellectual or developmental disability that significantly impairs their ability to perform 1 or more activities of daily living.

- ‘‘(5) Pregnancy related services.

- ‘‘(6) Emergency services.

- ‘‘(7) Services for children under age 21.

Wow. That covers...a lot.

Really, with deductibles wiped out altogether, extremely reasonable Max Out of Pocket caps, 28% of the population not having to pay a dime for anything and no coinsurance for anyone under 21 years old, etc etc as listed above, Med4America is really relying on the premiums (for those over 200% FPL) alone to make up the vast bulk of enrollee cost sharing. And of course even those are limited to 8% of income at the outside.

Other important provisions:

- No Annual or Lifetime Limits on services/benefits (this may seem obvious, but again, right now Medicare does have limits on a lot of stuff)

- No Balance Billing (doctors/hospitals can't try to charge you more than Med4America rates)

- No Private Contracting (I mentioned this above...in short, rich people won't be allowed to buy their way to the front of the line)

- Limits on the use of Flexible Savings Accounts (you can only use them for supplemental services, not core Med4America benefits)

- Network adequacy for Medicare Advantage plans (they'd have to meet reasonable standards)

- Limitation on removal of Medicare Advantage providers (Medicare Advantage plans can't drop doctors/hospitals mid-year without cause, etc.)

- Medicare outpatient observation services (patients who are still under observation status will still be considered inpatient)

- Mental health parity requirement

- Clarification of the definition of pediatric medical necessity in qualifying group coverage

- Safe Staffing Requirements (hospitals would be required to have an adequate number of nurses, orderlies, etc.)

This one is interesting, mainly for how brief it is:

SEC. 135. REPEAL OF BONUS PAYMENTS FOR MEDICARE ADVANTAGE PLANS.

Section 1853(o) of the Social Security Act (42 U.S.C. 1395w–23(o)) is repealed.

Since 2012, Medicare Advantage plans have been receiving bonus payments, as a result of changes made by the Affordable Care Act of 2010 and a CMS demonstration that terminated after 2014. Medicare Advantage plans with quality ratings of 4 or more stars, and plans without ratings are eligible for bonus payments. Between 2015 and 2018, the total annual bonuses to Medicare Advantage plans have more than doubled, from $3.0 billion to $6.3 billion. The rise in bonus payments is due to both an increase in the number of plans receiving bonuses, and an increase in the number of enrollees in these plans.

Some provisions are only relevant for the first few years anyway, but they'd be vitally important during that time:

- Eliminating the 24-month waiting period for Medicare coverage for individuals with disabilities (right now, the only people under 65 eligible to enroll in current Medicare are those with ALS, those with ESRD and those who've received SSDD for at least 2 years)

- Eliminating the waiting period for individuals on State Medicaid waiting lists (right now a lot of people are eligible for Medicaid programs but haven't been enrolled yet due to a processing backlog; this would require HHS to provide funding to make sure they're enrolled within 90 days of the law being enacted)

How much will doctors/hospitals be paid?

Except as provided in paragraphs (2) and (3), the Secretary shall establish rates for benefits and services to be provided to health care providers and suppliers furnishing under Medicare for America based on rates that would be applied (including as computed, updated, and adjusted) under title XVIII or title XIX, whichever is higher, for such type of health care providers and suppliers and item and service if such title remained in effect and, in the case of a type of provider and supplier or item or service coverable under Medicare for America but not otherwise coverable under title XVIII or title XIX, shall provide for rates that ensure adequate access to care.

It's important to note that basing rates on current Medicare rates is not the same as making them identical to current rates, which would be considerably lower than what private insurance reimburses healthcare providers today. Unless I'm misunderstanding, it sounds to me like the HHS Secretary would have pretty wide leeway to decide how much to pay providers...with a couple of important exceptions as noted below:

‘(2) EXCEPTIONS.—For purposes of this section, in applying paragraph (1) the Secretary shall ensure that rates to hospitals for inpatient services or outpatient services furnished under Medicare for America are at least 110 percent of such rates on average or in the aggregate for furnishing such inpatient or outpatient services otherwise applied under title XVIII or title XIX, whichever is higher, except that for hospitals serving underserved areas as specified by the Secretary, such rates are increased as necessary to ensure adequate access to care.

They have to be paid at least 110% of current Medicare, and they have to make sure rural hospitals don't go under.

‘(3) APPLICATION.—In applying rates under title XVIII and title XIX, as applicable, for purposes of this part, the following shall apply:

‘(A) The Secretary shall provide for site-neutral payments for items and services furnished in an outpatient hospital and physician office, the rate of payment for such service shall be the same.

(B) The Secretary shall provide for a mechanism to provide payments for direct and indirect costs of graduate medical education programs without any cap on the number of residency positions for which payment may be made, including payments to hospitals for such programs and to eligible facilities for programs for population health-based residencies and for nurse practitioner post-licensure clinical training, residency, and fellowship programs.

This is a really important addition, and one which I didn't know anything about before. I asked about it and apparently, right now there's only 700 slots available in Graduate Medical Education programs for preventative medicine residents right now, and only half of them are actually funded. Furthermore, it only applies to teaching hospital positions today, as opposed to public health doctors and nurses. I still don't know much about it, but this sounds like a smart move.

‘(C) The Secretary shall increase the average relative value of primary care and other mental and behavioral health and cognitive services by not less than 30 percent in order to ensure adequate access to inpatient and outpatient care.

Again: Primary care, mental health and some other specialties are currently seriously underpaid by Medicare and Medicaid.

‘(D) As a condition of participation in the program, participating providers shall accept Medicare for America rates paid by employer-sponsored insurance plans and Medicare Advantage for America plans.

‘(E) The Secretary shall semiannually review if the rates paid by Medicare for America are creating barriers to care. The Secretary shall have the authority to raise rates as necessary to ensure adequate access to care.

(4) INCREASED FEDERAL MATCH FOR MEDICAID AND THE CHILDREN’S HEALTH INSURANCE PROGRAM FOR YEARS 2023 THROUGH 2027.—The Secretary of Health and Human Services shall pay the difference between the Medicare for America rates and the Medicaid and CHIP rates during the period beginning on January 1, 2023, and ending on December 31, 2027.

It would cover the reimbursement rate gap for Medicaid & CHIP during the transition period.

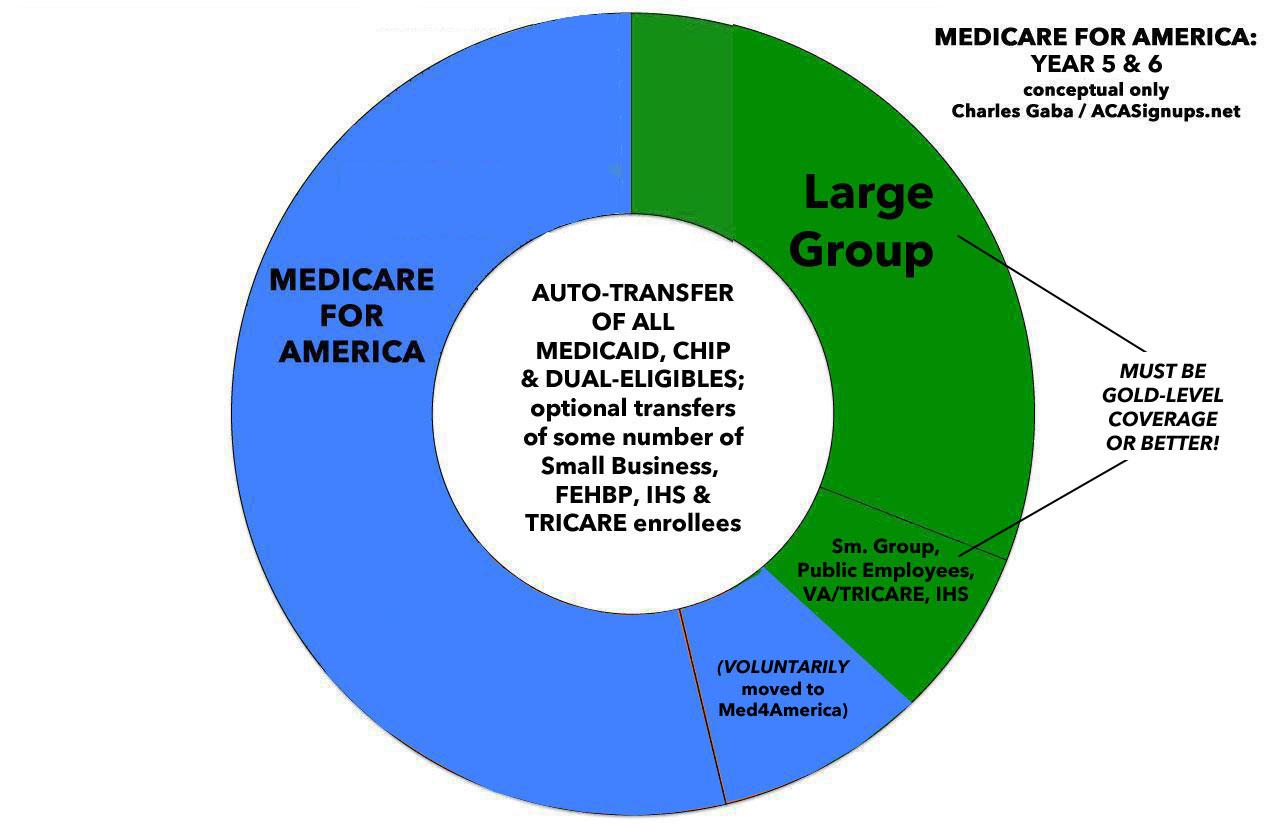

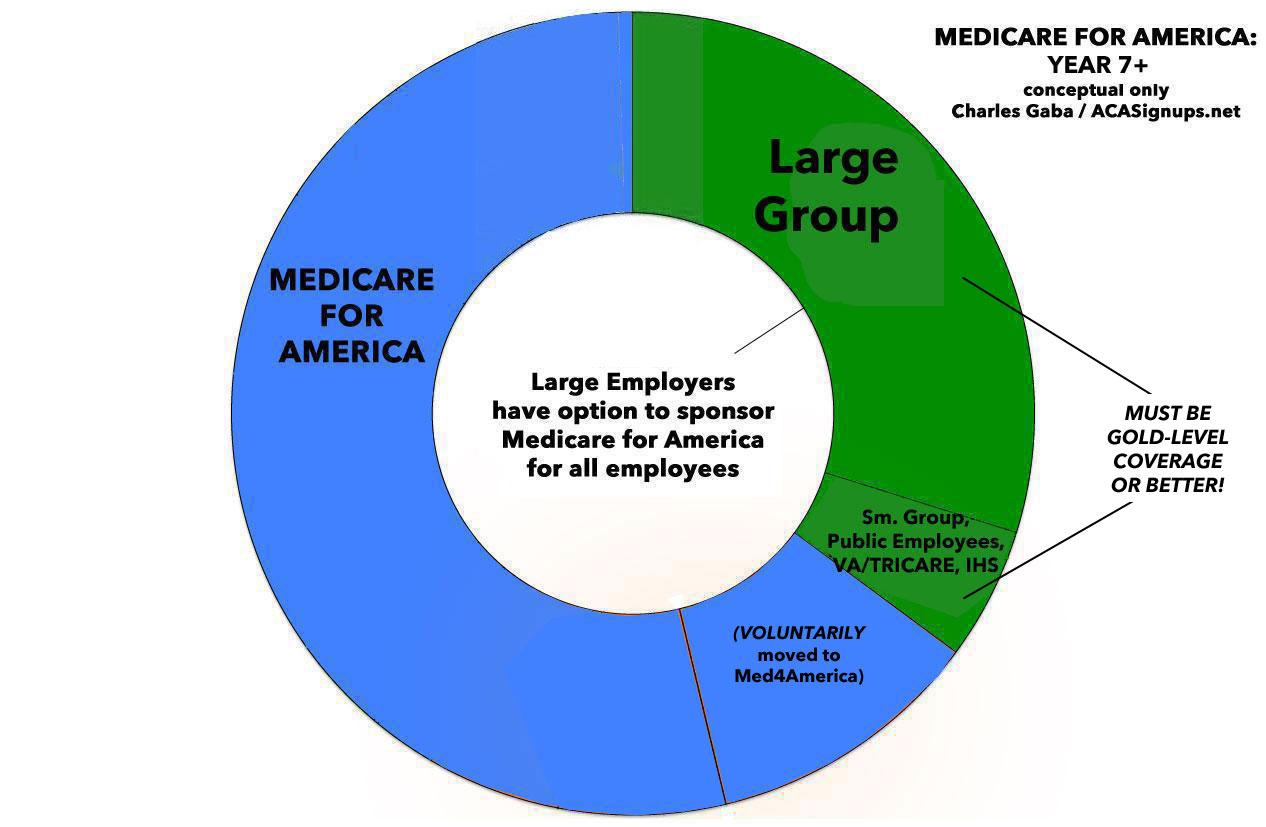

The entire bill itself is over 170 pages long, and I've only really gone through the first 40 or so until here. This post would be easily 2-3 times as long if I covered everything, but I think I'll just add one more section: The timeline.

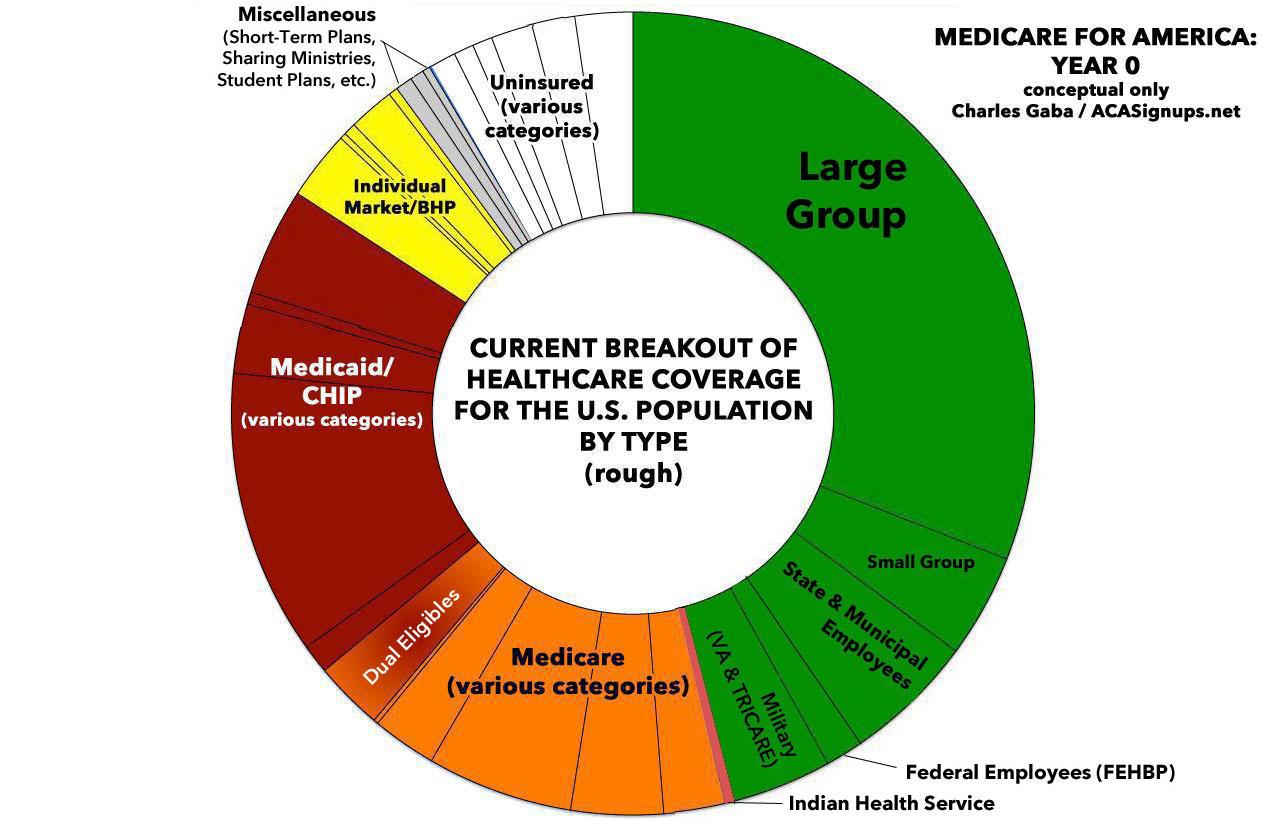

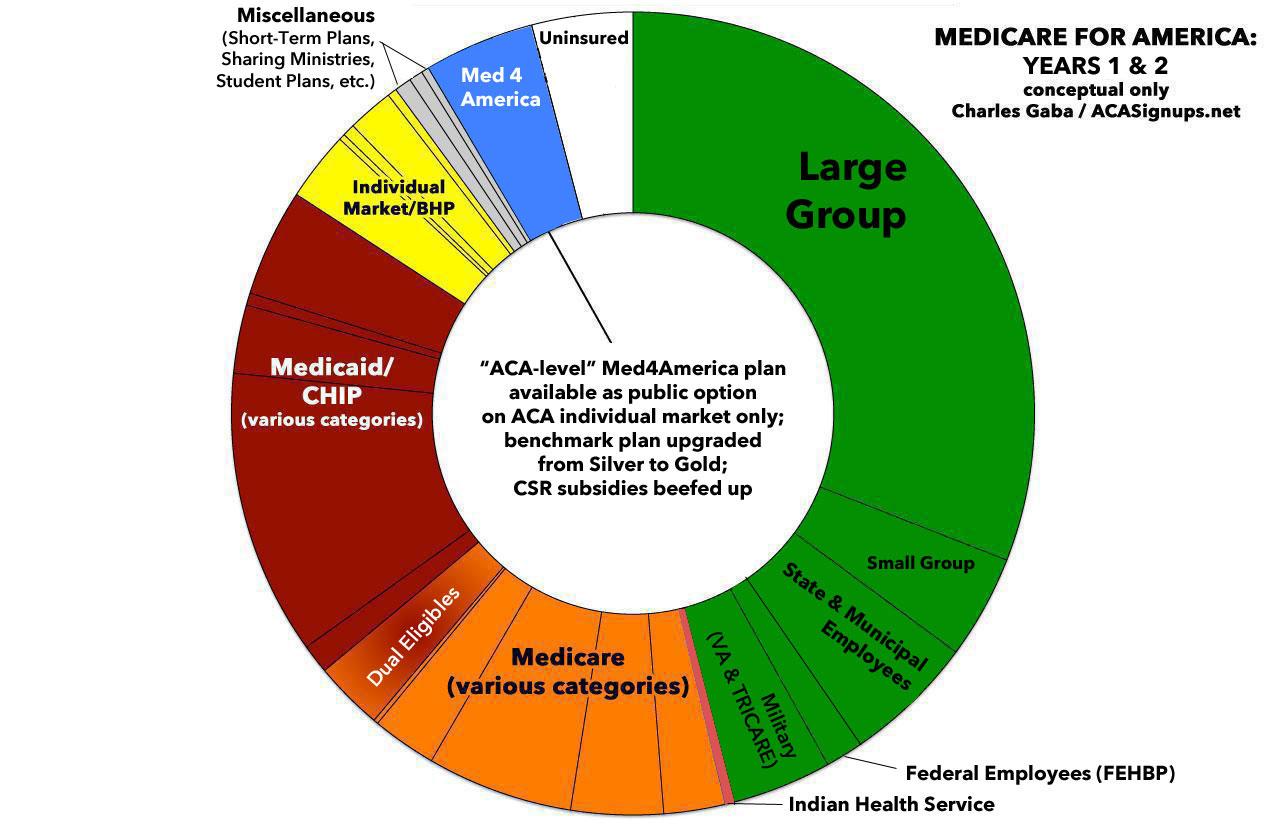

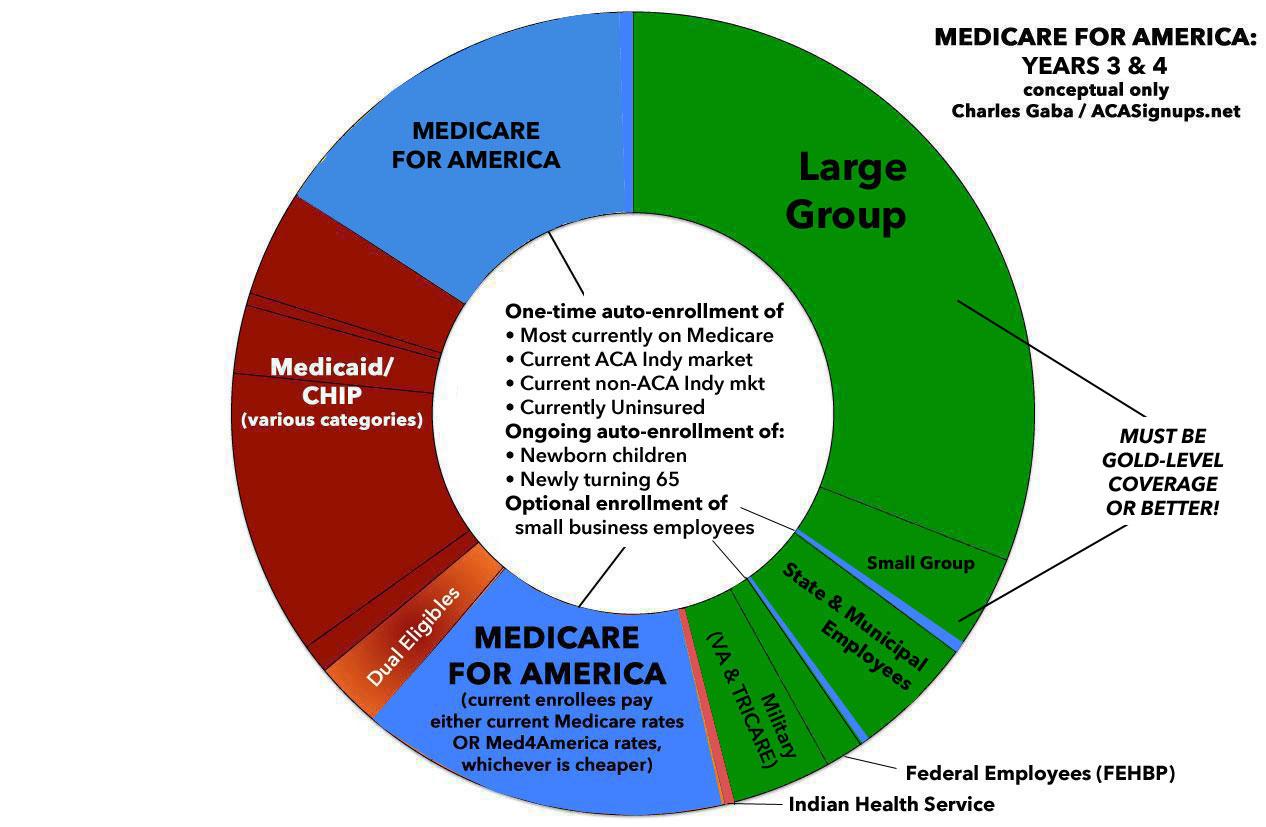

If you scroll down, you'll see that I've used my "Psychedelic Donut" graphic to give a general idea of how the Med4Ameria law would eventually expand to provide comprehensive, universal coverage for everyone.

- Year 1: For the first two years, "ACA-equivalent" plans (that is, not including all of the expanded services yet) would be available on the existing ACA individual market exchanges only, with substantially beefed-up APTC & CSR provisions. Basically, ACA 2.0 + a Public Option for the first two years.

- Year 3: The fully comprehensive version of Med4America starts autoenrolling everyone currently uninsured; those enrolled in the individual market; those enrolled in short-term plans & other non-ACA compliant plans; existing Medicare enrollees (with current Medicare enrollees continuing to pay existing rates); all newly-eligible Medicare enrollees (i.e., those turning 65); and all newborn babies (around 4 million per year). Small businesses could also optionally start enrolling their employees into Med4America as well.

- Year 5: Med4America would absorb the entire Medicaid/CHIP enrollment population, including those enrolled in Medicaid via ACA expansion. This would also be the point at which dual-eligible (Medicare/Medicaid) enrollees would be transferred over. At this point, somewhere between 50 - 60% of the U.S. population would likely be enrolled in the program.

- Years 7+: This is the point at which Large Employers (over 100 employees) would have the option to drop their coverage in favor of shifting their employees over to Med4America and paying a flat 8% annual payroll tax instead.

Assuming all went smoothly (which is obviously a huge assumption), by the 8th year or so, thanks to the continuing auto-enrollments of newborn children and those turning 65 each year, a good 2/3 of the population should be enrolled in Med4America. The FEHBP, IHS, TRICARE and the VA would all remain in place...but those enrolled in the first three programs would have the option of being shifted over to Medicare for America just like those with employer coverage.

After that, it would depend on how the employer-based insurance market holds up. It might stabilize at around that level, still covering 1/3 of the country...or it might continue to gradually shrink away as time went on.

Advertisement