It's Not Over Yet: #ACA Open Enrollment hasn't ended for ~10% of the population!

Fri, 01/04/2019 - 7:44am

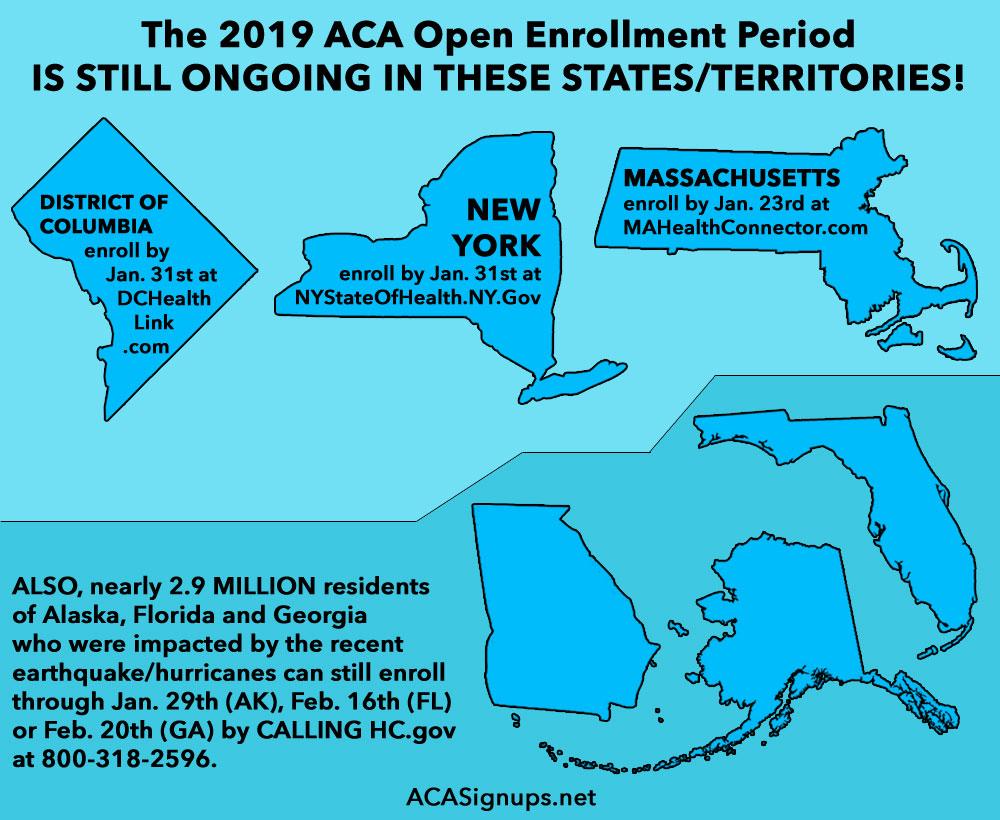

So, it's over, right? Well...not quite. The 2019 ACA Open Enrollment Period officially ended last night...but only in 43 states. In the remaining seven (+DC), Open Enrollment hasn't ended yet. 2019 ACA Open Enrollment is still ongoing for nearly 10% of the population!

- In Massachusetts, open enrollment runs through Jan. 23rd, 2019 for coverage starting February 1st

- In the District of Columbia and New York, open enrollment runs through Jan. 31st for coverage starting March 1st

ALSO...

- 60% of ALASKA residents (around 460,000 people) also have until January 29th to get covered if they were impacted by the recent earthquake by calling HC.gov directly at 800-318-2596

- Areas Eligible: Municipality of Anchorage, Kenai Peninsula and Matanuska-Susitna Boroughs

- FLORIDA residents in 18 counties (around 1.04 million people) who were impacted by last fall's hurricanes have until February 16th to enroll by calling HC.gov directly at 800-318-2596

- Counties Eligible: Bay, Calhoun, Franklin, Gadsden, Gulf, Hamilton, Holmes, Jackson, Jefferson, Leon, Liberty, Madison, Taylor, Okaloosa, Suwannee, Wakulla, Walton, Washington

- GEORGIA residents in 69 counties (around 1.37 million people) who were impacted by last fall's hurricanes have until February 20th to enroll by calling HC.gov directly at 800-318-2596

- Counties Eligible: Appling, Atkinson, Bacon, Baker, Ben Hill, Berrien, Bleckley, Brooks, Bulloch, Burke, Calhoun, Candler, Chattahoochee, Clay, Coffee, Colquitt, Cook, Crawford, Crisp, Decatur, Dodge, Dooly, Dougherty, Early, Echols, Emanuel, Evans, Glascock, Grady, Hancock, Houston, Irwin, Jeff Davis, Jefferson, Jenkins, Johnson, Jones, Laurens, Lee, Macon, Marion, Miller, Mitchell, Montgomery, Peach, Pulaski, Putnam, Quitman, Randolph, Schley, Screven, Seminole, Stewart, Sumter, Tattnall, Telfair, Terrell, Thomas, Tift, Tooms, Treutlen, Turner, Twiggs, Washington, Webster, Wheeler, Wilcox, Wilkinson, Worth

Add all of these up and that's over 30 million people who are still eligible to enroll.

In addition, there are several million people who are still eligible to enroll between January 1st and March 1st via a Special Enrollment Period due to their current healthcare policy being terminated on December 31st.

Oh yeah...and if you do live in these states, you may even qualify for a FREE (as in, $0 premium) Bronze ACA policy:

- Alaska: around 14,400 people

- Florida: around 31,400 people

- Georgia: around 33,700 people

- Massachusetts: 8,800 people

- TOTAL: Around 88,000 people

Here's six more important things to keep in mind for 2019 Open Enrollment:

#2: The Individual Mandate penalty is gone in most states...but it's still around in MA, NJ & DC.

Technically speaking, the ACA's federal financial penalty is still the law of the land...it's just that the amount of the penalty for not having ACA-compliant healthcare coverage (you also qualify if you have Medicare, Medicaid, CHIP or qualifying employer-sponsored coverage) has been reduced to $0 effective January 1, 2019.

However, Massachusetts still has their penalty which predates the ACA, and New Jersey and the District of Columbia passed laws/ordinances to restore the mandate penalty at the state (district) level anyway.

In both NJ and DC it's the exact same penalty as the ACA's has been until now: Either $695 per adult and $347.50 per child in a household or 2.5% of the total household income. Massachusetts uses a completely different penalty formula, laid out here.

The deadline to enroll in New Jersey has now passed, so if you didn't enroll in ACA-compliant coverage already you may face an ugly surprise when you file your state taxes in spring of 2020 if you're unable to acquire ACA-compliant coverage soon (via employer-sponsored coverage, Medicare, Medicaid, etc., or even via HealthCare.Gov if you qualify for a Special Enrollment Period).

Massachusetts and DC residents, as noted above, can still enroll for several more weeks, however.

#3: You may qualify for Tax Credits in 2019 even if you didn't in 2018...and it can make a BIG difference:

- ACA tax credits are based on the Federal Poverty Line, which is increasing by several hundred dollars in 2019.

- Since the threshold for tax credits is 4x the FPL, the income cut-off for being eligible to receive tax credits is actually increasing by $320 for a single person or $2,000 for a family of four.

- That means that if your household income is only a little over the 400% FPL line in 2018 and doesn't change much, you may end up qualifying in 2018 after all. For instance, if you're single and earned exactly $48,300 in 2018, you don't qualify for credits this year...but if you earn the same amount in 2019, you will!

- This year, that could potentially mean saving $2,500 for the exact same policy!

Here's how: Let's say the benchmark silver policy in your area costs $600 at full price, or $7,200/year in 2019. That's 14.9% of $48,300.

Under the ACA, if you earn between 300-400% FPL, anything over 9.6% of your income which the benchmark Silver plan costs is treated as a tax credit towards the difference. Since 9.6% of $48,300 is $4,636, that means you'd qualify for $2,563 in tax credits, or $214/month.

- Therefore, it's vitally important that everyone visit HC.gov (or their state exchange website) & plug in their projected 2019 info to see whether they qualify or not.

#4: Thanks to Silver Loading, SUBSIDIZED enrollees may be able to get a Gold plan at a bargain or a Bronze plan at a steal!

- As I explain here, most states have loaded the full Cost Sharing Reduction (CSR) cost onto Silver plans only. This means that Bronze & Gold plans will only go up the normal amount, while Silver plans will go up a lot...

- ...but the tax credits (for those eligible) also go up a lot to match the Silver increase, and those credits can be applied to any exchange plan...

- ...which means subsidized enrollees may end up getting a Gold plan for less than Silver, or a Bronze plan dirt cheap (or even free!).

- In fact, several states which didn't offer Silver Loading in 2018 are doing so for 2019, and some states which "only" offered "regular" Silver Loading are "upgrading" to full Silver Switcharoo status in 2019.

- Therefore, SHOP AROUND, SHOP AROUND, SHOP AROUND!

#5: HOWEVER, some people who grabbed ahold of extra tax credits this year may LOSE them next year.

- As I explain here, the "benchmark Silver" formula works both ways: If the benchmark premium goes up, so do tax credits for subsidized enrollees...but if the benchmark premium drops, so do those same tax credits.

- If the benchmark premium increases more in hard dollars than bronze or gold premiums do, you can use the higher tax credits to lower the price of the bronze/gold plan by a greater amount...but if the benchmark premium drops by more than the bronze/gold premium does, the opposite is true. Someone who went from $50/month in tax credits to $300/month might drop back down to $50...or even less.

- Therefore, SHOP AROUND, SHOP AROUND, SHOP AROUND!

#6: Unsubsidized enrollees are in a bind...but there's ways of mitigating the problem for most.

- If you earn more than 400% FPL, you don't qualify for any ACA subsidies, so if you shop on the ACA exchange, you'll probably find that Silver policies are insanely expensive...possibly costing even more than Gold plans at full price.

- This is because, again, CSR costs have been "loaded" onto Silver premiums only in most states, raising their premiums substantially.

- Therefore, if you're certain that you won't qualify for ACA subsidies, you may be better off looking for an ACA-compliant policy off-exchange...that is, directly through the insurance carrier itself as opposed to enrolling via the ACA exchange. Most states will offer "off-exchange only" Silver plans which don't have the extra CSR cost attached.

- This could save you literally thousands of dollars next year.

- Alternately, you could simply enroll in a Bronze or Gold plan either on or off-exchange

- HOWEVER, remember that if you do enroll off-exchange, you won't be eligible for tax credits if it turns out you overestimated your income, so only do this if you're certain that you're gonna earn more than 400% FPL in 2019.

#7 Whatever you do, DON'T allow yourself to be PASSIVELY AUTORENEWED!

- Again, the plans, pricing and tax credit formula are gonna be all over the place this year, resulting in some Gold plans being cheaper than Silver, some Silver plans being crazy-expensive, and some Bronze plans being dirt cheap or costing nothing at all.

- That means that anyone who doesn't actively log into their account at HealthCare.Gov, CoveredCA.com, etc. and actively pick the plan they want next year could end up missing out on hundreds or thousands of dollars in financial help, a better-value plan, or both.

- Therefore, I'll say it again: SHOP AROUND!

- Having said that, most of the exchange websites now feature Network and/or Formulary tools to check and make sure that your preferred doctors, hospitals and prescription medications are included in the policy you're signing up for. Make sure to use those tools to check before enrolling. Saving a couple hundred bucks on a policy doesn't do much good if you have to spend a couple thousand on an out-of-network doctor or prescription drug.

Advertisement