Florida: Rick Scott comes up with an interesting new campaign strategy...

Wed, 06/13/2018 - 10:28pm

Rick Scott is the Republican Governor of Florida, coming up on the end of his 2nd term in office.

Rick Scott is also running to become the next U.S. Senator from Florida, against incumbent Democrat Bill Nelson.

Prior to being elected Governor of Florida, Rick Scott was the CEO of Columbia/HCA, aka Hospital Corporation of America.

Under Rick Scott's leadership, Columbia/HCA was behind the largest Medicare fraud in history at the time:

Scott started what was first Columbia in 1987, purchasing two El Paso, Texas, hospitals. Over the next decade he would add hundreds of hospitals, surgery centers and home health locations. In 1994, Scott’s Columbia purchased Tennessee-headquartered HCA and its 100 hospitals, and merged the companies.

In 1997, federal agents went public with an investigation into the company, first seizing records from four El Paso-area hospitals and then expanding across the country. The investigation focused on whether Columbia/HCA had committed Medicare and Medicaid fraud.

Scott resigned as CEO in July 1997, less than four months after the inquiry became public. Company executives said had Scott remained CEO, the entire chain could have been in jeopardy.

During his 2010 race, the Miami Herald reported that Scott had said he would have immediately stopped his company from committing fraud -- if only "somebody told me something was wrong." But there were such warnings in the company’s annual public reports to stockholders -- which Scott had to sign as president and CEO.

Scott wanted to fight the accusations, but the corporate board of the publicly traded company wanted to settle.

In December 2000, the U.S. Justice Department announced that Columbia/HCA agreed to pay $840 million in criminal fines, civil damages and penalties.

Among the revelations from the 2000 settlement:

- Columbia billed Medicare, Medicaid, and other federal programs for tests that were not necessary or had not been ordered by physicians;

- The company attached false diagnosis codes to patient records to increase reimbursement to the hospitals;

- The company illegally claimed non-reimbursable marketing and advertising costs as community education;

- Columbia billed the government for home health care visits for patients who did not qualify to receive them.

The government settled a second series of similar claims with Columbia/HCA in 2002 for an additional $881 million. The total for the two fines was $1.7 billion.

On Scott’s 2010 campaign website, he admitted to the $1.7 billion fine, though the link is no longer on the site.

Somehow, despite the fact that Florida happens to be home to the highest percentage of Medicare enrollees in the nation, Scott was elected Governor in 2010 and again in 2014. This being the case, I'm not about to say that the following incident has doomed his Senate race...but it sure as hell isn't likely to have helped him:

Wow: @ScottforFlorida just admitted he thinks returning to a time when insurance companies could discriminate based on pre-existing conditions is a good idea.

“We’ve got to reward people for taking care of themselves...It’s no different from what companies have done the past.”

— American Bridge (@American_Bridge) June 13, 2018

Now, to be fair, he didn't quite say the first sentence; the actual full exchange was:

Reporter: "Have you had time to reflect on the Trump Administration's decision last week not to defend the Affordable Care Act and some of the (???)?"

Scott: "Well, I believe that if you have a pre-existing condition you need to still be able to have healthcare. It's very important to me, I think everyone oughta be able to get healthcare insurance, I do believe that (???) are working to fix the law...I mean that law caused our premiums to skyrocket, but I don't believe in grand bargains, I believe we've been incrementally trying to make change, we've got to allow more competition, to let people buy the insurance that fits for their family, and we've got to reward people who take care of themselves, we've got to..."

Reporter: "What does that mean, like, rewarding people for taking care of themselves...does that mean eliminating community rating and charging more for people who are obese, or..."

Scott: "I think, you know, it's no different from what companies have done in the past...they have smoking cessation programs, and things like that."

Hmmmm...technically speaking, Scott seems to be saying he's opposed to community rating here, not guaranteed issue itself, but most people won't make that distinction, and again, it doesn't really make much difference anyway--saying "you have to sell your policy to everyone even if they have cancer, but you can charge them 100x as much as someone without cancer" amounts to the same thing as "you don't have to sell your policy to them at all" for the vast majority of the public. Either way you're still talking about medical underwriting, asking a bunch of nosy personal questions about their medical history, demanding old medical records and so forth.

In any event, I find it especially noteworthy that a candidate for governor of Florida is saying this, because the potential for guaranteed issue and community rating regulations being threatened by the #TexasFoldEm case would primarily impact people on the individual healthcare market (as opposed to Medicare, Medicaid or Employer-Sponsored insurance).

The thing is, while the ACA-compliant individual market is around 15-16 million people at the moment (around 6% or so of non-elderly Americans), in Florida specifically it's around double that...roughly 13% of the non-elderly population.

In fact, if you limit it to South Florida, it's actually triple that of the rest of the country: Around 19% of the non-elderly population.

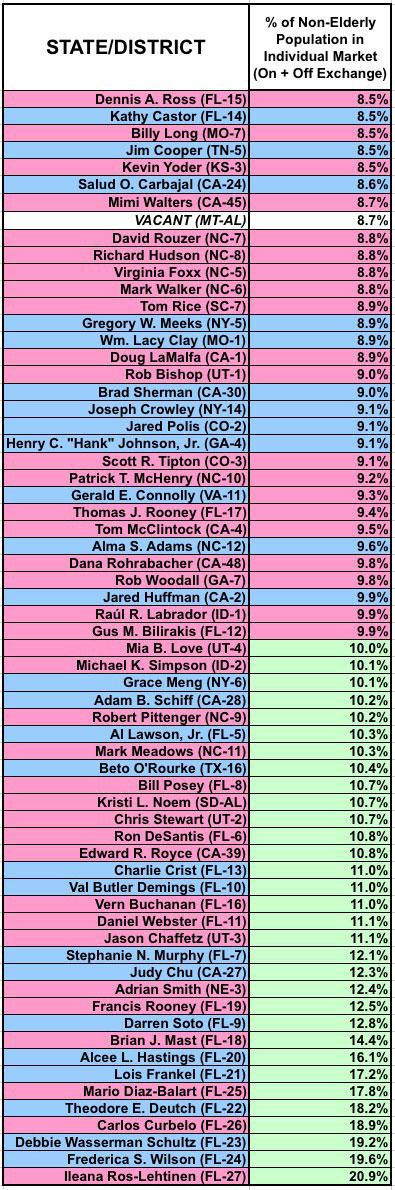

If my estimates are reasonably accurate, this means that nearly 13% of Florida's entire non-elderly population is enrolled in the individual market...including nearly 20% of the non-elderly population across much of South Florida. The highest is Republican-held FL-27, and GOP-held FL-25 and FL-26 are close to 20% as well.

In all 19 of Florida's 27 districts break 10%. I'm assuming that some of the reason for this has to do with Florida simply having a higher percentage of seniors than most states, but that still wouldn't account for the non-elderly population insurance demographics breaking out this way. The proportion between the individual, small group and large group markets should still be roughly the same as other states, shouldn't it?

In short, that's around 2 million Floridians who would be in immediate danger if the guaranteed issue and/or community rating provisions of the ACA were to be stripped away starting on January 1, 2019. Governor Scott might think about clarifying his position on this issue.

For the record, here's my estimates of which Congressional Districts had the highest percentage of their non-elderly population on the individual market from a year ago (obviously a lot has changed over the past year, so some of these may have shifted around a bit, and of course the Montana seat is no longer vacant):

...All 50 states are now completed, and I can state definitively that Florida's individual insurance market is unique across the country. Out of 435 Congressional Districts, only 32 are higher than 10%...19 of which are in Florida. Only 8 are higher than 15%...all of which are in Florida. In fact, the 11 highest-percentage districts are all in Florida.

Advertisement