Remember when Trump's HHS Dept. claimed #ShortAssPlans would only reduce ACA enrollment by ~150K? Yeah, about that...

Fri, 04/20/2018 - 10:22am

So, about a week ago I tweeted this out:

WAIT, I MISSED THIS: The Trump Administration DIDN’T INCLUDE OFF-EXCHANGE ACA POLICIES in their 100K - 200K projection?? I heard something about it but assumed they were just pulling numbers out of their asses. This is actually worse in some ways. https://t.co/S2qJetjdTS

— Charles Gaba (@charles_gaba) April 12, 2018

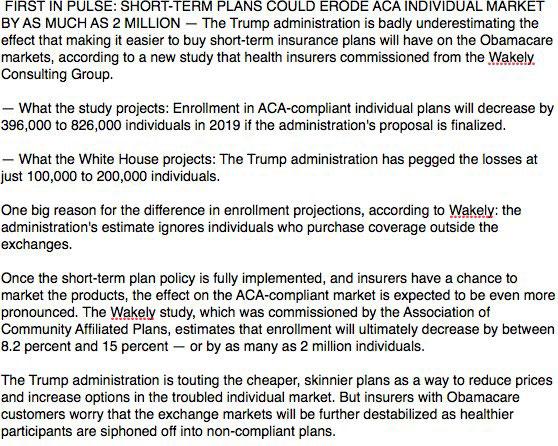

Just as I didn't notice this tidbit at the time, it took me until today to get around to writing up a full post about it. As it happens, HealthAffairs has a full report about not only the Wakely Consulting analysis quoted above but also about a similar analysis by Oliver Wyman about the likely impact to the individual market of Donald Trump's #ShortAssPlans executive order, which would open the floodgates for non-ACA policies to sabotage and undermine the ACA-compliant risk pool.

Sure enough, it turns out that when Trump's HHS Dept., Labor Dept. and Treasury Dept. (the "tri-agencies") wrote up the proposed rule to flood the market with dirt-cheap junk plans, here's what they projected:

Despite these concerns, the tri-agencies estimate that the impact of the changes outlined in the rule would be minimal, resulting in the shift of only 100,000 and 200,000 individuals from marketplace coverage to short-term coverage. Implicit in this assumption is that these individuals would skew younger and healthier because they would need to be able to pass medical review. To calculate this number, the tri-agencies cite enrollment trends prior to the 2016 rule and assume that only about 10 percent of these enrollees would have been eligible for subsidies through the marketplace.

...The proposed rule estimated that enrollment in the ACA-compliant individual market would drop between 100,000 and 200,000 people and that premiums would increase between 0.3 to 0.6 percent.

At first glance this doesn't sound too bad: ~150K out of 11.8 million...why, that's only 1.3% of the total ACA exchange market; no biggie, right?

There's two major problems with this projection.

First, even if it was accurate, it's critical to understand that those 100K - 200K people would likely be among the healthiest enrollees, which means that premium increases of only 0.3 - 0.6% more are...suspicious, to put it mildly.

The larger problem is that, as I alluded to in my tweet, and as HealthAffairs confirms today, Donald Trump's HHS, Labor and Treasury Departments all "forgot" to include around 40% of the total individual market:

Wakely’s estimates account for enrollment changes both inside and outside of the marketplace, whereas the federal estimate of up to 200,000 accounts only for changes in on-marketplace enrollment. To do a more direct comparison, Wakely adjusted the federal estimates to account for off-marketplace enrollment. According to the adjusted estimates, overall enrollment in the ACA-compliant individual market (both on- and off-marketplace) would decrease by between 400,000 and 790,000, and premiums would increase by between 0.7 and 1.4 percent. These numbers are much worse than estimates in the proposed rule.

The off-exchange market may only make up 40% of the total ACA individual market, but it makes up 70% of the total unsubsidized ACA market (around 4.5 million with the other 2.0 million being on-exchange), and since it's the unsubsidized enrollees who are by far the most likely to flee the ACA market, it makes sense that when you include them in the mix the number of people dropping ACA polices for #ShortAssPlans would triple or quadruple. Instead of a 1.3% enrollment drop we're talking about more like a 3-4% drop...and again, that's likely to be the healthiest 3-4% of the ACA market (~600,000 people), meaning significant rate hikes for the remaining 96% or so.

I'm sure completely ignoring 4.5 million unsubsidized ACA market enrollees was an honest mistake, right?

Wakely’s findings are consistent with an analysis from Oliver Wyman on behalf of the D.C. Health Benefit Exchange Authority. Oliver Wyman found that the proposed rule alone would increase claim costs in D.C.’s individual market by up to 3.1 percent; enrollment in the city’s individual market would decline by 900 people. Combined with repeal of the individual mandate penalty, claim costs would increase further, up to 21.4 percent, and enrollment would decline by about 6,100. Like Wakely, Oliver Wyman modeled a variety of different scenarios based on low and high take-up of short-term plans.

It's important to keep in mind that Oliver Wyman estimates that the pre-change individual market in DC is only around 17,000 people, so the #ShortAssPlan scheme alone would result in a 5.3% enrollment drop...although it would likely be closer to a whopping 36% drop when you also include the individual mandate repeal.

(DC's total on-exchange enrollment was around 19,200 this year, but Oliver Wyman is presumably including net monthly attrition. Unlike the rest of the country, DC's entire ACA-compliant market is on-exchange).

Oliver Wyman also included an estimate of the combined impact of the repeal of the individual mandate penalty, the proposed rule on short-term plans, and the proposed rule on association health plans. If all three are fully implemented at the same time, the combined impact would increase claim costs by up to 19.9 percent. (Informed by recommendations from the D.C. Health Benefit Exchange Authority, Mayor Muriel Bowser included a District-level individual mandate in her 2019 budget proposal, but it is up to the city council to adopt the mandate or not.)

Obviously DC is pretty tiny and has a lot of unusual circumstances, but between these two analyses from highly-respected consulting firms, it sounds like the #ShortAssPlans scheme alone will likely lead to a good 600K people dropping out of the market and a 1-3% premium increase for everyone else (around $6 - $18/month per enrollee, or $72 - $216/year) even without the impact of the GOP's repeal of the individual mandate.

As an aside, the Wakely analysis also includes a handy bullet point listing of some of the major differences between ACA policies and #ShortAssPlans (aka "STLDI" or "Short-Term Limited Duration Insurance"):

- Many STLDI plans have deductibles of $7,000 to $20,000 for three months of coverage, compared to ACA-compliant plans which are for a year of coverage and legally cannot exceed an amount preset by the Secretary (for example, deductibles for ACA-compliant individual plans were essentially capped at the maximum out of pocket amount of $7,150 in 2017).

- The American Academy of Actuaries notes that many STLDI plans have coverage limits of $1 million while ACA-compliant plans do not have annual limits.

- At the time of renewal or purchase, STLDI plans can exclude coverage for any condition developed in the prior coverage period. Individuals not only can be excluded due to illness when they initially purchase the coverage, but if re-occurring or chronic conditions occur while individuals have STLDI, then they would be unlikely to be covered again at the time of renewal. This is different from even pre-ACA individual market coverage, in which additional underwriting was not conducted at renewal.

- Additionally, ACA rating rules, such as age and gender restrictions, do not apply so these plans can charge higher premiums for individuals who have health conditions or can charge more based on a person’s sex.

- STLDI plans do not have to follow Medical Loss Ratio (MLR) restrictions so fewer premium dollars go to paying medical coverage and instead go to administration and profit. Historically, these ratios have been much lower in STLDI plans (for example the largest insurer of STLDI products in 2016 had a MLR below 50%, far below the 80% required MLR in the ACA-compliant individual market).

- Individuals in STLDI plans would be at risk for rescission. Rescissions are retroactive cancellations of coverage, often occurring after individuals file claims due to medical necessity. While enrollees in ACA coverage cannot have their policy retroactively cancelled, enrollees in STLDI plans can. According to Georgetown University, reports suggest issuers offering STLDI plans have been aggressive at using rescissions to shift their liability onto consumers.

Advertisement