Californians: How much will CA's expanded/enhanced subsidies reduce YOUR ACA premiums?

Wed, 10/16/2019 - 9:25am

As I noted yesterday, while the 2020 Open Enrollment Period doesn't officially start until November 1st across the rest of the country, in California it already started on October 15th, two weeks earlier than everywhere else.

I also noted that there's two important points for CA residents to keep in mind starting this Open Enrollment Period:

- First: The individual mandate penalty has been reinstated for CA residents. If you don't have qualifying coverage or receive an exemption, you'll have to pay a financial penalty when you file your taxes in 2021, and...

- Second: California has expanded and enhanced financial subsidies for ACA exchange enrollees:

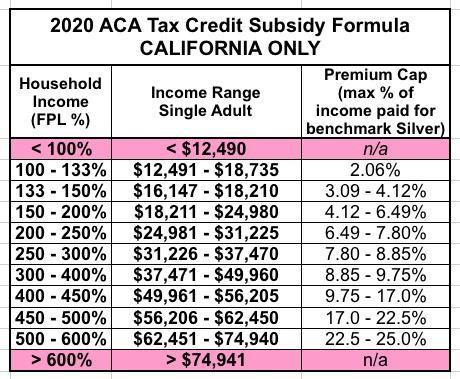

Until now, only CoveredCA enrollees earning 138-400% of the Federal Poverty Line were eligible for ACA financial assistance. Starting in 2020, however, enrollees earning 400-600% FPL may be eligible as well (around $50K - $75K/year if you're single, or $100K - $150K for a family of four). In addition, those earning 200-400% FPL will see their ACA subsidies enhanced a bit.

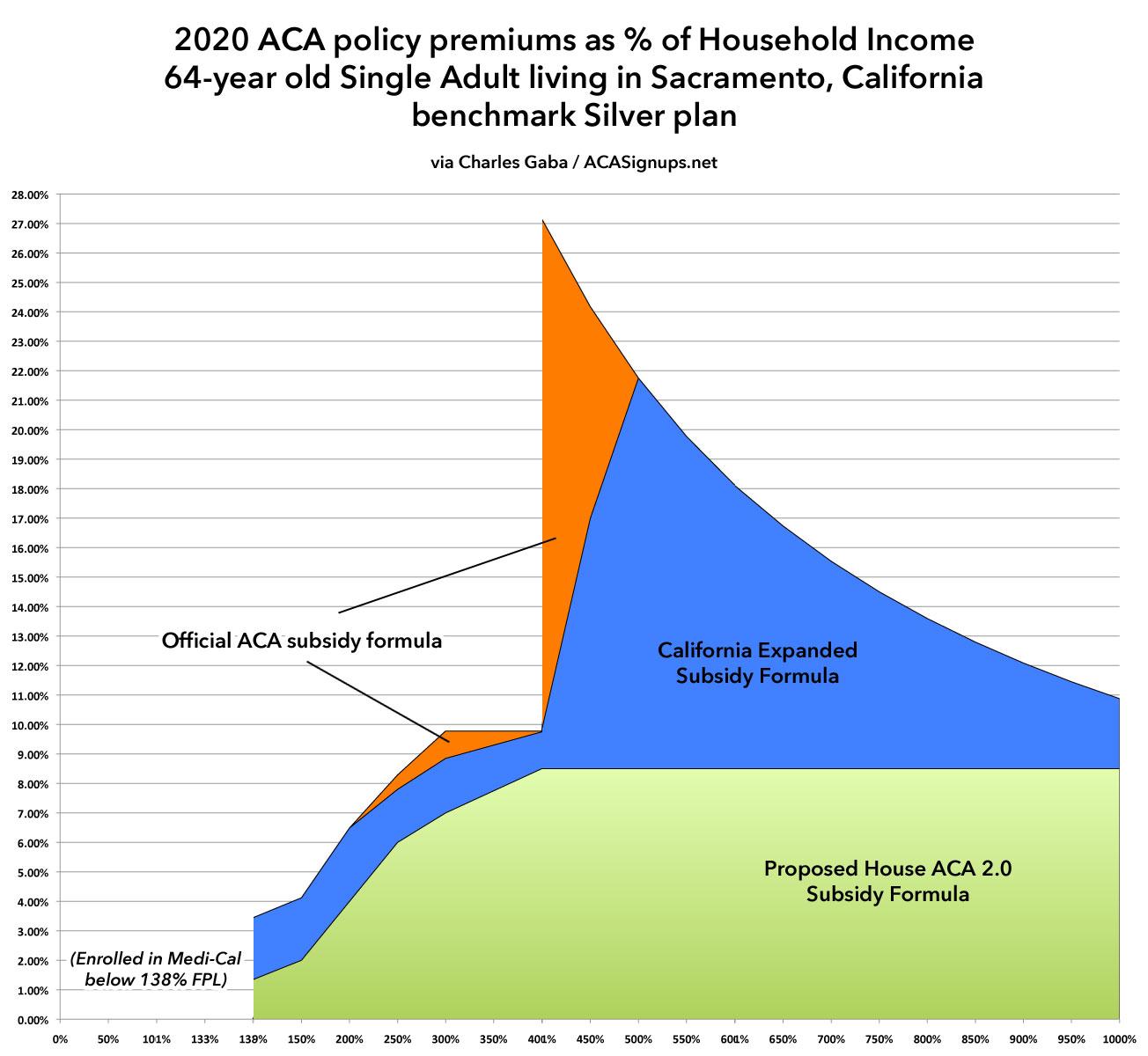

Here's what the formula looks like:

The actual savings compared to the current formula will vary greatly by region, age, plan chosen and household, of course.

With that in mind, I've whipped up several examples showing how different California households will fare compared to the official ACA subsidy structure for 2020. It's important to keep in mind that all of these assume they're enrolling in the benchmark Silver plan. If they go for a Bronze, Gold, Platinum or different Silver, things will look a bit different as well.

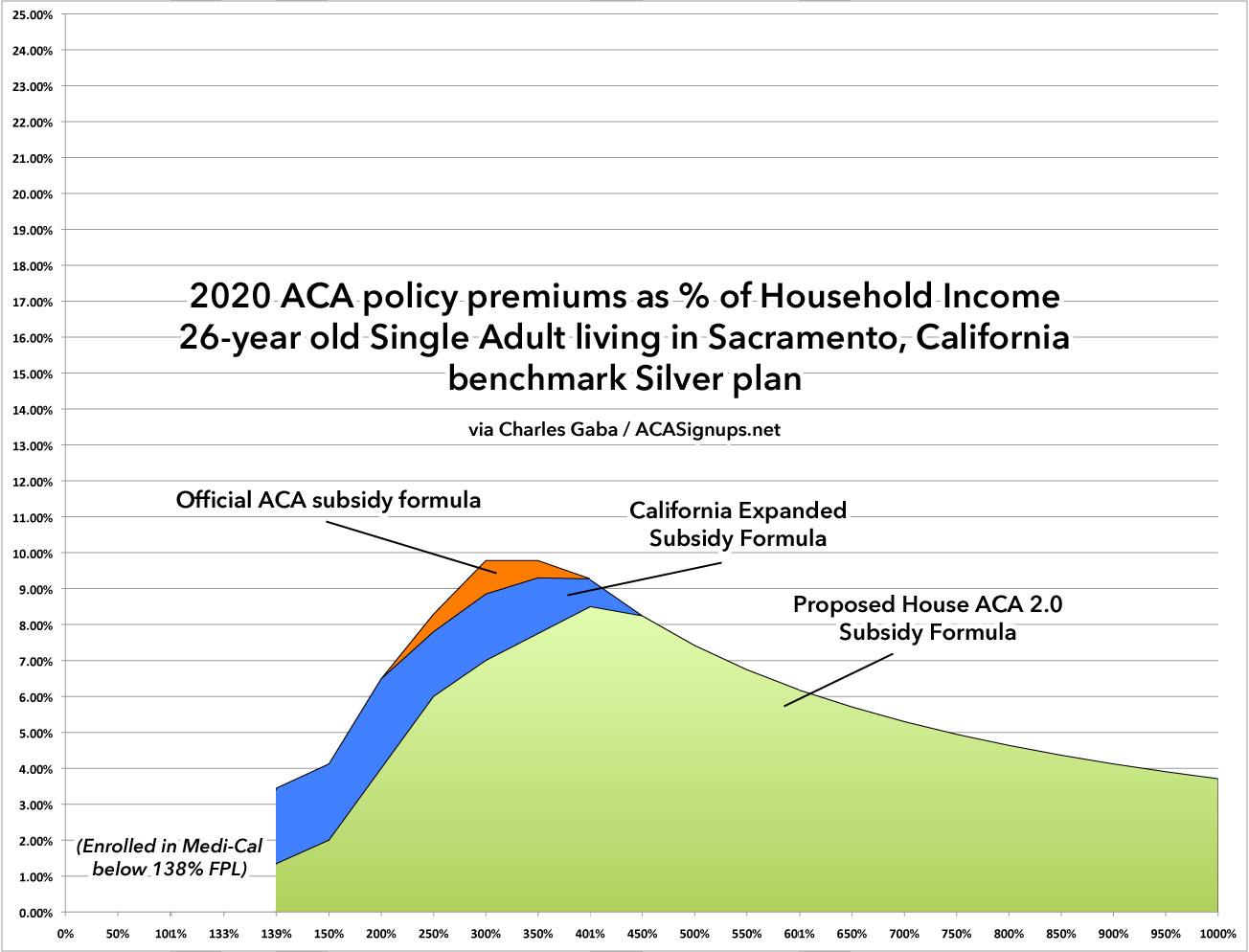

I've also included a third overlay on the tables below: The federal House Democrats ACA 2.0 bill (either H.R. 1868 or H.R. 1884), which would cap premiums at no more than 8.5% of income. The official ACA formula is in Manilla; the California subsidy formula is in Orange, and the proposed ACA 2.0 structure is in Green.

Unsubsidized ACA premiums for the same policy can only vary based on three factors: The age of the enrollee(s) (within a 3:1 range); whether they smoke or not; and what geographic rating area they live in. California is split into 19 Rating Areas.

Since I used Sacramento in my first example, I'll stick with it. Sacramento (both the city and county) is located in CA's 3rd Rating Area, which also includes Placer, El Dorado and Yolo Counties.

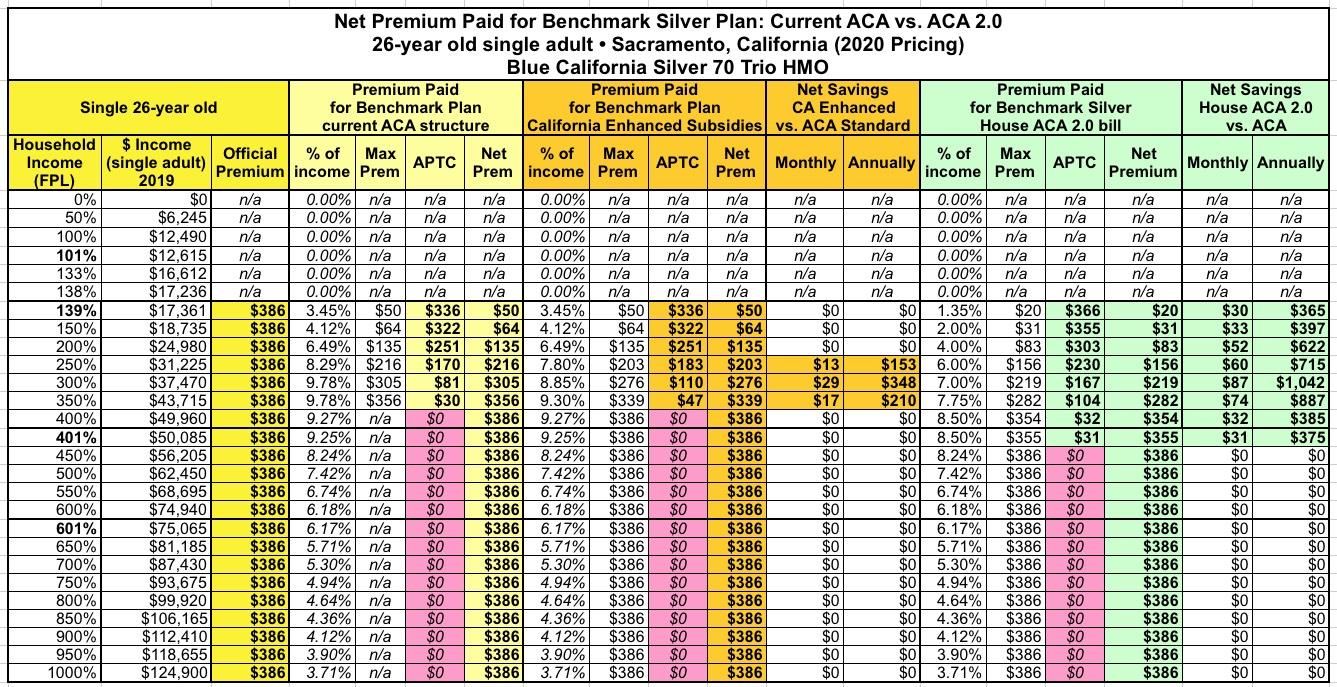

First, here's a single 26-year old...let's say, a young adult just moving off of their parents' healthcare coverage. The unsubsidized benchmark silver premium for them is $386/month, or $4,632/year. Under the official ACA subsidy structure, they'd receive as much as $336/month in federal tax credits if their income ranges between 138 - 400% FPL, limiting their premiums to no more than $50 - $386/month. The full price falls below the subsidy threshold at around $47,300.

This means that California's expanded subsidies don't do anything for 26-year olds in the 400-600% range...but from 250-350%, they'd save as much as an additional $348 for the year.

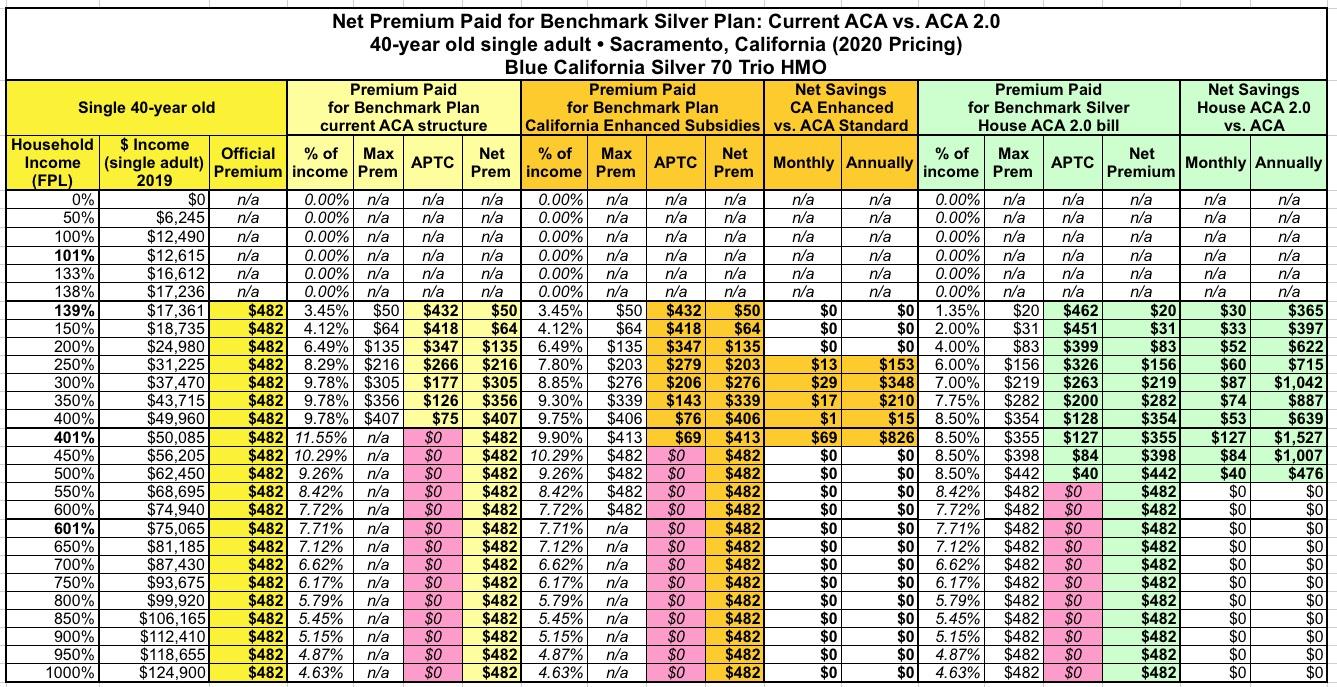

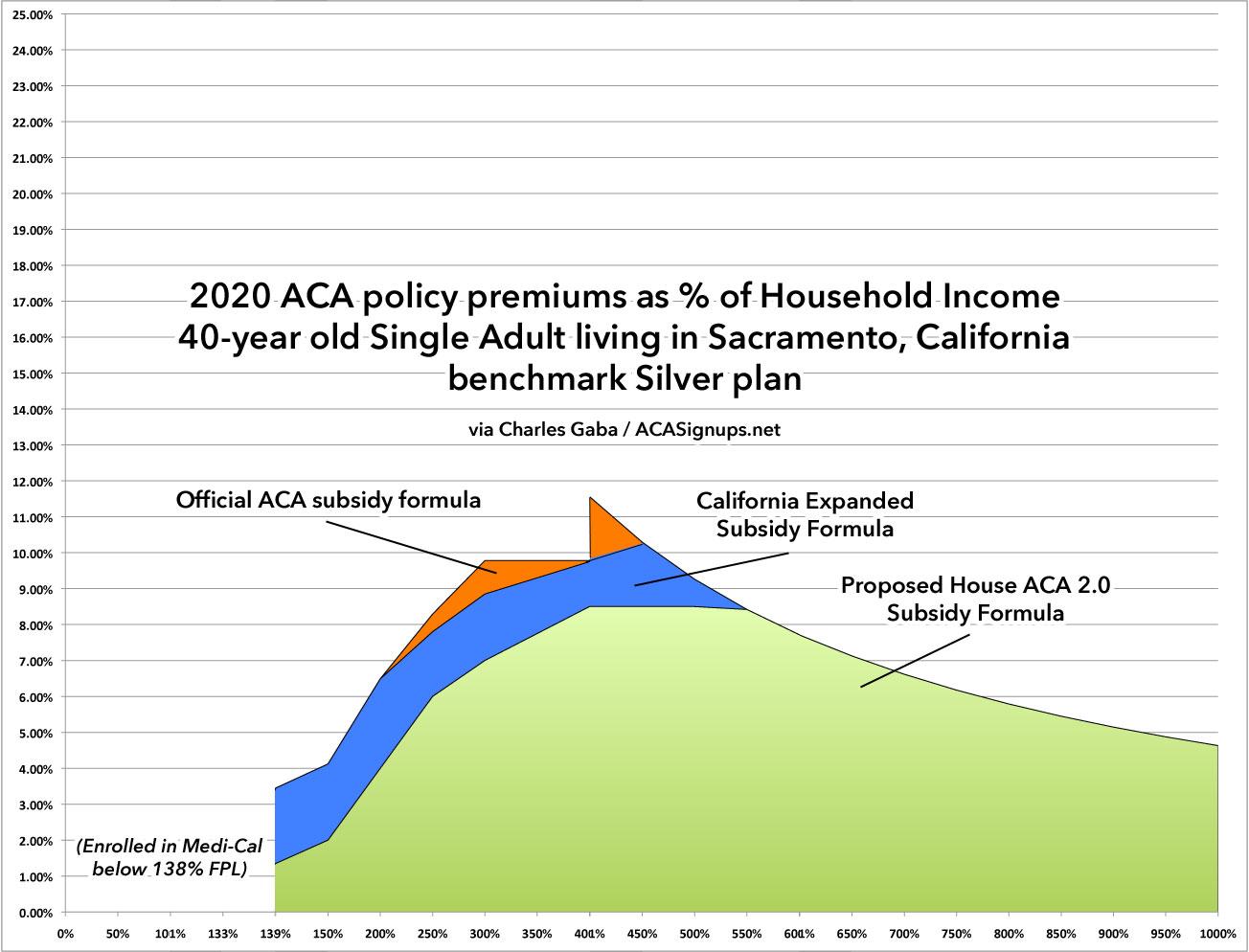

Next, let's look at a single 40-year old. Their unsubsidized premium is $482/month, or $5,784/year.

Under the official ACA subsidy structure, they'd receive as much as $432/month in federal tax credits if their income ranges between 138 - 400% FPL, limiting their premiums to no more than $50 - $407/month. At exactly the 400% threshold, however ($49,960), their subsidies are immediately cut off.

At 40 years old, California's expanded subsidies will save them up to $826 if they earn between 400-450% FPL...and from 250 - 400%, they'd save as much as an additional $348.

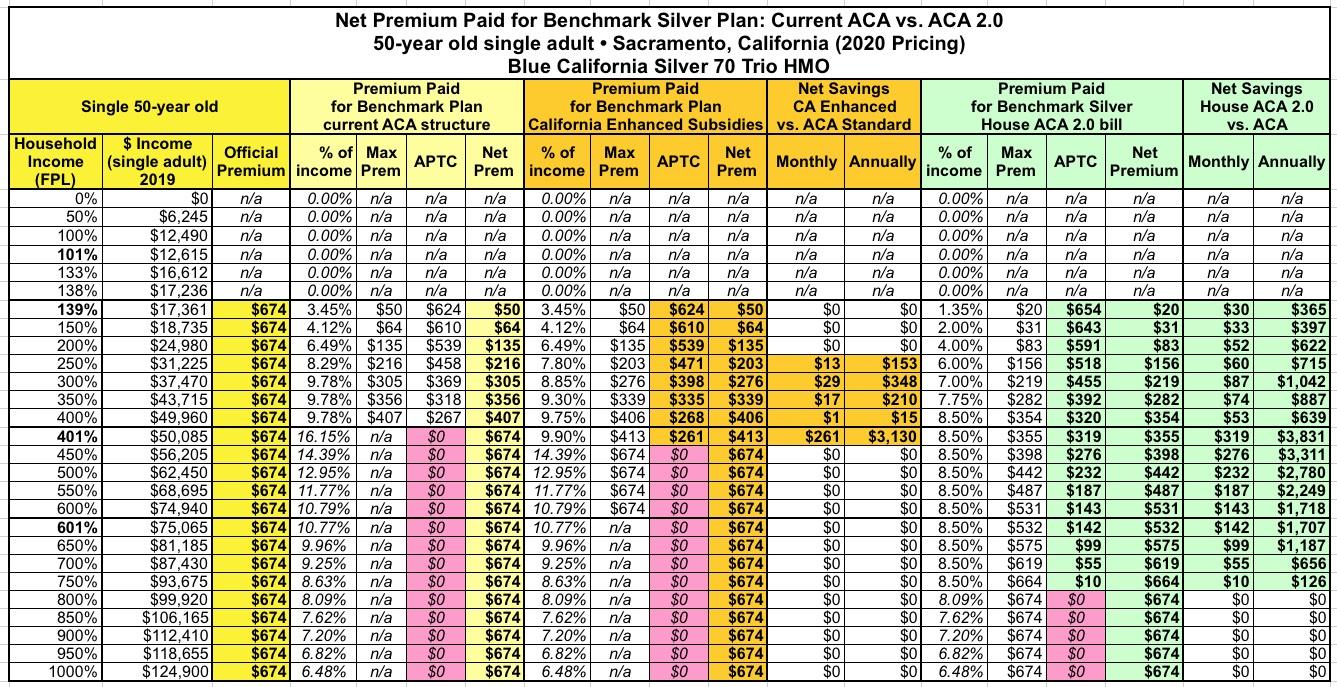

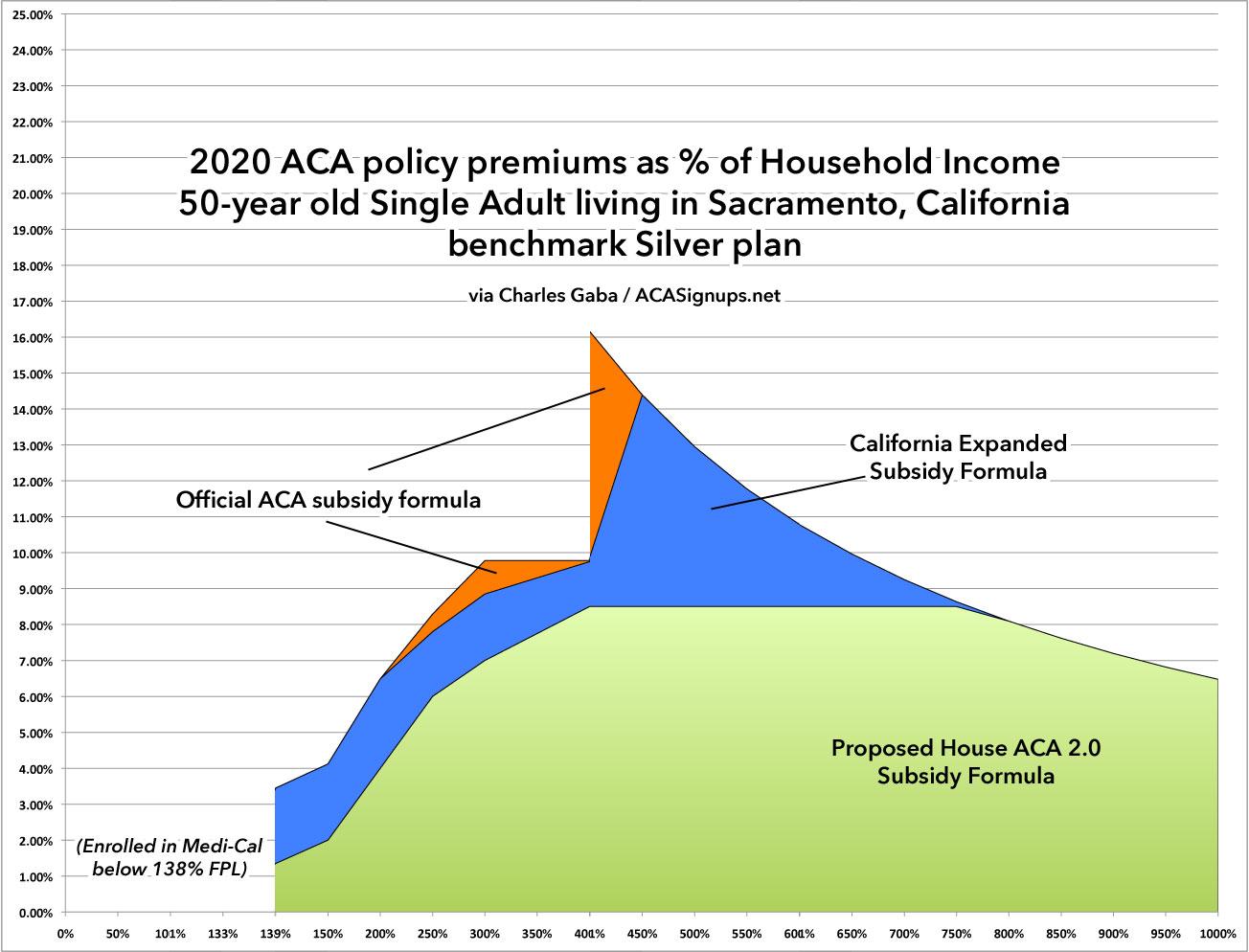

Next up: A single 50-year old. Their unsubsidized premium is $674/month, or $8,088/year.

Under the official ACA subsidy structure, they'd receive as much as $624/month in federal tax credits if their income ranges between 138 - 400% FPL, limiting their premiums to no more than $50 - $407/month. At exactly the 400% threshold, however ($49,960), their subsidies are immediately cut off.

At 50 years old, California's expanded subsidies will save them up to $3,130 if they earn between 400-450% FPL...and from 250 - 400%, they'd save as much as an additional $348.

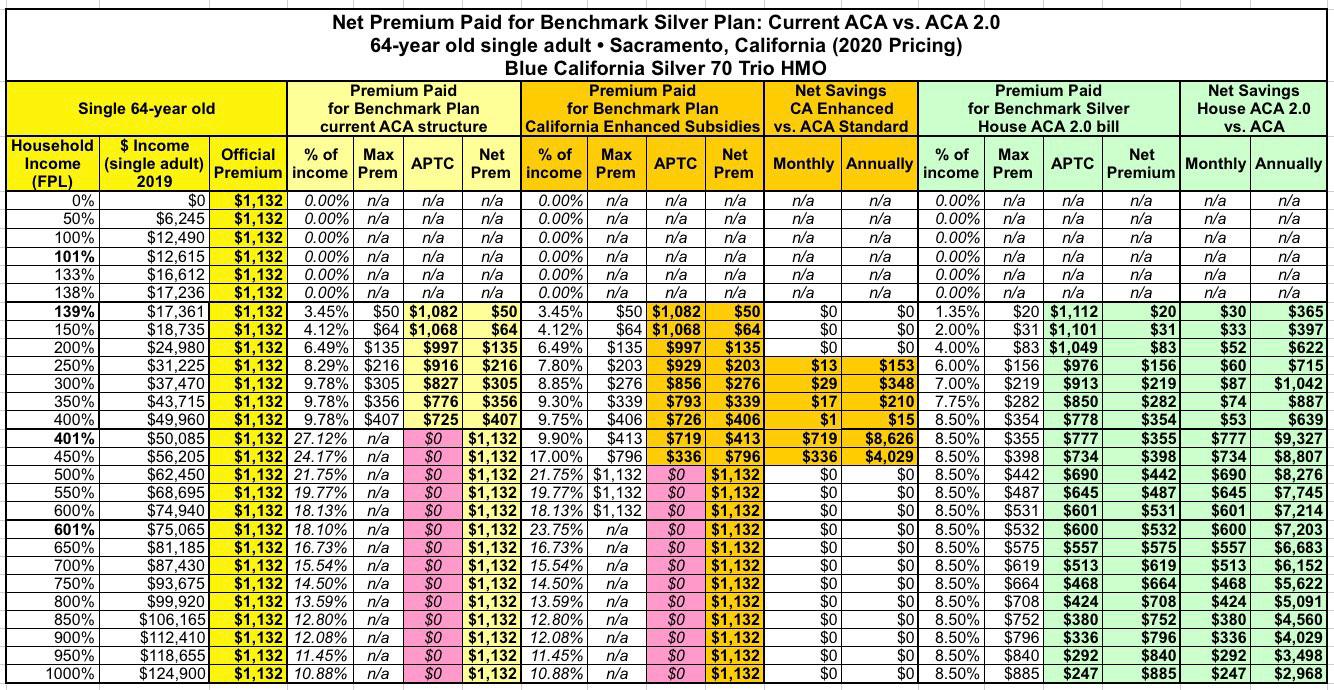

Finally, let's go back to the single 64-year old I wrote about yesterday. Their unsubsidized premium is a whopping $1,132/month, or $13,584/year. That's a ludicrous 27% of their income.

Under the official ACA subsidy structure, they'd receive as much as $1,082/month in federal tax credits if their income ranges between 138 - 400% FPL, limiting their premiums to no more than $50 - $407/month. At exactly the 400% threshold, however ($49,960), their subsidies are immediately cut off.

At 64 years old, California's expanded subsidies will save them up to $8,626 if they earn between 400-450% FPL...and from 250 - 400%, they'd save as much as an additional $348.

All four of these examples are for individuals. What about families? For that, I've put together four additional examples:

- A 30-year old single parent with one child

- A 40-year old married couple with two children

- A 50-year old married couple with one adult child still on their plan

- A 60-year old married couple

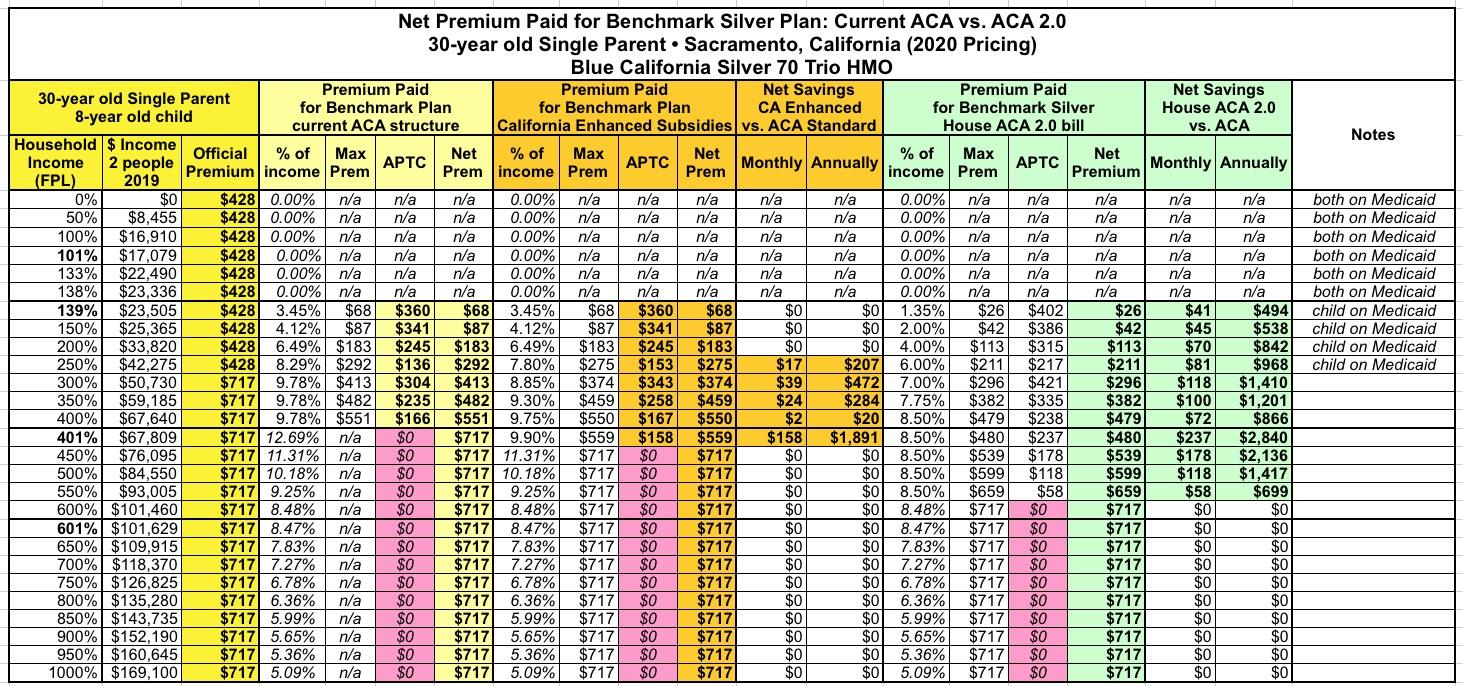

First up: The single parent (30 years old, one 8-year old child):

This actually gets a little trickier than you might think, because in California, children under 18 are eligible for Medi-Cal (Medicaid) if the household income is less than 266% FPL. This means that up to around $45,000, the parent would be eligible for a subsidized ACA exchange plan, while the child wouldn't be enrolled in that plan at all since they'd be enrolled in Medicaid instead. That means the parents' unsubsidized premium for the benchmark plan is $428 for herself only up until 266% FPL...at which point it increases to $717/month for both them and the child.

Under the official ACA structure, the total cost for both would be limited to no more than between $68 and $551/month between 138 - 400% FPL...after which it would immediately jump to the full $717/mo, or over $8,600/year. Under California's expanded subsidies, however, they'd receive additional savings of as much as $472/year between 250 - 400% FPL...and as much as $1,891 between 400-450%.

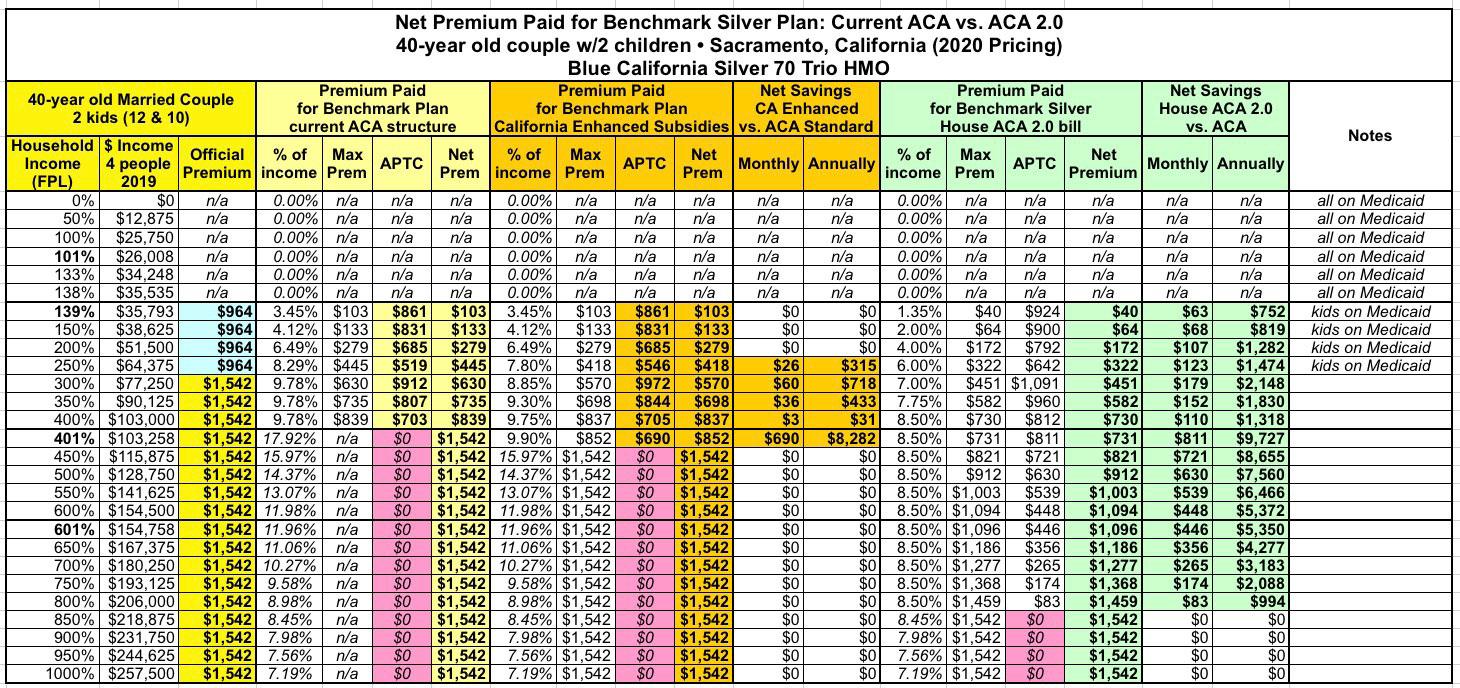

Next: A Nuclear Family...40-year old married couple with 2 children age 12 & 10:

Again, in California, children under 18 are eligible for Medi-Cal (Medicaid) if the household income is less than 266% FPL. This means that up to around $68,000, the parents would be eligible for a subsidized ACA exchange plan, while the children wouldn't be enrolled in that plan at all since they'd be enrolled in Medicaid instead. That means the parents' unsubsidized premium for the benchmark plan is $964 for themselves only up until 266% FPL...at which point it increases to $1,542/month for both them and the two children.

Under the official ACA structure, the total cost for both would be limited to no more than between $103 - $839/month between 138 - 400% FPL...after which it would immediately jump to the full $1,542/mo, or over $18,500/year. Under California's expanded subsidies, however, they'd receive additional savings of as much as $718/year between 250 - 400% FPL...and as much as $8,282 between 400-450%.

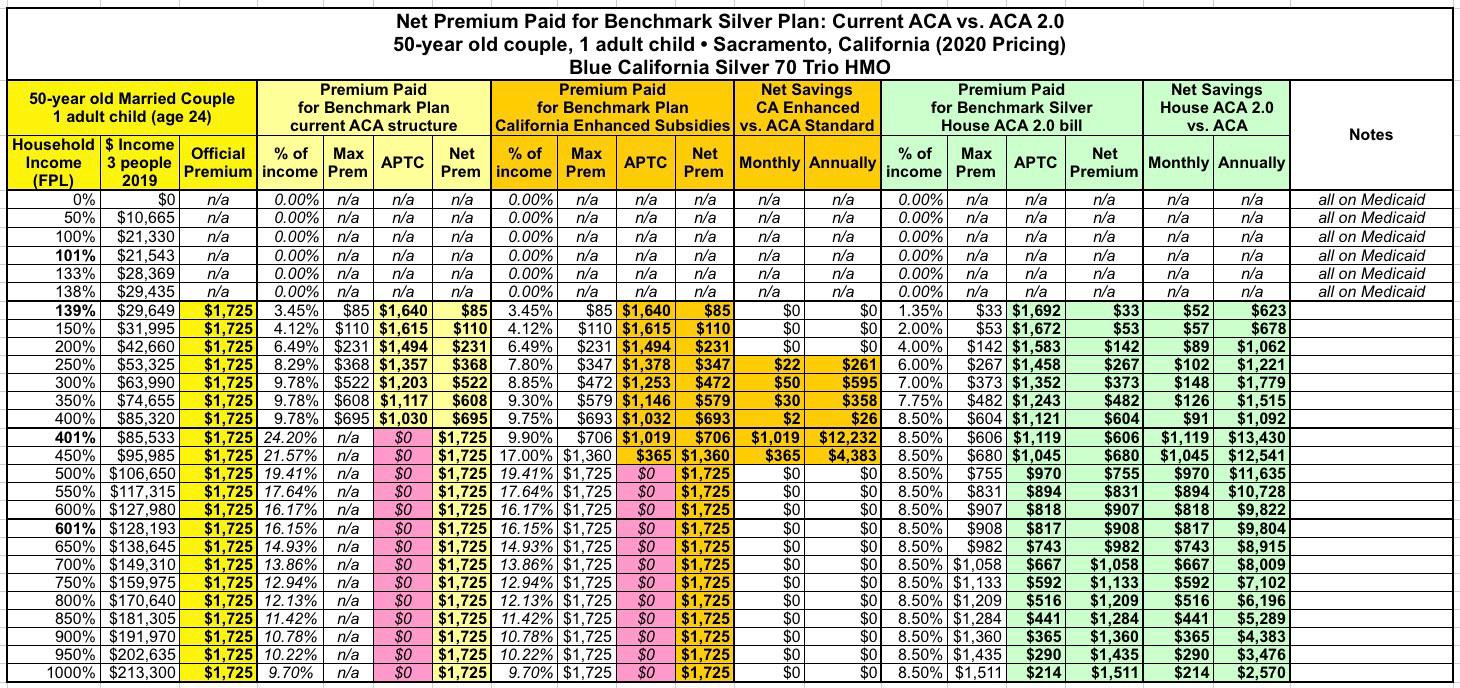

Next: Empty-Nesters...a 50-year old married couple with 1 adult child on their plan (age 24).

The Medi-Cal factor is no longer at play here since their kid is over 18, which simplifies things a bit.

Under the official ACA structure, the total cost for all three family members would be limited to no more than between $85 - $695/month between 138 - 400% FPL...after which it would immediately jump to the full $1,725/mo, or a whopping over $20,700/year...fully 24% of their total income.

Under California's expanded subsidies, however, they'd receive additional savings of as much as $595/year between 250 - 400% FPL...and savings of as much as $12,232 between 400-500%.

That's right...the net premiums for this family would drop from $20,700 down to just $8,500 if their household income hovers just over the 400% FPL threshold.

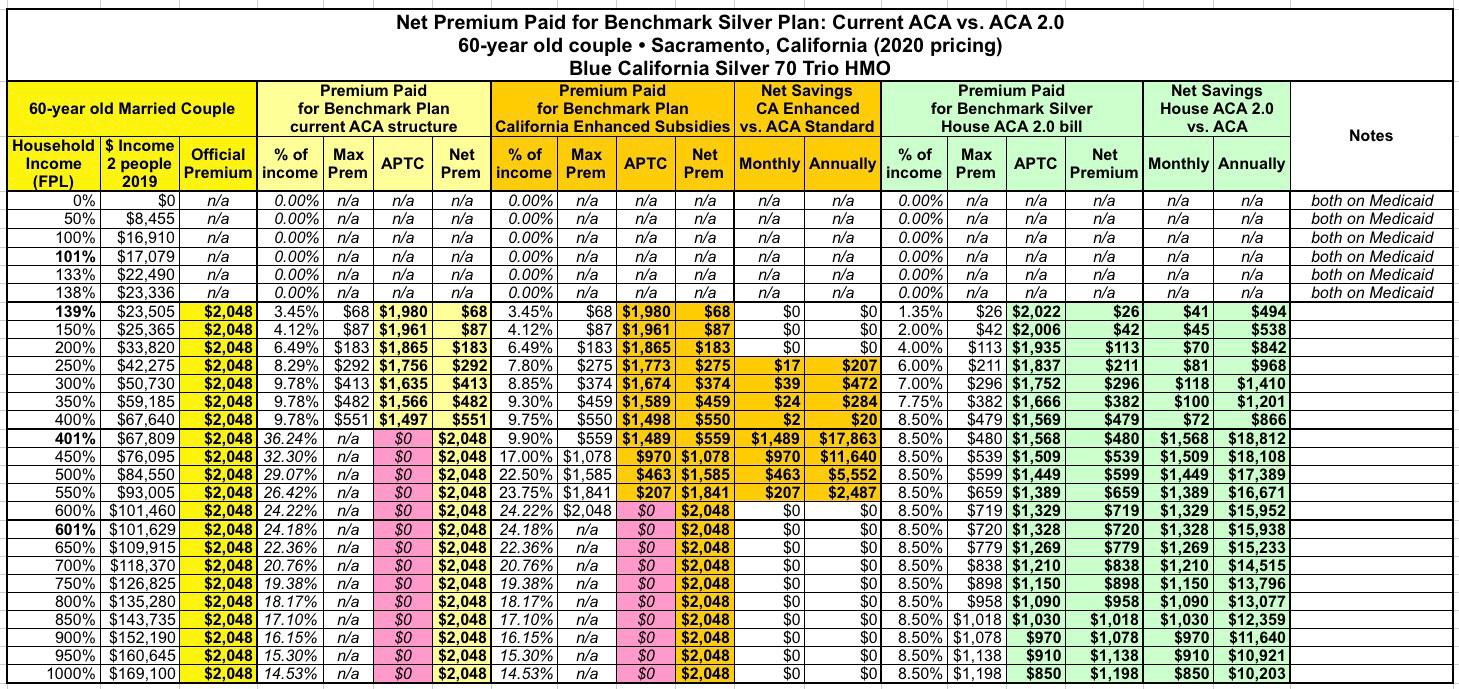

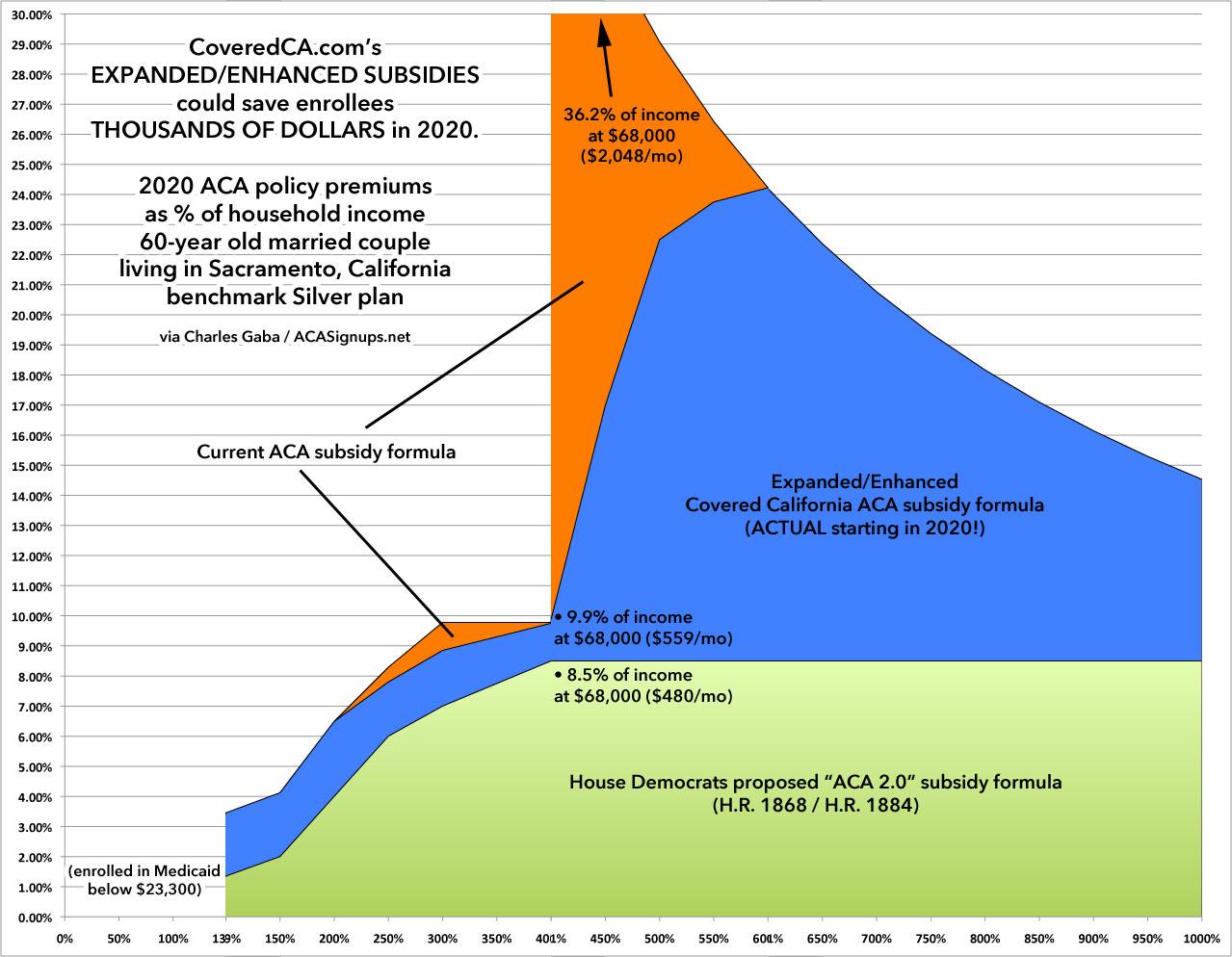

Finally, let's look at a 60-year old married couple:

The unsubsidized premium for this couple would, again, be an absurd $2,048/month. Under the current ACA formula, they're limited to paying between $68 - $551/month if their income ranges from 138 - 400% FPL, but skyrockets right after that; $2,048/month amounts to a jaw-dropping 36% of their total income.

Under the expanded California subsidies, the same couple would see their premiums plummet dramatically if they earn between 400 - 450% FPL...a reduction of an insane $1,489/month or nearly $18,000/year, and it would still drop pretty significantly between 450 - 550%, although they'd still be spending 17% of their income on the policy at that point.

So there you have it. Here's a summary of the maximum all 8 of these households could potentially save compared to what they'd be paying otherwise for an ACA benchmark Silver plan in 2020:

- Single 26-year old: Up to $348 in savings

- Single 40-year old: Up to $826 in savings

- SIngle 50-year old: Up to $3,130 in savings

- Single 64-year old: Up to $8,626 in savings

- 30-year old single parent w/1 child: Up to $1,891 in savings

- 40-year old couple w/2 children: Up to $8,282 in savings

- 50-year old couple w/1 adult child: Up to $12,232 in savings

- 60-year old couple: Up to $17,863 in savings

Again, this is for Sacramento County only. All of the amounts above will vary widely depending on the rating area, and of course different ages and household compositions will impact the amounts as well.

California's move here isn't ideal; there are still millions of people who won't be helped at all by it, and it won't be enough to make policies affordable even for many of those who are eligible for the extra subsidies...but for hundreds of thousands of Californians it should still make a big difference.

Advertisement