Stating the Obvious: There's *another* reason enrollments fell short of projections this year...

Thu, 02/09/2017 - 6:01pm

I've written a lot about the negative impact on enrollment this year due to deliberate sabotage efforts on the part of Donald Trump and the Congressional GOP, and I stand by it. I've run the numbers and honestly believe that I've proven pretty conclusively that these efforts--in particular, the last-minute yanking of millions of dollars' worth of HC.gov "Final Deadline!" advertising--had a significant negative impact, to the tune of several hundred thousand "lost" enrollments.

However, I've also repeatedly stressed that there were most definitely other factors as well which can't be pinned on Trump's efforts. Some of these are quantifiable and pretty obvious:

- Louisiana expanded Medicaid; this likely cannibalized a good 60,000 people who otherwise would've enrolled in exchange QHPs.

- New York's BHP program skyrocketed; it likely cannibalized at least 30,000 (and potentially up to 286,000)

Other than this, though, there's a pretty obvious "Occam's Razor" explanation as well: Higher premiums and carriers dropping out of the exchange.

Significant premium increases shouldn't have had much impact on those who qualify for tax credits (about 85% of exchange enrollees), but they obviously are gonna be a big turnoff to winning over enrollees who don't qualify for credits (or who only qualify for nominal assistance). By the same token, any time a carrier drops out of the market, some percentage of their enrollees are gonna decide to make other arrangements rather than switch to a different carrier.

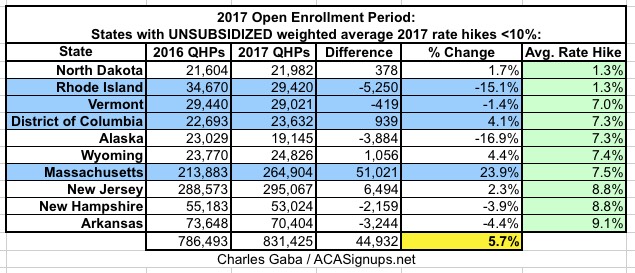

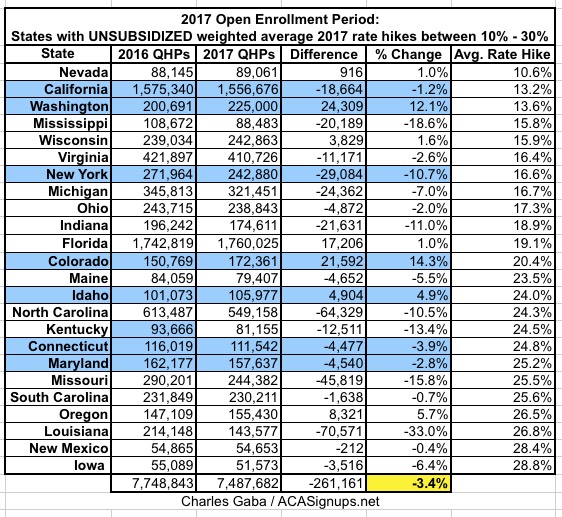

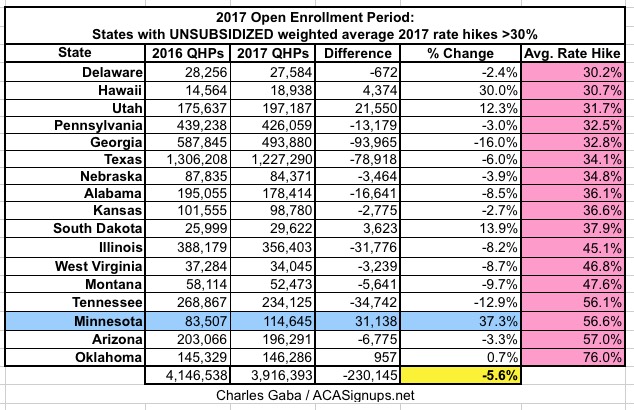

I don't really have the data to determine the impact of the latter, but I have hard evidence of the former...namely, my own State By State 2017 Rate Hike Project from last fall. As you may recall, I (fairly accurately) projected the weighted unsubsidized average rate hikes for the entire ACA-compliant individual market in each state. Nationally, I came up with an overall average of around 25%, but this varied widely from state to state...from as low as 1.3% in North Dakota and Rhode Island to as high as a whopping 76% in Oklahoma.

So, what I've done is to break out the year-over-year exchange enrollment change into three groups:

- States where rates increased by under 10%

- States where rates increased between 10-30%

- States where rates increased by more than 30%

...and the results tell the story:

- In the 10 states where unsubsidized premiums only went up modestly (and yes, anything under 10% has been "modest" in the health insurance industry since long before the ACA was passed), enrollments increased by an average of 5.7% over last year (slightly higher once Vermont's final number comes in). Worth noting: 4 of the 10 happen to run their own exchanges.

- In the 24 states where unsubsidized premiums increased between 10-30%, enrollment dropped by an average of 3.4%.

- Finally, in the 17 states where unsubsidized premiums increased by over 30% over 2016, enrollment dropped by 5.6%. (Again: Worth noting that this only includes 1 of the state-based exchanges, Minnesota...which, as it happens, actually increased their enrollment total by a whopping 37% over last year...in large part, I presume due to the last-minute "25% discount" policy enacted by the state legislature, which actually brings MN's average rate hike down to around 17%, meaning it "should" really be included in the 2nd group.)

Remember, the original projections by both the HHS Dept. and myself called for around 13.8 million. The actual total is around 12.2 million (possibly 12.3 million in the end). My gut tells me that the "TrumpScare" sabotage efforts killed off perhaps 500K enrollments, but that enrollments would've been another 500K - 1.0M higher if not for the excessive rate increases on the unsubsidized enrollment pool and a number of carriers dropping out of the exchanges (in fact, Rhode Island specifically blamed UnitedHealthcare's withdrawl as being one of the major factors).

Advertisement