In which I actually defend the insurance carriers on something.

Tue, 04/19/2016 - 11:41am

As I've stated many times in the past, I'm in favor of ultimately phasing out most of the private, for-profit insurance industry. My timeline and specifics differ greatly from, say, Bernie Sanders's proposed single payer plan, and I think there's room for the private market for supplemental insurance, but I'm no fan of keeping things as they are. While not every carrier is guilty of doing so, the health insurance industry as a whole has repeatedly proven itself to have a hell of a lot of bad corporate citizens over the years, to put it mildly.

Having said that, there are some criticisms which aren't always warranted, and one of these just came up today in light of UnitedHealthcare's decision to pull out of the ACA exchanges in most of the 34 states they're currently operating in...or more specifically (since United wasn't even participating the first year), the losses sustained by many other carriers during the first 2 Open Enrollment Periods for 2014 and 2015.

Many people have pointed out (including myself) that most of these carriers actually priced their policies too low for each of these years (and yes, I realize that this may sound ludicrous to many of the people enrolled in these policies, but I'm looking at it from the corporate bottom line perspective here). "Serves them right!" some said, for foolishly underpricing in order to snap up market share, and then getting bitten in the ass by that decision.

When pricing their policies for the following year, the carriers are supposed to gather up all of their actual financial/claims data from the previous year and use that to try and project what they expect their claims expenses are going to be for the next year. They then submit those filings to state and/or federal regulators, using the data to justify whatever premium rate increases they're asking for imposing.

The regulators are supposed to then review all of the numbers themselves and determine whether or not they think the carrier's analysis and projections are accurate/reasonable or not. If they agree, they approve the rate changes. If they disagree, they might reduce the requested increase (from a 10% hike to a 5% hike) or, in some cases, even require the carrier to reduce premiums...from 10% to -5%, for instance.

Finally, in some cases, they may actually require the carrier to increase rates more than the carrier asked them to (15% instead of 10% or whatever). There are two reasons they might do this: First, since the Risk Corridor, Risk Adjustment and Reinsurance programs are/were supposed to cover a portion of the losses of carriers who underperformed, they want to keep an eye out for carriers trying to pull a fast one. That is, a carrier might deliberately price their policies at a loss to scoop up huge marketshare, knowing that the feds will cover most of their losses, in the hopes of quietly jacking up those rates in the future. The other reason regulators might require a greater increase is to save a carrier from itself--the regulators have an obligation to make sure that the carriers remain viable, with enough assets to cover the policy claims which come in throughout the year.

On the surface, it looks as though both the carriers as well as the regulators did a lousy job of predicting the costs for both 2014 and 2015, right? Well, perhaps...except for some important caveats.

For 2014, no one had the slightest clue what the market would look like. The ACA exchanges turned the entire individual market upside down; the assumptions and formulas that insurance carriers and regulators had been using for decades no longer had much meaning since the rules changed. In many ways this was a good thing, since those old assumptions included things like "cherry picking your enrollees", "kicking them off their policies over minor technicalities the moment they actually need you the most" and so forth. Nonetheless, those rules were no longer applicable, so trying to figure out how to price plans for 2014 was a complete crapshoot (this, in fact, was one of the main reasons that the "Risk Corridor" program and the like was implemented in the first place, to help cushion the blow from botching the projections).

For 2015, however, the carriers should have had a full year of data under their belt so that they could adequately project expected costs over the 2nd year, right?

Well...not quite.

Here's the thing you have to remember: The insurance carriers can't wait until 5 minutes before the next open enrollment period begins to figure out their pricing. They're legally required to submit their rate requests to regulators as much as 6 months earlier (June or July at the latest), depending on the state. It takes a lot of time to comb over all of the data, run analysis and make projections, and then there's a whole mess of paperwork which has to be compiled to support the claims. That then has to be be reviewed in detail by the regulators. Then, the final rates have to be added into the systems of both the carriers, the regulators and the exchanges.

All of this means that the initial pricing requests for 2015 policies had to be submitted by perhaps June 2014...and the supporting data was completely dependent on the limited 2014 data they had on hand at that time.

Normally the carriers would have used the full 2013 data to make their projections for 2015, but since the individual market was so utterly different, they had to look at the first few months of 2014 to figure it out.

OK, so instead of 12 months of data, they only had 3. That sucks, but at least it's something, right?

Well, again...not quite.

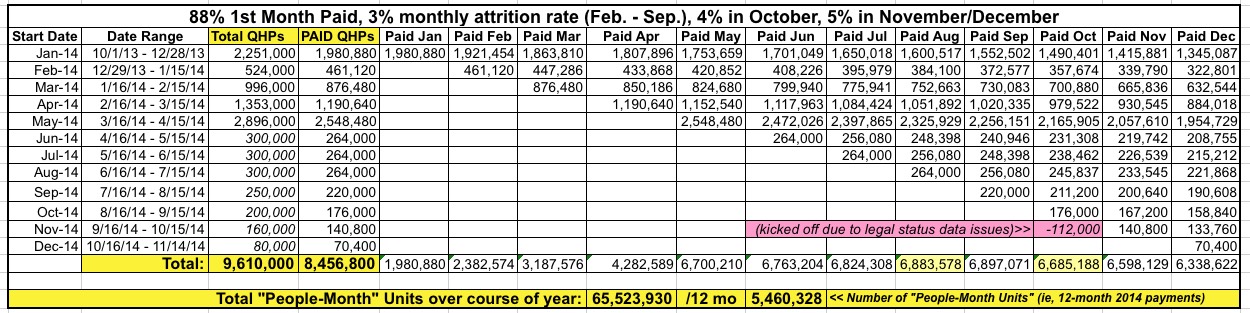

Remember, due to both 2014's 6-month open enrollment period (October - March, plus the 2-week "overtime" period in April) and especially the massive technical problem in October/November 2013 when the exchanges first launched, only about 60% of 2014's exchange enrollees were even effectuated as of March.

In fact, it was even worse than that. Here are the 2014 exchange enrollment figures for each month of 2014:

- 2.2 million selected plans between 10/01/13 - 12/28/13

- 1.1 million more selected plans between 12/29/13 - 2/01/14

- 940K more selected plasn between 2/02/14 - 3/01/14

- 3.8 million more selected plans between 3/02/14 - 4/19/14

Aside from the deadline extension in December, after that, you had to enroll by the 15th of a given month in order to have your coverage start on the 1st of the following month, which is why the table above is broken out differently from the links above.

As you can see, after lopping off those who never paid at all, only around 2 million people were even enrolled in exchange policies in January 2014. Another 400K or so were enrolled in February, and around 800K more for March. The rest didn't even start coverage until either April or May, by which point the actuaries for the various carriers were already furiously scrambling to cobble together the data from January, February and March.

So...instead of having 8 million QHP selections to work with (of which only around 7 million actually became effectuated), the actuaries only had the following hard enrollment data available when pricing things for 2015:

- 2.0 million people for January

- 2.4 million for February

- 3.2 million for March

That means they only had data for an average of 2.5 million enrollees per month to work with...versus a total independent market which had been over 11 million the previous year.

And all of this was after having expected several million more people to have their NON-ACA compliant policies terminated effective December 31, 2013...only to then be informed that those policies would mostly stay in place for a year or three longer.

BUT WAIT, THERE'S MORE!

As was pointed out to me this morning, not all of the claims are sent in right away. The claims for heart surgery performed in, say, mid-March might not actually be sent to the insurance carrier until May or June, and so on.

The point of all this is that it wasn't until planning their pricing for 2016 that the insurance carriers and their corresponding state/federal regulators had full, proper data to work with for 2014. And even then, last summer's drama surrounding both the King v. Burwell case, followed by the Risk Corridor Massacre last fall both threw huge monkey wrenches in the works for projecting this year.

What about 2017? Well, things should be somewhat easier to pin down this time around. They'll have all of 2014's data, and just about all of 2015's, since the Open Enrollment Perido was cut down to 3 months last year, ending in mid-February. In addition, King v. Burwell is a thing of the past, and while the Risk Corridor program is still crippled, at least they know about it ahead of time.

However, the history of the ACA has proven time and time again that just when you think things have settled down, some crazy new development arises...so stay tuned...

Advertisement