UPDATE: Wyoming: APPROVED 2019 #ACA rate hikes: FLAT, but would likely DROP ~12% without #ACASabotage

Sun, 08/05/2018 - 8:15pm

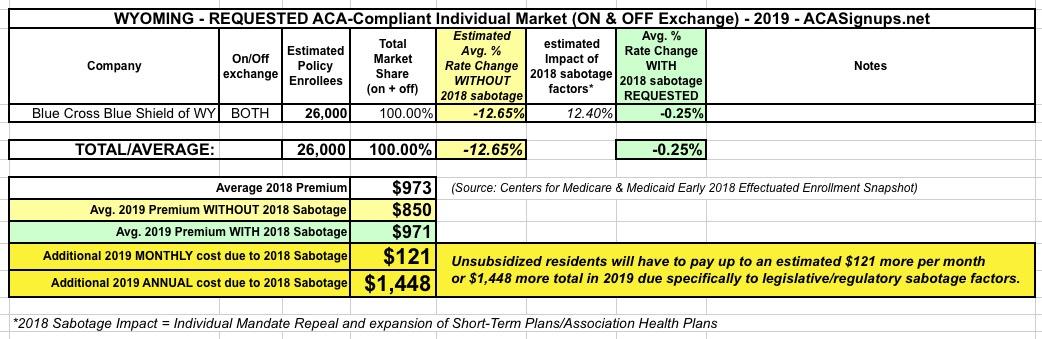

Annnnnnnnd finally, the least-populated state of them all...which also happens to be suffering from the highest average monthly premiums for unsubsidized individual market enrollees: Wyoming.

There's only a single carrier in the Equality State (seriously...that's their motto; who knew?), Blue Cross Blue Shield. They're actually looking to lower rates by just a smidge (0.25% on average).

However, once again, the Urban Institute projected that there'd be roughly an 18.6% increase factor due to the ACA's individual mandate being repeale and short-term & association plans being expanded by the Trump administration.

Assuming just 2/3 of that to play it safe, that still means that unsubsidized enrollees would have been looking at roughly a 12% drop in their 2019 premiums without those measures...a difference of over $120/month, or a whopping $1,400 more apiece next year. Ouch.

UPDATE 10/18/19: This is more of a clarification than an update, really...it looks like the requested rates for 2019 are also the approved rates, according to this press release from the Wyoming Insurance Dept on August 10th...doesn't look like the state insurance commissioner made any changes:

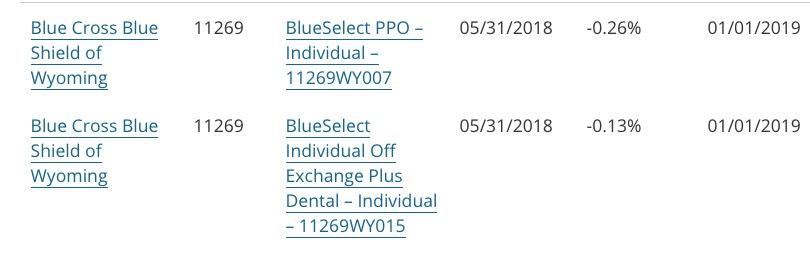

CHEYENNE ------ Blue Cross Blue Shield of Wyoming recently announced its Individual and Small Group Market rates for 2019 plans that are sold on the Market or Exchange and the OffMarket or Off Exchange plans. The Individual On-Exchange plans will see an average of 0.27% decrease from the 2018 rates. Individual Off-Exchange plans will experience an average of 0.12% decrease and the small group Off-Exchange rates will see a minimal 0.01% increase for 2019.

That still averages out to right around a 0.25% drop (perhaps 0.20%, but that's not even a rounding error within the state, and nationally it's not even a blip given that Wyoming only has half a million residents).

Wyoming Insurance Commissioner Tom Glause stated, “I am pleased to see the 2019 rates show that the Wyoming market is stabilizing.” Glause went on to say, “While not every consumer will see their rates decrease, this is a significant change from last year and from the double-digit increases in previous years.” The Department of Insurance (DOI) is also continuing to work on ways to further stabilize the market and to reduce the costs that Wyomingites have experienced in recent years. For example, DOI is conducting an actuarial study and anticipates it will apply for a 1332 Waiver which would allow Wyoming to develop a plan to reduce costs, if the Waiver is approved.

The federal government also recently announced easing the restrictions on short-term limited duration health plans. As the name suggests, these plans are not as comprehensive as Affordable Care Act (ACA) qualified plans. Consumers are well advised to carefully read the language of these plans and to understand that there is not guaranteed enrollment or renewability of short-term limited duration plans. The new federal regulations allow these plans to cover up to 364 days and to be renewed for up to three years, but renewability is at the discretion of the insurer. Glause stated, “It remains to be seen if these short-term plans will have an impact on Wyoming’s market. Regardless, Wyoming consumers should be fully aware of what they are purchasing.”

Advertisement